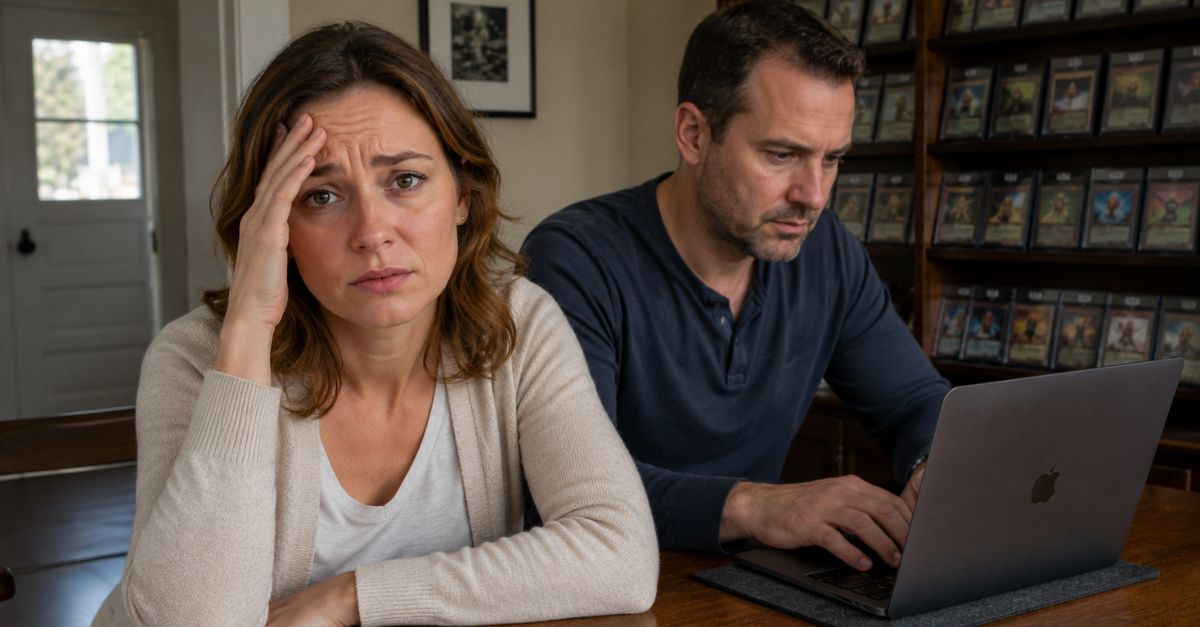

When a Treasure Hunt Starts to Look Like a Spending Habit

When a collector, especially one who knows their stuff, says, “It’s an investment,” they can be convincing. Every day there's a new story about a watch, trading card, comic, or limited-edition figurine selling for a huge amount. But if the value of your spouse's collection is hard to pin down, the costs keep adding up, and you never see any cash coming in, it's time for a serious conversation.

Collectibles Can Be Real Assets

Collectibles are not automatically a bad financial move. The IRS treats many items such as art, rugs, antiques, metals, gems, stamps, coins, alcoholic beverages, and certain other tangible personal property as collectibles for tax purposes. That alone shows these items can hold value, but it does not mean every purchase is a smart investment.

The IRS Has a Very Specific Definition

Under IRS rules, gains on collectibles held for more than one year can be taxed differently than stocks and bonds. The maximum federal tax rate on collectible gains is generally 28%, which is higher than the long-term capital gains rate many investors expect on traditional assets. So even when a collectible goes up in value, taxes can take a bigger cut.

The First Big Test Is Simple

If your husband says he is investing, ask one basic question: what is the plan to make money. A real investment case should explain what he bought, why it should go up in value, what comparable sales back that up, what fees are involved, and when he would actually sell.

An Investment Needs a Market Price

Stocks have prices posted all day, but collectibles usually do not. Their value often comes from auction results, dealer listings, grading reports, and buyer demand at a specific moment. If he cannot point to recent comparable sales from credible marketplaces or auction houses, the claimed value may be more wishful thinking than fact.

Illiquidity Is Where the Story Often Falls Apart

A collectible may be “worth” a certain amount on paper and still sit unsold for months. That is illiquidity, and it matters because an asset is only really useful if it can be turned into cash when needed. In a household budget crunch, a shelf full of niche memorabilia is not the same thing as money in the bank.

Gary Dunaier, Wikimedia Commons

Gary Dunaier, Wikimedia Commons

Costs Quietly Eat the Return

Collectors often focus on the purchase price and ignore everything that comes after: grading, insurance, storage, shipping, repairs, and auction commissions. Those costs can be steep, especially for cards, coins, watches, art, and vintage toys. If the item has to jump a lot in value just to break even, the investment argument gets shaky fast.

Nelson Pavlosky , Wikimedia Commons

Nelson Pavlosky , Wikimedia Commons

Even Experts Warn About Friction

The Securities and Exchange Commission has warned investors about assets that are hard to value and hard to sell. The SEC is not a collectibles price guide, but its warnings about illiquidity, murky pricing, and sales hype fit this market too. If a purchase depends more on excitement than evidence, it deserves a closer look.

The Resale Price Is Not the Asking Price

One of the easiest mistakes in collectibles is confusing listed prices with completed sales. A seller can ask anything online. What matters is what buyers actually paid, and how recently they paid it, on platforms with transparent records.

Recent Sales Matter More Than Old Glory

That mint-condition comic that exploded in 2021 may not fetch the same number today. Collectibles move in cycles, and markets can cool off quickly after a hype run. A serious buyer should be tracking current sales data, not repeating a headline from the peak years.

Hype Can Make Ordinary Shopping Feel Sophisticated

Scarcity, limited drops, celebrity ownership, and online communities can create a rush that feels financial. Behavioral finance research has long shown that excitement, fear of missing out, and overconfidence can shape buying decisions. If the thrill of the hunt is doing most of the work, that is a clue the purchase may be more emotional than economic.

Passion Investing Is Still Spending

There is nothing wrong with spending money on something you love, as long as the household can afford it and the spending is called what it is. Trouble starts when discretionary buying gets dressed up as careful investing. Calling a purchase an asset does not automatically make it one.

Ask Whether He Ever Sells

A useful dividing line is whether he has a repeatable process for taking profits. Real investors eventually sell some holdings, review returns, and compare the results with other options. If everything gets stored, displayed, and defended forever, the collection may be acting more like consumption than investment.

Track the Collection Like a Portfolio

If he wants to call it investing, ask him to keep a spreadsheet. It should include purchase date, purchase price, taxes, shipping, grading fees, insurance, storage costs, and current estimated resale value based on recent comparable sales. That exercise alone often reveals whether the collection is actually making money.

Net Worth Is Not the Same as Cash Flow

A collection may boost household net worth on paper while still putting pressure on the monthly budget. If expensive purchases are crowding out retirement contributions, emergency savings, debt payoff, or family goals, that is a red flag. A good investment should not leave the rest of the financial plan struggling.

Opportunity Cost Is the Quiet Killer

Every dollar tied up in collectibles is a dollar not compounding somewhere else. Broad stock market index funds, high-yield savings accounts, and retirement accounts offer transparency, diversification, and easier access to cash. A collectible should be judged not just by whether it might go up, but by whether it can beat the alternatives after all costs and taxes.

Diversification Still Matters at Home

If one person in a couple pours a big share of extra cash into one niche category, household risk goes up. That is especially true when the market depends on trends, condition, buyer tastes, and discretionary spending. A concentrated pile of comics or watches is not a substitute for a diversified investment plan.

Fraud and Counterfeits Are Not Small Risks

Counterfeit goods and misrepresented condition have plagued many collectible markets for years. Authentication and grading can help, but they do not remove every risk, and they add cost. If your husband is buying from questionable sellers or relying on social media claims, the odds of an expensive mistake rise.

Insurance Is a Reality Check

Insuring valuable collectibles can be smart, but it also forces a conversation about appraisals, documentation, and real market value. If the items are too valuable to leave uninsured, that is another ongoing expense. If they are not valuable enough to justify the cost, the investment case may be thinner than it sounds.

Watch the Household Warning Signs

The point where investing turns into shopping often shows up in daily life before it shows up on a balance sheet. Are bills being delayed, savings goals ignored, credit card balances carried, or arguments breaking out after each purchase? Those signs matter more than any story about what an item might be worth someday.

Debt Changes the Equation Fast

Buying speculative collectibles while carrying high-interest credit card debt is usually a losing trade. Credit card APRs can easily outpace likely collectible returns after fees and taxes. In that situation, the purchases are usually consumption with a very expensive financing charge attached.

Set a Household Policy Before the Next Purchase

Couples usually do better when they decide the rules ahead of time. That can mean a monthly collectible budget, a dollar threshold that requires joint approval, or a rule that retirement and emergency savings must be funded first. Boundaries reduce fights because each purchase becomes a policy question instead of a personal battle.

Create a Sell Rule, Not Just a Buy Rule

Many collectors have detailed reasons to buy and no rules for when to exit. Consider setting criteria such as selling when an item rises by a certain percentage, when market demand fades, or when the collection grows beyond a target allocation. An investment strategy without an exit plan is usually just accumulation.

Use a Simple Three-Part Test

Ask whether the purchase has verifiable market data, a realistic path to resale, and a clear place within the household financial plan. If the answer to any of those is no, be careful. If all three are missing, it is probably shopping.

There Is Nothing Wrong With Calling It a Hobby

In fact, that label can be healthier and more honest. Hobbies bring enjoyment, identity, community, and pride, even when they do not outperform the S&P 500. The trouble starts only when a hobby is used to justify spending the household cannot comfortably absorb.

The Best Compromise Is Often a Split Approach

One practical fix is to separate collection money from investment money. Fund retirement accounts, emergency savings, and core goals first, then carve out a fixed amount for discretionary collecting. That keeps the fun while protecting the family balance sheet.

So When Is It Just Shopping?

It is just shopping when the purchases lack a documented thesis, reliable comparable sales, liquidity, and a sell plan, or when they undermine bigger financial priorities. It is also shopping when the emotional payoff of owning the item is clearly the real point. There is nothing shameful about that, but there is a lot to gain from calling it what it is.