You Co-Signed For Your Cousin, Now He's Skipped Town, What's Next?

Co-signing a lease for someone can seem like a nice thing to do, particularly if they're your family—you're helping them out, right? Well, not in this case. If your cousin who's never been much of a person of their word has decided to skip town on a lease that you co-signed, you're up the creek without a paddle. Here's how to handle it.

Understand The Weight Of A Co-Signer Agreement

When you co-sign a lease, you’re not just vouching for someone—you’re accepting full legal responsibility. If your cousin stops paying, you’re on the hook for the entire rent and any damages. This agreement gives the landlord the legal right to pursue you for payment, even if you never lived there. It’s important to acknowledge this legal reality from the outset.

Don’t Ignore Communication From The Landlord

Whatever you do, don't ignore the landlord's attempts to contact you. This will not be a good look for you if the matter proceeds to court. Try to reply promptly to their texts, emails, or phone calls. Ghosting is a bad idea.

Request A Copy Of The Lease Agreement

Ask the landlord for a copy of the lease agreement if you don't already have one. This will provide clarity on what you signed up for. This is your right as a signee, so don't let you landlord refuse to give you one.

Confirm That Your Cousin Has Actually Abandoned The Lease

Before assuming the worst, ask the landlord for evidence that your cousin truly abandoned the property. Sometimes, a delayed payment or a misunderstanding can be mistaken for desertion. Did your cousin return the keys or leave their belongings behind? Clarifying this status is critical because your liability may differ if the lease is still technically active.

Document All Communication In Writing

Start saving every interaction related to this issue—emails, text messages, call logs, or even handwritten notes. Create a folder or digital archive. These records can become vital if the situation turns into a legal dispute or if you later pursue your cousin for reimbursement. Being organized with documentation can also make you appear more credible and cooperative to the landlord or a judge.

Ask The Landlord For A Full Breakdown Of Charges

Before paying anything, ask for an itemized statement showing exactly what is owed. This should include missed rent, late fees, utility charges, and any damage costs. Scrutinize the details—landlords occasionally inflate numbers. If the charges seem suspicious, request receipts or documentation. Knowing exactly what you’re dealing with makes negotiation and financial planning far more manageable.

Try To Contact Your Cousin Directly

Even if your cousin has gone silent, it’s worth making one last effort to reach out. Use email, phone, social media, or mutual contacts. Let them know the landlord is pursuing you and request that they take responsibility. Keep your tone civil and non-threatening—your goal is to get their cooperation, not to burn bridges. Save proof of your attempts to contact them.

Consider Making A Payment To Avoid Escalation

If the amount owed is relatively small, paying the balance—even if it feels unfair—might be the best way to prevent bigger problems. This may stop the landlord from filing a lawsuit or reporting the lack of payment to your credit agency, which can decimate your credit score.

Check Your Credit Report For Any Red Flags

Because you're a co-signer, missed rent payments can damage your credit even if you weren’t living in the unit. Get a free copy of your credit report from all three bureaus. Look for late payments, collection notices, or new accounts tied to the lease. Early detection allows you to take steps to dispute or repair any unjust entries.

Explore Whether Renters’ Insurance Covers Anything

Though not common, renters’ insurance might offer some coverage if the damage or loss involves theft, vandalism, or natural disaster. If either you or your cousin had a policy, review it to see if it helps reduce the amount owed. It’s a long shot, but one that may provide financial relief—especially if property damage is part of the landlord’s claim.

Ask The Landlord About Subletting Or Reassigning The Lease

If the property is still under lease, see if the landlord will allow you to find a replacement tenant. Subletting or assigning the lease can mitigate your liability going forward. Be sure to get approval in writing, and make sure the new tenant signs a formal agreement. While it won’t fix past debt, it can prevent future losses.

Negotiate A Settlement With The Landlord

Most landlords don't want to take you to court. Try and settle with the landlord for part of the money first. As you co-signed the lease, you don't have a lot of leeway here: try to cough up some of the money.

Consult A Local Tenant Rights Organization

If your community has a tenant's rights organization, you'd be well served to consult with them about what options you have. Their employees may be able to speak to the landlord on your behalf.

Talk To A Lawyer If The Amount Is Large

If the landlord threatens to sue you, you should immediately consult an attorney or law student. You may pay a small fee for their services, but even a single consultation can help you understand your options. An attorney may also spot lease violations or procedural flaws that could reduce or eliminate your liability.

Consider Suing Your Cousin In Small Claims Court

If you end up paying part or all of the debt, you may be able to sue your cousin for reimbursement. Small claims court is designed for cases like this and doesn’t require a lawyer. Bring all your records—proof of payment, the lease, messages showing their abandonment—to build a strong case. You deserve to be made whole if you were left holding the bag.

Evaluate Whether A Debt Management Plan Is Needed

Unfortunately, it's not uncommon for debt like this to bleed into your other finances. If your cousin refuses to pay you back, you'll be saddled with the debt and will need to come up with a debt management plan. If you think you can pay it back in one fell swoop, do so. If not, create a budget that incorporates the debt repayment.

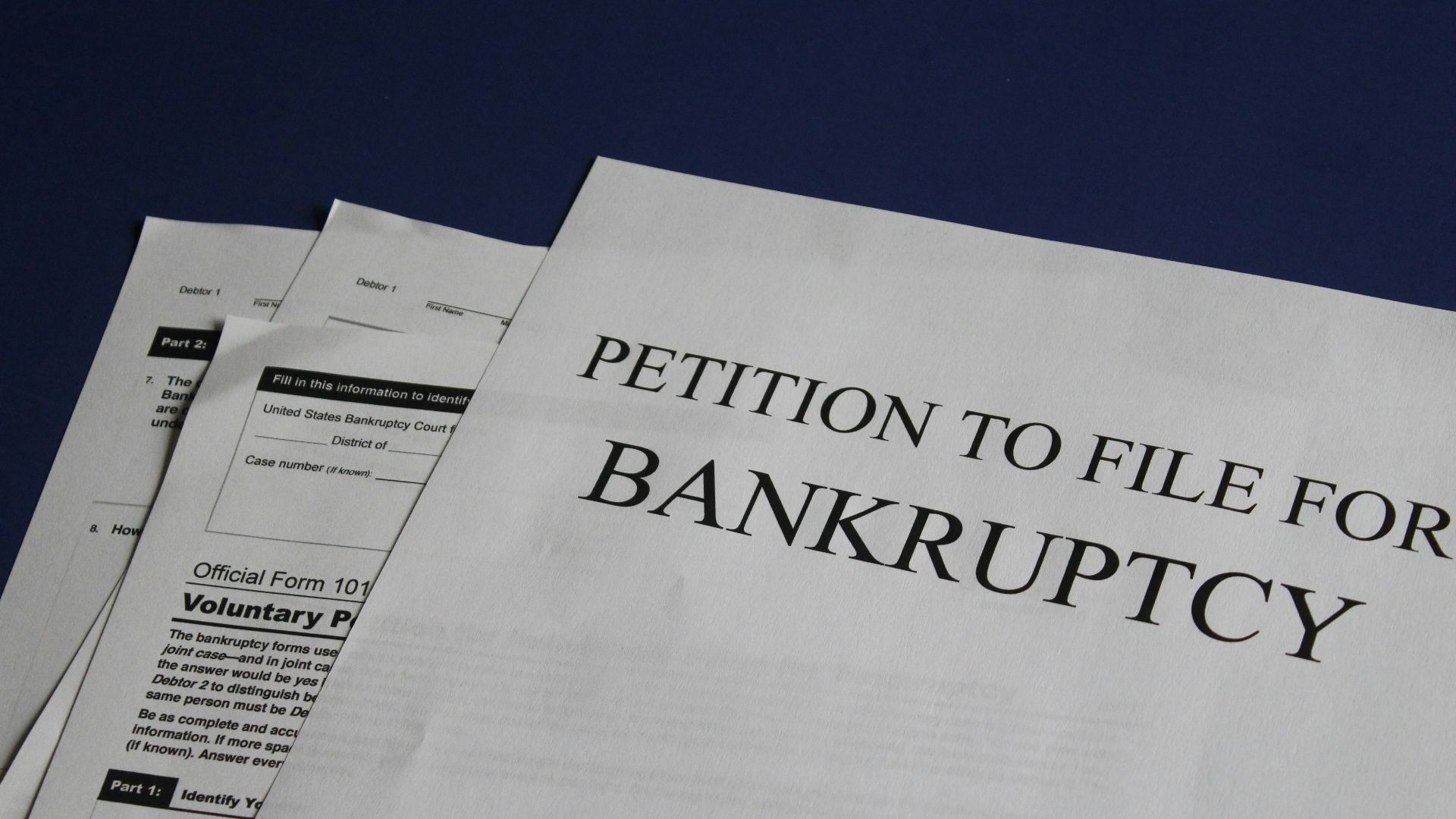

Research Whether Bankruptcy Could Apply

Bankruptcy is a last resort for most people, but it could be a good option for your situation. If your cousin has left you with a huge bill and has skipped town, your only option might be to declare bankruptcy to wipe out the debt. Consult with a bankruptcy lawyer to see if this is the right path forward.

Never Co-Sign Again Without Extreme Caution

Let this experience serve as a warning: co-signing is not just a favor—you are legally bound to fulfill the obligations of the lease. Are you willing to take the risk again? We think not. Use extreme caution before ever co-signing a lease for someone again.

Educate Others On The Risks Of Co-Signing

Many people don’t understand that co-signing means full responsibility—not just moral support. Share your story with friends, family, or online communities. You could prevent someone else from making the same mistake. Public awareness can go a long way toward helping others make informed financial decisions.

Take Steps To Repair Your Credit And Move Forward

Once the immediate crisis is handled, shift focus toward rebuilding. Make on-time payments, reduce outstanding debt, and consider a secured credit card to re-establish creditworthiness. Monitor your credit report regularly. A few months of responsible behavior can begin to undo the damage and set you on a healthier financial path.

You May Also Like:

Fast Food Toys From The 80s & 90s That Are Collectible Gold

These Early Cell Phones Have Become Collector's Items Worth Big Money

My Retirement Fund Is $700K, Should I Pay Off My $120K Mortgage?