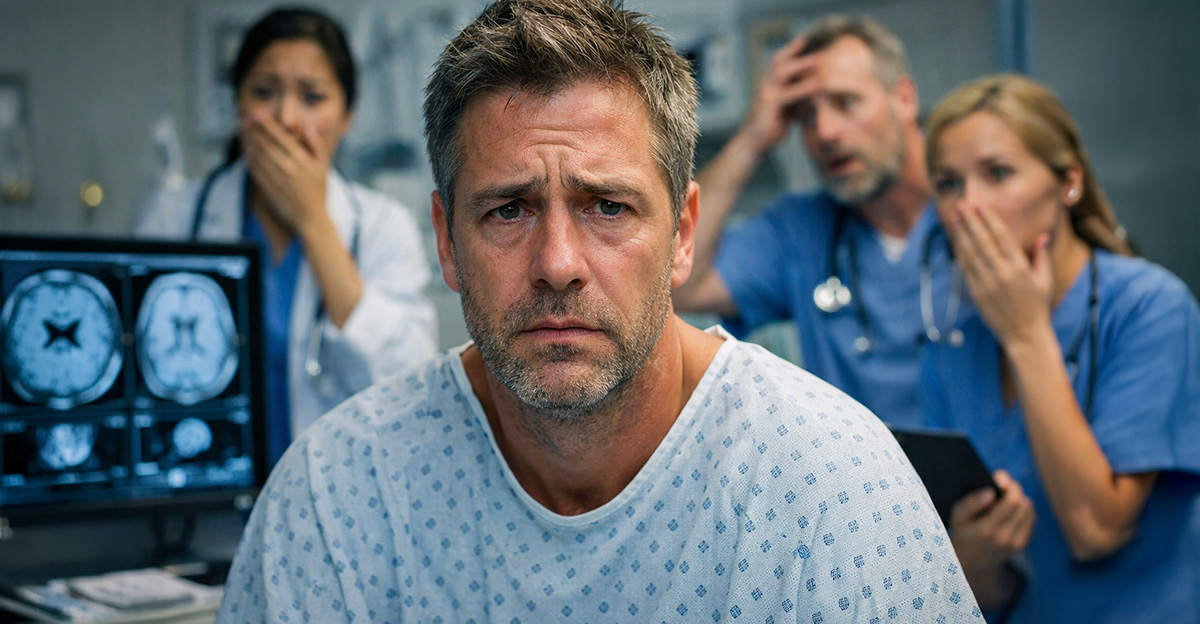

The Day After The End Of The World

Last year, you were told the kind of news that turns your bones to ice: you had a terminal illness. So you did what many people would do when the future suddenly looked painfully short—you stopped planning for later and started reacting to now. You sold the house, the car, the furniture, the keepsakes, maybe even the “good dishes” nobody was allowed to touch. Now the doctors say it was a misdiagnosis, and you are very much alive, very much here, and very much staring at the wreckage of decisions made under a terrifying lie.

First, Take A Breath

Before you do anything practical, give yourself permission to feel wildly confused. Relief, anger, grief, embarrassment, rage, exhaustion—this is not an overreaction cocktail, it is the normal human response to emotional whiplash. You do not need to be “grateful it all worked out” on anyone else’s timeline. It did not all work out neatly, and pretending otherwise will only make the cleanup harder.

You Made Decisions Under Extreme Duress

Let’s be very clear about one thing: you were not reckless, foolish, or dramatic. You were operating under the belief that your life was ending. That changes the math on everything. Selling assets, cashing out accounts, giving things away, and abandoning long-term plans can all seem completely rational when you think time is running out. That matters, emotionally and sometimes legally too.

Get The Full Medical Record

Your first practical move is not shopping for a new couch or panicking about rent—it is gathering every piece of medical paperwork related to the diagnosis and the reversal. Ask for copies of test results, scan reports, doctor notes, referrals, second opinions, and the formal explanation of the error. You need a clean paper trail because this is no longer just a medical story; it may also become an insurance, legal, or compensation issue.

Ask For A Clear Written Explanation

Do not settle for a vague, mumbly “mistakes happen.” Request a plain-language explanation of what went wrong. Was a lab result misread? Were records mixed up? Was a specialist supposed to confirm something but never did? You need to understand whether the error came from bad communication, bad testing, bad judgment, or something even more serious. Specifics matter now.

Consider Speaking To A Medical Malpractice Lawyer

This is one of those times when “talk to a lawyer” is not dramatic advice—it is practical advice. A misdiagnosis that caused major financial harm may be worth legal review, especially if you sold major assets, emptied accounts, or suffered documented emotional distress because of negligent care. A consultation can help you understand whether you have a case, even if you never decide to pursue one.

Write Down Everything That Happened

Memory gets slippery when trauma enters the chat. Sit down and create a timeline while the details are fresh: when you were diagnosed, what you were told, who said it, what actions you took, what you sold, what you withdrew, and what expenses followed. Include dates, names, amounts, and emotional impact. This record can help with lawyers, insurers, financial planners, and your future self.

Make A List Of What You Sold

Now comes the painful but useful inventory stage. Write down every major thing you sold, transferred, donated, or cashed out because of the diagnosis. Include the approximate value, the sale price, and whether the buyer was a stranger, company, friend, or family member. This is not about torturing yourself—it is about seeing the real scope of the damage and identifying what, if anything, can be reversed.

Some Things Might Be Recoverable

Not everything is gone forever. If you sold a car to a relative, a piece of jewelry to a friend, or furniture to someone local, it may be worth politely reaching out. Some people may be willing to sell it back, especially if they understand the situation. No, this will not work with every item, and yes, it may feel awkward, but awkward is cheaper than replacing everything at retail.

Review Any Home Sale Carefully

If you sold your house, condo, or land, pull every document from that transaction and have a real estate lawyer review it. Most completed sales cannot simply be undone because your circumstances changed, but there may be rare exceptions if fraud, coercion, or unusual contract terms were involved. At minimum, a lawyer can tell you where you stand and stop you from clinging to false hope.

Rebuild Your Housing Plan Fast

If you no longer own a place to live, housing becomes your top money priority. That may mean renting for now, staying with family briefly, or creating a six- to twelve-month stabilization plan before buying again. Do not pressure yourself to “get back where you were” immediately. The goal is not perfect symmetry with your old life; it is safe, stable footing.

Check What Happened To Your Savings

Maybe you spent cash reserves on bucket-list experiences, medical travel, debt payoff, or helping loved ones. Maybe you drained emergency savings because, honestly, what emergency could be bigger than dying? Now is the moment to check account balances without flinching. Knowing your starting point—even if it is ugly—is better than fearing a number you have not looked at yet.

Look At Retirement Withdrawals

If you pulled money from retirement accounts, there could be tax consequences, penalties, or opportunities to soften the damage depending on timing and account type. This is a good time to speak with a CPA or tax professional who can review what was withdrawn, when it happened, and whether any correction or planning move is still possible. The tax bill should not get to surprise you too.

Examine Insurance Decisions

Some people cancel life insurance, long-term savings products, disability coverage, or even health plans after a terminal diagnosis because the logic changes overnight. Now that the diagnosis has been reversed, review every policy you ended, reduced, or borrowed against. Reinstating coverage may not be simple, but understanding what lapsed and what can be restored is an important part of rebuilding.

Protect Your Credit While You Recover

A year like this can leave a financial mess behind the scenes. Bills may have gone unpaid, accounts may have been closed, and autopay setups may have been disrupted while you were emotionally underwater. Pull your credit reports, check for missed payments, collections, or identity mistakes, and make a plan to clean up the damage. Bad credit loves chaos, and you have had enough chaos.

Pause Big Emotional Spending

After surviving this kind of roller coaster, it is tempting to celebrate being alive by spending like a confetti cannon. Understandable? Absolutely. Wise? Not usually. Try not to swing from “I sold everything because I was dying” to “I deserve to buy everything because I’m not.” Your future self deserves some joy, yes, but they also deserve a working budget.

Build A Bare-Bones Restart Budget

Forget your old life for a moment. Build a fresh, stripped-down monthly budget based on the life you have now, not the one you had before the diagnosis. Start with housing, food, transportation, insurance, debt, and healthcare. Then add realistic categories for replacement items and emotional recovery. This is not punishment budgeting—it is your financial landing pad.

Replace What Matters Most First

You do not need to repurchase your entire life in a single dramatic weekend. Start with the essentials and the meaningful things that make daily life workable: a bed, a laptop, a car if needed, basic kitchen gear, work clothes, important documents, and maybe one or two comforts that make the place feel like home. Survival first, style later.

Lean On The People Who Love You

This is not the season for fake independence. If trusted family or friends can offer housing, furniture, childcare, transportation, or plain old moral support, let them. You do not get extra points for rebuilding alone with gritted teeth and a brave smile. Community exists for moments exactly like this, even when your pride wants to lock the door.

You May Need Therapy, Not Just Spreadsheets

Money is a huge part of this story, but it is not the whole story. A misdiagnosis like this can leave you with medical trauma, trust issues, grief over the life you dismantled, and even guilt over surviving a crisis that turned out not to be real. A therapist can help you process the emotional wreckage so your financial decisions are not being made by panic in a trench coat.

Be Careful With Family Conflict

Money stress plus emotional trauma can turn even loving families into courtroom-level drama clubs. Maybe you gave away inheritance early, loaned money to relatives, or sold things below value to people close to you. If tensions are rising, keep communication clear, documented, and calm. You do not need to turn every disagreement into a war, but you also do not need to be endlessly accommodating.

Revisit Any Estate Planning Changes

If you changed your will, named beneficiaries differently, assigned powers of attorney, or made end-of-life plans during the diagnosis period, review all of it now. Those choices may still reflect your wishes—but they may also belong to a version of you who thought the clock had almost run out. This is a good moment to update documents with a clearer head.

Don’t Rush To Return To “Normal”

There is a big temptation after something bizarre like this to perform normality as quickly as possible. Get the job, buy the furniture, smile at brunch, joke about second chances, move on. But your life is not a movie montage. Rebuilding will likely be uneven, emotional, and weirdly boring in places. That does not mean you are failing; it means you are living in reality.

Use Professionals Where They Count

This is a “pay for good advice” moment if you can manage it. A lawyer may help with liability, a CPA may help with tax fallout, a fee-only financial planner may help rebuild the numbers, and a therapist may help rebuild the person holding those numbers together. You do not need a giant team forever, but a little expert help now can prevent expensive mistakes later.

Make A Recovery Plan In Phases

Try dividing your comeback into phases: stabilize, assess, repair, rebuild. Stabilize housing and cash flow first. Assess the legal, tax, and asset situation next. Repair credit, insurance, and key paperwork after that. Then rebuild savings, routines, and long-term goals. When everything feels shattered, phases turn a catastrophe into a checklist, and that is often how healing begins.

Give Yourself Permission To Be Angry

You are allowed to be furious that a bad diagnosis blew up your finances and rearranged your life. That anger does not make you ungrateful to be alive; it makes you honest. The goal is not to suppress it under inspirational quotes and gratitude journals. The goal is to channel it into smart action, careful documentation, and better choices going forward.

This Is A Restart, Not A Ruin

The truth is, you may not be able to restore every dollar, every object, or every version of the life you had before. That part hurts. But a misdiagnosis does not have to become the final chapter of your financial story. With documentation, professional advice, a realistic plan, and a little self-compassion, you can build again—this time not around a countdown, but around the fact that you still have a future.

You May Also Like: