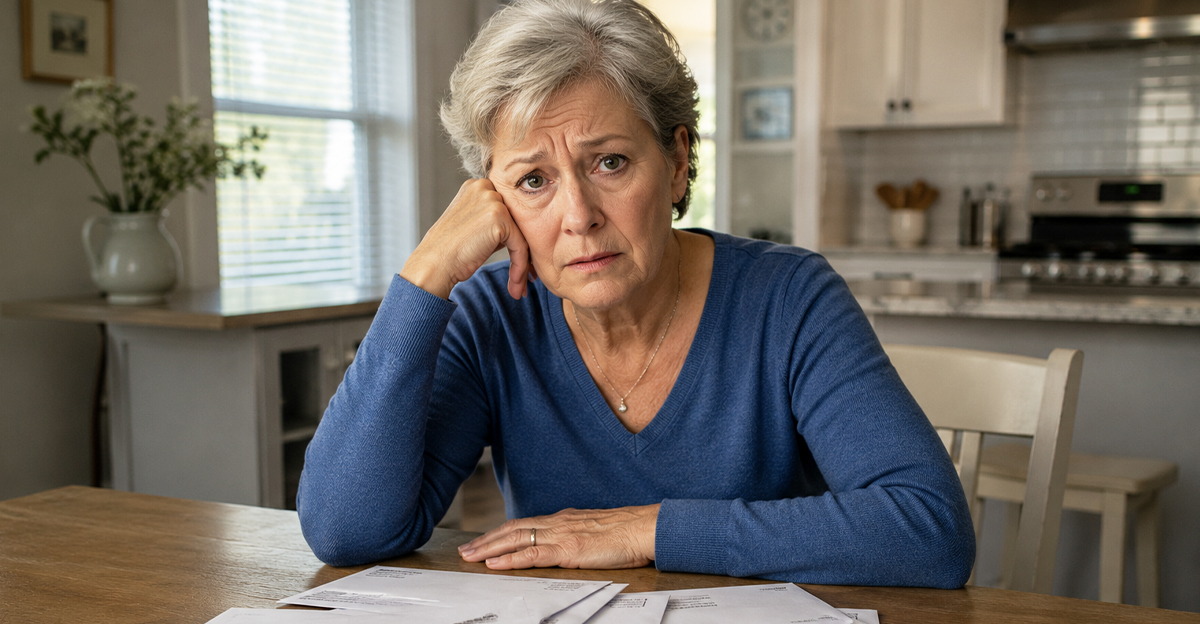

Situation Report: Urgent

You’ve got an emotionally loaded dilemma on your hands: your wife wants to rescue her brother’s struggling business, and she sees your retirement fund as the solution. You recognize how irreplaceable those savings are at this stage of life. Before you start yelling and screaming and flying off the handle, step back, take a deep breath, and make an objective assessment of what’s really at stake here.

Separate Love From Financial Reality

It’s understandable that your wife wants to help her brother, but she has to separate compassion from financial risk. A failing business rarely turns around because someone made an 11th-hour infusion of cash. Using retirement savings might put off the final collapse briefly but it could permanently jeopardize your future security in the process.

Understand The True Health Of The Business

Before you make any rush decisions, insist on reviewing all the business’s financial statements such as profit-and-loss reports, debts, vendor obligations, payroll records, and tax liabilities. There’s nothing personal in doing this, it’s just due diligence. A long-term decline is a strong indicator that new money won’t solve the real underlying problems.

Ask For An Honest Business Assessment

Encourage your wife and her brother to meet with a small-business accountant or advisor. An outside expert can make an objective evaluation of whether the business is salvageable or whether it has structural weaknesses that no cash windfall will fix. This backs your case and protects the two of you from risk.

Assess The Risk To Your Retirement Timeline

Every dollar pulled out of your retirement accounts sacrifices compound growth, may trigger penalties, and undermines your long-term financial stability. By the time you’re in your 50s or 60s, rebuilding those depleted retirement funds becomes increasingly difficult. Your financial security has to remain the top priority, especially as the years roll by.

Look At Alternative Ways To Help

Instead of throwing around large sums of cash that you can ill afford, you might suggest helping your brother-in-law reorganize his operations, cut expenses, negotiate with vendors, or apply for grants and relief programs. These are the options that offer real assistance without putting your retirement funds on the line. You’re not refusing help; you’re offering safer support.

Build A Wall Around Your Retirement Funds

You’re allowed to draw a firm boundary, even with close family members: retirement savings should never be used to bail out others. Marriage requires shared financial responsibility, and protecting your long-term security as a couple is essential. Calmly reinforce that your retirement accounts are off limits for this purpose.

Talk About The Emotional Layer

Your wife may feel emotionally responsible for her brother, especially if their family has a history of financial insecurity. Acknowledge her feelings while gently reminding her that risking your shared retirement for an unstable business is neither sustainable nor fair.

Avoid Being The Back-Up Plan

If her brother is turning to you because banks and lenders have already denied his applications for more credit, that’s a major red flag. Banks don’t just fork over large sums of money; they reject high-risk borrowers for a reason. Family members often become the next target for funds, but that’s an even bigger sign that you need to avoid becoming his lender of last resort.

Think Of The Impact On Your Marriage

Money stress can strain a relationship to the breaking point. Frame your concerns as protecting your shared future; don't rip into her brother for his irresponsible ways. Emphasize long-term goals: 'I want us to retire securely, and this decision affects our future together.' Focus on unity, not pointing the finger of blame.

Talk To A Financial Advisor Together

A neutral advisor can explain the long-term damage that using retirement funds could cause. They can provide projections and models that show how a big withdrawal like this could derail your retirement timeline; it may help bring your wife back down to Earth.

Understand The Legal Consequences

Here’s another important question: if money is given, is it a loan or a gift? Without a contract, collateral, or repayment terms, you may never see the money again. Even with agreements, repayment is uncertain. Treat this as a formal financial transaction, not a family obligation.

Does The Business Have A Path Forward?

Is your brother-in-law’s industry declining? Are office supply stores losing relevance due to online competition? If the business model is outdated, pouring more money into it won’t fix structural shortcomings. Evidence, not optimism, should be driving decisions.

Mr. Satterly, Wikimedia Commons

Mr. Satterly, Wikimedia Commons

Protect Yourself From High-Pressure Decisions

Struggling business owners often push for quick financial help. Don’t allow panic to overrule careful thinking. Any decision involving your retirement funds deserves slow, deliberate review. In fact, you shouldn’t be going that route at all. Step back, gather information, and don’t let anyone rush you.

Consider Offering Only What You Can Afford To Lose

If you absolutely feel compelled to help, settle on an amount you’re comfortable losing entirely, without even touching retirement funds. Make it clear that any assistance is a one-time contribution, not a revolving line of credit or ongoing bailout.

Look For Objective Warning Signs

Unpaid invoices, mounting debt, delayed payroll, declining customers, and repeated 'temporary setbacks' are all warning signs of serious distress. These signs show your retirement money would probably disappear pretty quickly without changing outcomes. Evidence supports your refusal.

Reframe The Conversation With Your Wife

Shift the question from 'Should we help my brother?' to 'How do we protect our own future?' People often agree on the long-term goal of financial stability even if they don’t see eye-to-eye on specific actions. Unite around your shared hope for a sound and secure future.

Make A Joint Retirement Plan

Use this moment to clarify your retirement goals together: contribution targets, lifestyle expectations, and long-term financial priorities. When you’re both on the same page with this stuff, it makes it a lot harder for outside pressures to interfere with your plans or influence decisions.

Vodafone x Rankin everyone.connected, Pexels

Vodafone x Rankin everyone.connected, Pexels

Get Ready For Emotional Pushback

Your wife might feel guilt or family pressure. Expect emotional reactions, but stay calm and stick to your original plan of action. Reinforce that your retirement savings are for your future, and not a bailout fund. Maintaining this boundary protects both of you.

Protect Your Future By Saying No

Your Number One responsibility is to your financial wellbeing and your shared life. You can still care about your brother-in-law while refusing to jeopardize your future. Saying no isn’t selfish; it’s your only practical option. Protect your retirement with confidence and clarity.

LinkedIn Sales Navigator, Pexels

LinkedIn Sales Navigator, Pexels

You May Also Like: