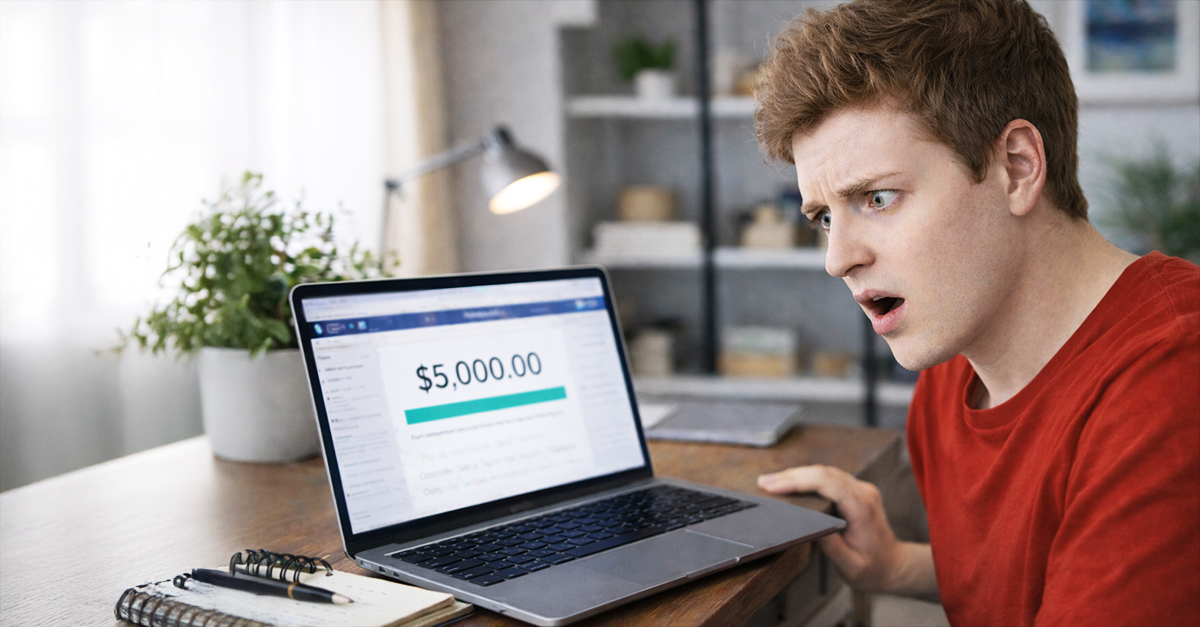

A Windfall You Didn’t Want

You log into your bank account and see an unexpected $5,000 deposit. At first, it feels like a mistake or even a good luck windfall. But then a stranger called, claiming that the money was sent by accident, and asks you to return most of it through Zelle. Now you’re understandably hesitant to send anything under the growing suspicion that this is some kind of scam.

This Is A Well-Known Scam Pattern

The situation described here closely matches a common overpayment or accidental transfer scam. In these situations, scammers send money and then quickly ask for a portion back. The urgency is set up to push you into doing something before you fully understand what’s going on.

Why The Money Might Not Be Real

The original $5,000 may come from a compromised account or fraudulent source. Even if it shows up on your balance, it can later be reversed by the bank once fraud is detected. That means the money isn’t truly yours to keep or safely return.

How The Trap Actually Works

If you send $4,500 back using Zelle, that transaction is typically final. Later, when the bank reverses the original fraudulent deposit, you lose the entire $4,500 you sent. The scammer pockets the real money, while you are left covering the loss.

Zelle Transfers Are Hard To Reverse

Zelle payments are designed to work like cash. Once you send money, it’s extremely difficult to recover unless the recipient voluntarily returns it. This is why scammers prefer using Zelle for these schemes.

The Caller Puts Pressure On

Scammers often call soon after the deposit is made and create a sense of urgency. They may claim they made a mistake or that they need the money immediately. This pressure is deliberate and is intended to stop you from contacting your bank first.

It Could Also Be A Fake Payment

In some cases, the deposit you see isn’t even real. Scammers can sometimes send fake notifications or manipulate timing so that the funds appear temporarily. They rely on you sending real money back before the system corrects itself.

Never Send Money Back Directly

You should never send money "back" to someone who contacts you unexpectedly about a deposit. Even if the situation seems legitimate, the best and safest process to take is to let the banks handle it. Sending money yourself puts you at significant risk.

Let The Bank Handle Any Reversal

If the deposit was truly accidental, the sender can work with their bank to reverse the transaction. Financial institutions have formal processes for correcting mistakes. It’s not your responsibility to fix it manually.

Get In Touch With Your Bank Immediately

As soon as you notice the deposit and the request, contact your bank directly using official channels. Explain what happened and ask them for guidance. This helps protect you and creates a record of the situation.

Report The Incident As Potential Fraud

Most banks and payment platforms encourage reporting suspicious activity right away. Zelle specifically advises their users to contact their bank if they at all suspect fraud.

Don’t Spend The Money

Even though the funds are showing in your account, you should treat them as temporary. Spending the money could cause complications if the bank later removes it. Keeping the funds untouched is the safest approach.

Understand How Liability Works

If you voluntarily send money through Zelle, even under pressure or deception, it may be considered an authorized transaction. This can make it a lot harder to recover your funds compared to unauthorized fraud.

Why Banks Sometimes Don’t Refund Losses

Federal rules generally require banks to refund unauthorized transactions, but scams often fall into a gray area. If you initiate the payment yourself, even as a result of deception, reimbursement isn’t always guaranteed.

Scammers Often Use Stolen Accounts

The original $5,000 may have been sent using stolen banking credentials. Once the real account holder reports the fraud, the bank reverses the transaction. That reversal doesn’t undo any money you sent to the scammer of your own accord.

Warning Signs You Shouldn’t Ignore

Unexpected deposits, urgent requests for repayment, and instructions to use fast payment methods are all red flags. If someone insists on immediate action or discourages you from contacting your bank, especially if it’s a stranger on the other end of the line, that’s a strong indicator of a scam.

Keep All Communication Records

Save any messages, call logs, or transaction details related to the incident. This documentation can be useful if your bank investigates the matter or if you need to file a report with authorities.

Consider Filing A Report With Authorities

If you think you’re being targeted by a scam, you can report it to agencies like the Federal Trade Commission or the FBI’s Internet Crime Complaint Center. This helps track patterns and may be of assistance in broader investigations.

What To Do If You Already Sent Money

If you already transferred funds, contact your bank immediately and explain what happened. While recovery isn’t guaranteed, acting quickly gives you the best chance of limiting your losses.

Turn A Scare Into A Lesson

Situations like this are stressful, but they highlight how modern scams operate. By recognizing the warning signs and refusing to act under pressure, you protect yourself. When in doubt, pause, verify, and let your bank take care of anything involving unexpected money.

You May Also Like: