When Grief Turns Into Financial Panic

Losing a parent is one of life’s most disorienting experiences. When that loss is followed by phone calls or letters demanding money you never borrowed, grief can quickly turn into panic. The emotional timing alone can make it hard to think clearly or push back.

How Big a Problem Is Credit Card Debt in the U.S.?

Credit card debt is extremely common in the U.S. Americans collectively owe over $1.2 trillion on credit cards, according to Federal Reserve data. That scale explains why unpaid balances at death are far from rare. Many families encounter this suddenly, without warning or preparation.

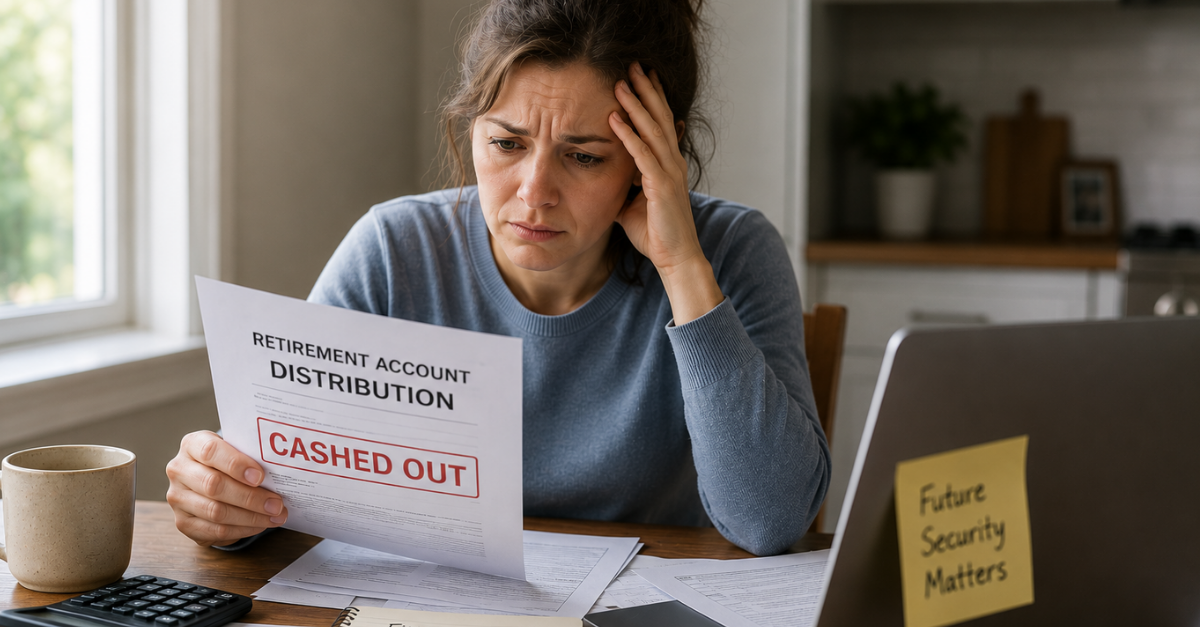

What Those Numbers Look Like for Real Families

The average U.S. credit card holder carries over $6,000 in credit card debt, and some studies estimate the average per household balance at more than $11,000. These amounts help explain why estates often can’t cover everything—and why creditors may push hard to collect.

Why Collectors Act Fast After a Death

Once a death is reported, credit card companies often move quickly to protect their interests. Accounts may be flagged and collection efforts can begin. Speed benefits the creditor—not the grieving family—and urgency does not always reflect actual legal responsibility.

What Debt Collectors Can and Cannot Do

Debt collectors may contact relatives to locate an estate or executor, but they cannot legally harass you or mislead you into thinking you personally owe a debt if you don’t. Federal consumer protection laws place limits on what collectors are allowed to say.

Where Debt Belongs After Someone Dies

When someone passes away, debts are typically paid from their estate, meaning the money and property they left behind. Debts do not automatically transfer to children or other family members, even if collectors imply otherwise.

The Role of an Estate Executor

An executor or personal representative is responsible for managing estate assets, reviewing creditor claims, paying valid debts in the correct order, and distributing what remains. If you are not the executor, you usually are not the proper party for payment discussions.

If the Estate Has No Money or Assets

If there are no assets—or not enough assets—in the estate, credit card companies often receive nothing. This is legally normal. Unsecured debts like credit cards are typically last in line and frequently go unpaid when estates are insolvent.

Exceptions: When You Might Be Liable

You may be responsible only in limited situations. These include being a joint account holder, a co-signer, or in some cases a surviving spouse in a community property state. Simply being a child or heir does not create legal liability.

Authorized Users vs. Responsible Parties

Being listed as an authorized user does not make you legally responsible for credit card debt. Joint account holders and co-signers are different. Collectors sometimes blur this distinction, which is why knowing how the account was set up matters.

Why Collectors Sometimes Contact Relatives

Collectors often contact family members to locate the executor or learn whether an estate exists. That outreach does not mean you owe the debt. In many cases, it is simply an attempt to find someone authorized to speak for the estate.

It’s Illegal to Misrepresent Your Liability

Federal law prohibits debt collectors from falsely stating that you are legally responsible for a debt you do not owe. Threatening lawsuits or financial consequences when none apply may violate consumer protection rules.

What a Collector Can Discuss With You

Collectors may ask about estate details or request executor information. What they should not do is pressure you to pay personally or suggest that moral responsibility equals legal obligation. You are allowed to set boundaries in these conversations.

Debt Doesn’t Disappear—It’s Just Handled Differently

Debt does not automatically vanish at death, but it does not pass down like an inheritance either. The estate absorbs it first. If the estate runs out of money, creditors typically have no further legal recourse.

How Probate Law Works (Simply)

During probate, estate funds pay expenses in a set order: administrative and funeral costs first, secured debts next, and unsecured debts like credit cards last. If nothing remains by the time credit cards are reached, those balances often go unpaid.

No Life Insurance Doesn’t Change Liability

The absence of life insurance does not make family members responsible for debt. Life insurance payouts generally bypass creditors unless the estate itself is named as beneficiary. Not having a policy may reduce assets—but it does not create new obligations.

Big Balances Don’t Automatically Mean Big Responsibility

Even very large credit card balances do not override the law. Without estate assets or a signed agreement tying you to the debt, the size of the balance alone does not make it yours.

Ask for Validation in Writing

You have the right to request written proof showing who owes the debt and why. This slows pressure tactics and forces collectors to document their claims. Until they do, you are not required to engage further.

How to Communicate Calmly and Safely

You can state that you are not responsible for the debt and ask for all communication in writing. You do not need to argue or explain. Calm, minimal responses protect you better than emotional back-and-forth.

When Legal Help Makes Sense

If collectors continue aggressive contact or make false claims, a brief consultation with a probate or consumer protection attorney can help. Even a single letter from an attorney often stops improper collection efforts.

The Bottom Line

You don’t inherit credit card debt simply because you lost your parents. In most cases, responsibility ends with the estate. Slow down, don’t pay out of fear, and make creditors prove every claim before you act.

You Might Also Like: