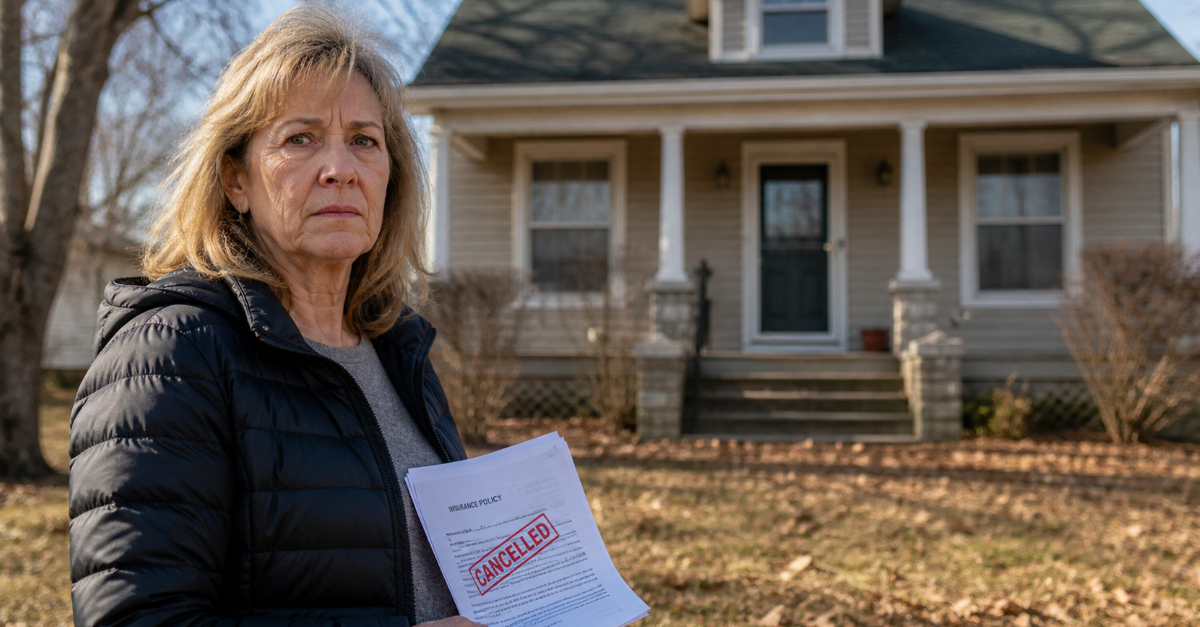

You Did Everything Right…So Why Is This Happening?

You handled things responsibly after your father passed. You insured the house, were upfront that it was a secondary home, and even paid the full year in advance. Now months later, the insurer is backing out anyway—and it feels like the rules changed after the fact.

What This Situation Usually Means

This feels like a broken promise, but insurance policies aren’t always as locked in as they seem. Even after payment and signing, insurers often include cancellation clauses that allow them to end coverage under certain conditions.

Insurance Policies Aren’t Truly “Guaranteed”

Most home insurance policies are written with terms that allow the company to cancel mid-policy. This can happen for underwriting reasons, risk changes, or internal policy updates, even if everything seemed approved at the start.

There’s Usually a Cancellation Clause

If you look closely at the policy documents, there’s almost always a section explaining when and how the insurer can cancel coverage. This is standard across most providers and is part of the contract you agreed to.

Secondary Homes Are Higher Risk

Insurance companies often view secondary or vacant homes as higher risk. These properties may be unoccupied for long periods, increasing the chances of unnoticed damage, theft, frozen pipes, or maintenance issues that lead to costly claims.

Why They Approved It Initially

Sometimes policies are issued quickly based on initial information, then reviewed more deeply afterward. This is called underwriting review, and it can happen weeks or even months after the policy starts.

Centre for Ageing Better, Pexels

Centre for Ageing Better, Pexels

Post-Issue Underwriting Happens More Than You Think

It’s not uncommon for insurers to revisit a policy after it’s already active. If they later decide the risk doesn’t meet their guidelines, they can choose to cancel—even if they knew some details upfront.

“They Knew” Doesn’t Always Lock It In

Even if you told them it was a secondary home, that doesn’t always prevent cancellation. If the policy was issued before a full underwriting review, the company may still reverse course later.

They May Have Changed Internal Rules

Insurance companies sometimes update their underwriting guidelines. If they decide to stop covering certain types of properties, like secondary homes, they may cancel existing policies that no longer fit their criteria.

Centre for Ageing Better, Unsplash

Centre for Ageing Better, Unsplash

Timing Matters

Most cancellations like this happen within the first 30 to 90 days, when insurers have the most flexibility. After that, rules often become stricter depending on the state or province. At five months, whether this is allowed depends heavily on local law and the reason given.

No Federal Rule

In the U.S., there’s no single federal law governing home insurance cancellations. Rules are set at the state level. In Canada, it’s similar—each province sets its own regulations, notice periods, and acceptable reasons.

Some Areas Are Stricter Than Others

States like California and New York often restrict cancellations after about 60 days unless there’s nonpayment, fraud, or major risk changes. Other states may allow more flexibility early in a policy, but become stricter later. Canadian provinces also vary.

Provincial Differences In Canada

Provinces like Ontario, Alberta, and British Columbia require written notice and valid reasons for cancellation. Typical notice periods range from 5 to 30 days depending on the situation and policy terms.

Notice Is Required

Insurance companies are generally required to give written notice before canceling a policy. The notice period is often 10 to 30 days, depending on the reason and local regulations, though some areas require longer notice.

The Reason Must Be Stated

They can’t just cancel without explanation. The insurer must provide a reason for the cancellation, such as underwriting issues, property risk, or policy eligibility problems like secondary home status.

They Can’t Just Keep Your Money

If an insurer cancels your policy mid-term, they are typically required to refund the unused portion of your premium. You shouldn’t be paying for coverage you’re no longer receiving, especially after paying the year upfront.

Refunds Are Usually Prorated

In most cases, you’ll get a prorated refund based on how much time was left on the policy. If you paid for a full year and they cancel after five months, you should receive the remaining balance back.

This Doesn’t Mean You Did Anything Wrong

Situations like this are frustrating, but they don’t mean you made a mistake. You disclosed the information—you just ran into the insurer’s internal rules or changing risk tolerance.

You May Have Other Coverage Options

Not all insurers treat secondary homes the same way. Some specialize in them or are more flexible, especially if the property is maintained, monitored, or occasionally occupied.

Vacant vs Secondary Home Matters

There’s a difference between a secondary home and a vacant one. If the home is completely unoccupied, fewer insurers will cover it, and the requirements can be stricter.

You Might Need a Specialty Policy

In some cases, you may need a specific type of coverage designed for seasonal, rental, inherited, or unoccupied homes. These policies often cost more but are built for this exact situation.

What You Should Do Next

Start by reviewing the cancellation notice and your original policy. Confirm the reason, check the refund amount, and look at the timeline. Then begin shopping for a new policy as soon as possible.

Consider Calling the Insurer Directly

Sometimes you can clarify or even reverse a cancellation by speaking with the company. If the issue is documentation or misunderstanding, there may still be a chance to resolve it.

Document Everything

Keep records of your communications, policy documents, and payment receipts. If there’s ever a dispute over the cancellation or refund, having a clear paper trail can make a big difference.

So…How Is This Allowed?

It comes down to the fine print and local laws. Insurance contracts and regional regulations give companies flexibility, especially early in a policy. It feels unfair—but in many cases, it’s legally built into how these policies work.

You Might Also Like: