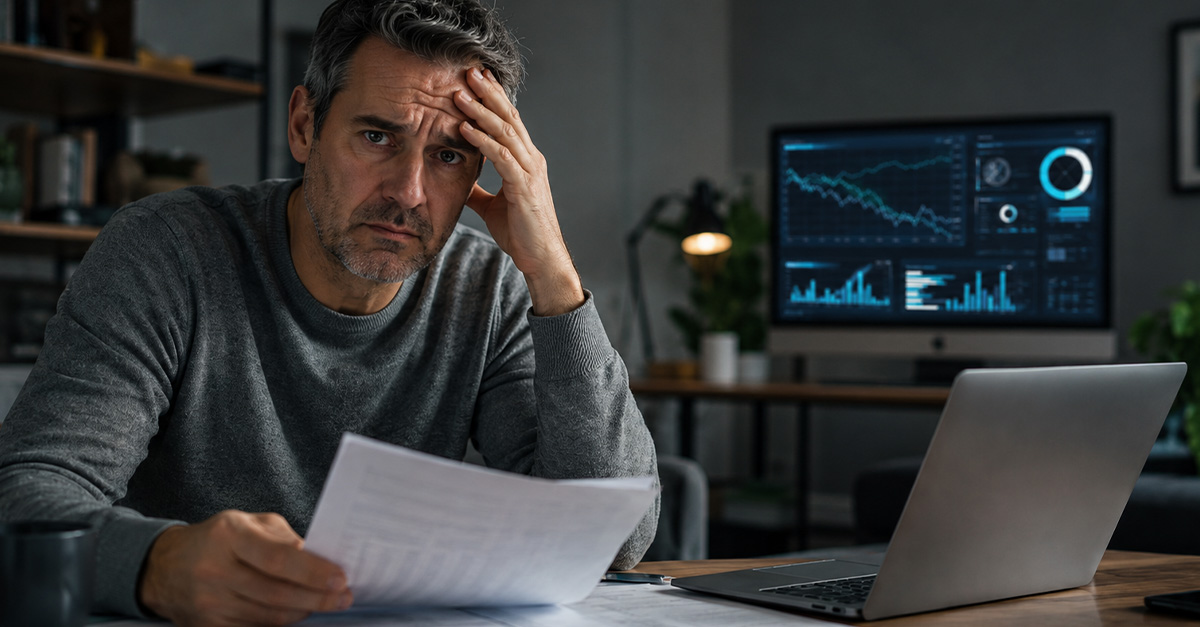

The AI Gave Me A Sunny Forecast

AI can do a lot of impressive things, but it still cannot see the future. If you asked a chatbot or retirement calculator how long your savings would last and it gave you a comforting answer, only for real life to laugh in your face, you are not alone.

First, Don’t Panic

Running out of money in retirement sounds terrifying because, well, it is serious. But panic is not a plan. The first step is to slow down, gather the facts, and figure out whether this is a five-alarm emergency or a problem with room to maneuver.

AI Is A Tool, Not A Crystal Ball

AI can make projections based on the numbers you feed it, but retirement is packed with surprises. Markets fall, medical bills pop up, rent rises, cars break, and inflation does not politely ask permission before eating your grocery budget.

Find The Bad Assumption

Before you blame yourself, look for the assumption that broke the plan. Did the AI expect higher investment returns? Lower spending? A shorter retirement? No health surprises? A paid-off home? Finding the weak spot helps you fix the right problem.

Rebuild Your Real Budget

Now it is time for a kitchen-table budget, not a fantasy spreadsheet. List what you actually spend each month, including boring things like insurance, prescriptions, taxes, gifts, repairs, streaming services, and that “small” coffee habit that somehow became a subscription.

Separate Needs From Nice-To-Haves

This part is not fun, but it is powerful. Housing, food, health care, insurance, transportation, and utilities are needs. Travel, restaurant meals, upgrades, gifts, and hobbies may still matter deeply, but they are places where cuts can buy time.

Calculate Your Runway

Take your current savings and divide it by your realistic yearly shortfall. That gives you a rough runway. It will not be perfect, because investments move and expenses change, but it tells you whether you need small tweaks or big action.

Check Your Withdrawal Rate

If you are pulling too much from your savings each year, the account can drain faster than expected. A lower withdrawal rate may stretch your money, but it often requires lifestyle changes. This is where brutal honesty beats wishful math.

Look At Social Security Timing

Social Security can be a major piece of retirement income. If you have not claimed yet, claiming age matters. Delaying benefits past full retirement age can increase monthly benefits up to age 70, but the right move depends on your health, income, savings, and needs.

Review Every Income Source

Make a full list of income: Social Security, pensions, annuities, rental income, dividends, part-time work, retirement accounts, and any spouse or survivor benefits. People sometimes forget small income streams that can make a real difference when stacked together.

Consider Part-Time Work

No one dreams of “unretiring,” but part-time work can be a lifeline. Even modest income can reduce withdrawals, delay draining savings, and add structure to the week. Consulting, tutoring, seasonal retail, bookkeeping, pet sitting, or remote work may help.

Cut The Big Three First

Tiny cuts help, but housing, transportation, and health care usually drive the budget. Downsizing, getting a roommate, moving to a lower-cost area, selling an extra car, or reviewing insurance can do more than canceling every pleasure in your life.

Don’t Ignore Housing Options

Housing is often the biggest retirement expense. Renting out a room, moving closer to family, downsizing, refinancing carefully, or exploring senior housing programs may help. None are easy choices, but a house-rich, cash-poor retirement can become stressful fast.

Watch Out For Debt

Debt can quietly wreck a retirement plan. Credit cards, personal loans, car payments, and medical debt all compete with groceries and utilities. Focus on high-interest debt first, and do not use retirement withdrawals casually without understanding taxes and penalties.

Check For Benefits You Missed

Many retirees qualify for help and never apply. Look into property tax relief, utility assistance, prescription help, food assistance, Medicare savings programs, veterans benefits, and local senior services. Pride should not stop you from using programs built for this exact moment.

Talk To A Real Professional

An AI answer can be useful, but this is where a human professional earns their chair. A fee-only financial planner, tax professional, or accredited credit counselor can help test scenarios, manage withdrawals, and avoid expensive mistakes.

Get Tax Advice Before Big Moves

Selling investments, withdrawing from retirement accounts, converting accounts, or selling a home can all have tax effects. One move that looks brilliant in a chatbot window can create a surprise bill later. Ask before you act, not after.

Understand Required Withdrawals

Some retirement accounts require minimum distributions once you reach the required age. These rules matter because they affect taxes and cash flow. If you have traditional IRAs or workplace plans, make sure your withdrawal plan fits the current rules.

Revisit Your Investments

Running out of money does not always mean you should gamble for higher returns. Taking wild risks late in retirement can backfire badly. Instead, review whether your investments match your age, goals, spending needs, and emotional tolerance for market swings.

Avoid Miracle Solutions

When people are scared, scammers smell opportunity. Be suspicious of guaranteed high returns, secret strategies, pressure to act immediately, or anyone who says they can “fix” retirement overnight. Desperation is expensive when the wrong person gets involved.

Consider Annuities Carefully

An annuity can sometimes turn savings into predictable income, but the details matter. Fees, surrender charges, inflation protection, and insurer strength all count. Do not buy one just because someone used comforting words and a glossy brochure.

Bring Family Into The Conversation

Money stress loves secrecy. If trusted family members may be affected, tell them early. Adult children, siblings, or close friends might help with housing, transportation, paperwork, or planning. You do not need to hand them control, but support can matter.

Build A Crisis Plan

If the numbers are truly tight, make a crisis plan now. Decide what bills get paid first, what expenses can stop immediately, what assets could be sold, and who you would call. A plan is calmer than a scramble.

Update The Plan Regularly

Retirement planning is not a one-time fortune cookie. Recheck the numbers every few months, especially after market swings, medical changes, big expenses, or benefit updates. The goal is not perfection. The goal is catching problems early.

Keep Some Joy In The Budget

A survival-only retirement can feel punishing. Even while cutting back, protect a few affordable joys: library books, walks, potlucks, community events, gardening, volunteering, or coffee with friends. Retirement should not become a punishment for bad software.

The AI Was Wrong, But You’re Not Done

The AI gave you a bad map. That does not mean the road is gone. With a real budget, professional help, smarter withdrawals, possible income, and honest cuts, you may still have options. The sooner you act, the more choices you keep.

You May Also Like: