Money Matters

Nobody talks about the perks of growing older. Sure, there are challenges, but some things actually get better. Tax season becomes less painful when you know what advantages come your way.

IRS Senior Guidelines

The moment you turn 65, the IRS begins treating you differently—and more favorably. Dozens of provisions specifically benefit seniors, from enhanced deductions to special credits. These are written into sections like IRC 63(f) and detailed in Publication 554, “Tax Guide for Seniors”.

Geraldshields11, CC BY-SA 3.0, Wikimedia Commons

Geraldshields11, CC BY-SA 3.0, Wikimedia Commons

Tax Forms Overview

Form 1040-SR features a larger print and a simplified layout explicitly designed for taxpayers 65 plus. Unlike regular forms, it displays age-related benefits and includes helpful charts for Social Security calculations. Most adults complete their entire tax return using this form, along with Schedule A.

Age-Based Tax Benefits

Congress recognized that seniors face unique challenges. That's precisely why turning 65 triggers multiple tax advantages: additional standard deductions, elderly credits, penalty-free IRA withdrawals, and favorable capital gains treatment. The Tax Policy Center estimates these coordinated provisions save them an average of $1,200 annually.

Filing Status Impact

Strategic filing choices can dramatically affect your tax bill. Married couples might benefit from filing separately if one spouse has huge medical expenses, lowering the 7.5% AGI threshold for reductions. The choice between joint, separate, or head of household status for qualifying widows is different.

Improved Standard Deduction

Single filers receive $15,000 while married couples enjoy $30,000—amounts nearly doubled since 2017's Tax Cuts and Jobs Act. This guaranteed subtraction eliminates considerable income from federal taxation without requiring receipts. For couples in the 22% bracket, that represents automatic $6,600 tax savings.

Additional Senior Amount

Beyond regular abatement lies an often-overlooked benefit of $2,000 extra for singles and $1,600 per qualifying spouse for married people. This stacks automatically if you're 65 by December 31st, creating a combined $33,200 deduction for married seniors: no forms or calculations required.

Standard Vs Itemizing

With elevated amounts, roughly 90% of taxpayers now choose the standard deduction over itemizing. Yet, elders often have circumstances that make itemizing worthwhile due to medical expenses, mortgage interest, or charitable giving. The smart approach requires comparing your potential itemized total against guaranteed standard amounts.

Medical Expense Threshold

Also, medical expenses exceeding 7.5% of adjusted gross income become deductible, making this particularly valuable for folks facing escalating healthcare costs. For someone with $40,000 AGI, any expenses above $3,000 qualify for deductions. This encompasses insurance premiums, prescriptions, and doctor visits.

Prescription Drug Costs

Every prescription medication prescribed by licensed practitioners qualifies for medical expense reductions, including insulin, specialty drugs, and over-the-counter medicines with prescriptions. Even vitamins and supplements become deductible when prescribed for specific conditions. Keep pharmacy receipts year-round, as these costs often push adults over the 7.5% threshold.

Long-Term Care

Long-term care insurance premiums are also deductible based on age-adjusted limits: $470 for individuals aged 51–60, $1,760 for those aged 61–70, and $5,880 for those over 70 in 2025. Additionally, care facility costs qualify as medical expenses when medical care is the primary reason for residence.

Medicare Premium

Unlike Medicare Part A, which is premium-free for most seniors, Parts B, C, and D premiums require a deductible. Standard Part B costs $174.70 monthly, alongside supplemental Medigap policies, which add hundreds more. These premiums qualify as medical expenses, resulting in big deductions when combined.

Rix Pix Photography, Shutterstock

Rix Pix Photography, Shutterstock

Health Insurance Premiums

Self-employed elders hit the jackpot with above-the-line health insurance reductions. Unlike medical expense itemizations, which are subject to the 7.5% threshold, these premiums reduce adjusted gross income directly. This includes Medicare premiums, long-term care insurance, and even COBRA continuation coverage.

IRA Contribution Limits

The 2025 contribution ceiling is $7,000 annually, plus an additional $1,000 catch-up for those aged 50 and older, totaling a maximum of $8,000. Working seniors can contribute to traditional IRAs indefinitely, unlike the old rules that stopped contributions at 70½.

Photo By: Kaboompics.com, Pexels

Photo By: Kaboompics.com, Pexels

Traditional IRA

Income limits determine your rebate eligibility when a workplace retirement plan covers you. Single filers lose full deductibility between $79,000–$89,000 AGI in 2025. Similarly, married couples face phase-outs from $126,000 to $146,000. However, non-working spouses can contribute and subtract up to $8,000.

401k Contributions

Working older adults can defer $23,500 into 401 (k) plans for 2025, plus $7,500 catch-up contributions for those 50+. This totals up to $31,000 maximum annual deferrals. Such contributions slash current-year taxes while building retirement security.

Super Catch-Up

Apparently, individuals aged 60–63 enjoy enhanced catch-up contributions of $11,250 instead of the standard $7,500, which boosts total 401 (k) deferrals to $34,750 per year. This SECURE 2.0 provision recognizes peak earning years when retirement planning becomes urgent.

Mortgage Interest

Well, the $750,000 debt limit applies to mortgages originated after December 15, 2017. Earlier loans maintain the $1 million limit. Home equity loan interest becomes subtractable only when proceeds improve the secured property. Hence, no more subtracting interest on loans used for other purposes.

SALT Deduction

State and local tax deductions are capped at $10,000 annually through 2025, affecting the combined property taxes and sales taxes. High-tax states reach this limit quickly, making the deduction less valuable than it was at pre-2018 levels. However, the 2025 tax legislation proposes raising this cap to $40,000.

Property Tax

Real estate taxes on primary and secondary residences count toward the $10,000 SALT limitation, making careful planning essential in high-tax areas. Property tax assessments often increase during retirement as home values appreciate, creating larger deductions but potentially hitting SALT caps.

Energy Credits

So, home energy improvements qualify for 30% tax credits up to specific limits. This includes $1,200 for windows, doors, and insulation, as well as $2,000 for heat pumps and water heaters. However, the current tax legislation will eliminate most energy credits after December 31, 2025.

Home Office

That spare bedroom where you consult part-time becomes a legitimate business expense, potentially worth thousands in reductions. The IRS allows either a simplified deduction ($5 per square foot) or the typical expense method, calculating utilities, insurance, and maintenance percentages.

Business Equipment

Laptops, smartphones, printers, and office furniture become powerful tax abatements when used for consulting or business activities. Section 179 grants permission for the immediate expensing of up to $1.25 million in 2025, while smaller items under $2,500 qualify for the de minimis safe harbor rule.

Section 179 Expensing

Rather than depreciating business equipment over numerous years, Section 179 lets you cut the entire cost immediately, up to $1.25 million in 2025. This election works particularly well for older consultants who purchase expensive equipment, such as vehicles, computers, or machinery.

Bonus Depreciation

Equipment purchases this year qualify for a 40% bonus depreciation in addition to regular depreciation reductions, although this percentage decreases annually until its elimination after 2026. Unlike Section 179, bonus depreciation has no dollar limits and applies to both new and used qualifying property.

Professional Development

Continuing education maintains and improves skills required for your current business or profession, making courses, seminars, and certifications fully deductible. The IRS distinguishes between maintaining existing skills versus acquiring entirely new skills. Industry conferences, professional subscriptions, and even business-related books qualify, helping professionals stay current.

Centre for Ageing Better, Pexels

Centre for Ageing Better, Pexels

QCD Strategies

Qualified charitable distributions allow direct transfers from traditional IRAs to charities, satisfying required minimum distributions without developing taxable income. The $105,000 annual limit in 2025 provides tax planning opportunities for charitably inclined seniors facing large RMDs. QCDs work regardless of whether you take standard deductions.

Stepped-Up Basis

Inherited assets receive a "stepped-up basis" equal to fair market value at the decedent's death, essentially erasing lifetime capital gains for tax purposes. This provision can save heirs thousands on appreciated stocks, real estate, or other investments. Community property states provide even greater benefits.

Rental Property

Moreover, real estate investments provide multiple tax advantages, including depreciation deductions, maintenance expenses, and professional management fees. Residential rental property depreciates over 27.5 years, giving rise to annual rebates even when property values increase. The $25,000 annual loss allowance phases out for higher-income taxpayers.

Roth IRA Benefits

While contributions aren't deductible, Roth IRAs offer tax-free growth and withdrawals, plus no required minimum distributions during your lifetime. Old-aged people can convert traditional IRA funds to Roth accounts, paying current taxes to eliminate future tax obligations. Strategic conversions during lower-income years minimize conversion taxes.

SEP-IRA Deductions

Self-employed seniors are eligible to contribute up to 25% of self-employment income or $70,000 (whichever is less) to SEP-IRAs this year, drawing big tax deductions. Unlike traditional IRAs with modest limits, SEP contributions can reach thousands annually for profitable consulting businesses.

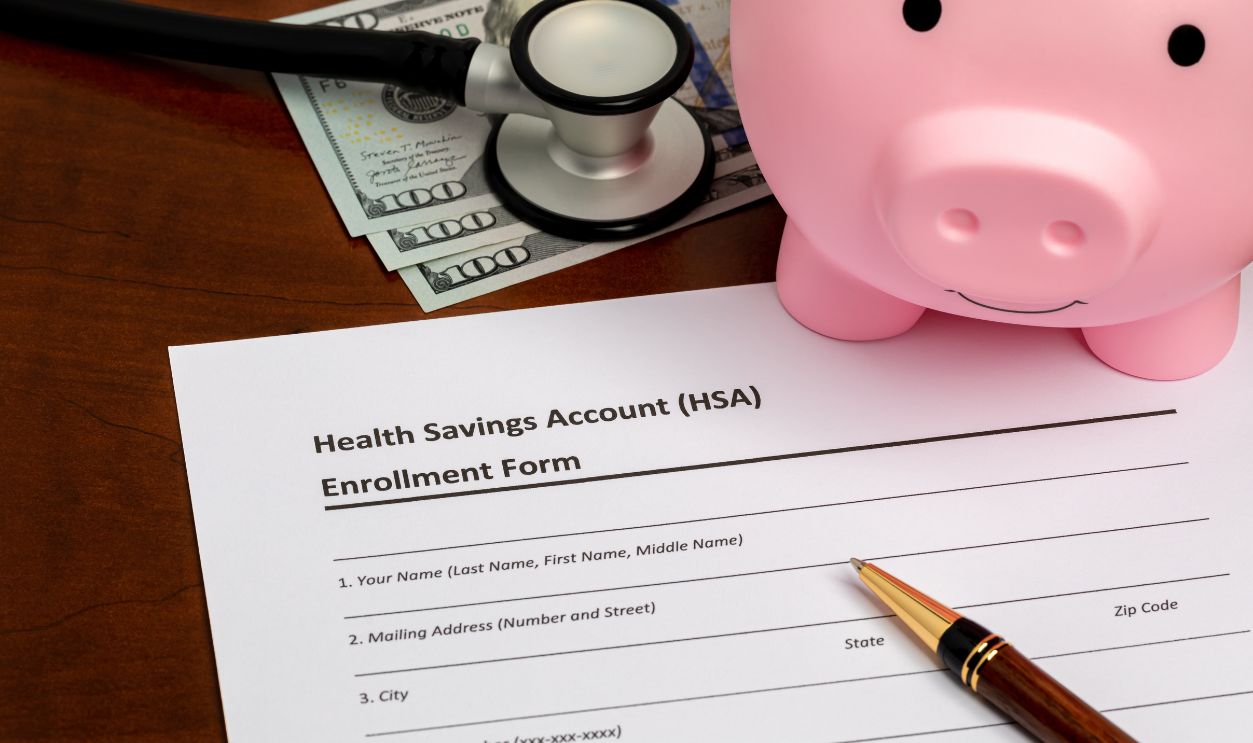

HSA Contributions

Health Savings Accounts serve triple tax advantages, which include tax-free growth and tax-free withdrawals for medical costs. Contribution limits are around $4,300 for individuals and $8,550 for families in 2025, requiring enrollment in high-deductible health plans. After age 65, HSAs turn into flexible retirement accounts.

HSA Catch-Up

Once you are 55, HSA contribution limits go up by $1,000 per year, allowing maximum deferrals of $5,300 for individuals or $9,550 for families when both spouses qualify. However, Medicare enrollment ends HSA eligibility, making the years between 55 and 65 particularly valuable.

Medical Transportation

Getting to medical appointments costs money, and those expenses add up to meaningful subtractions. The standard mileage rate for medical transportation is 21 cents per mile, covering gas, oil, and vehicle wear. Alternatively, deduct actual charges like parking fees, tolls, taxi fares, or even flights.

Home Modifications

Accessibility improvements for medical reasons qualify as deductible healthcare expenses, not just home improvements. Installing wheelchair ramps, walk-in tubs, stairlifts, or grab bars becomes tax-advantaged when medically necessary. Improvements that increase home value may require reducing deductions by the value added.

Photo by RDNE Stock project, Pexels

Photo by RDNE Stock project, Pexels

Business Travel

Consulting work often demands travel to client locations, conferences, or professional meetings. Airfare, hotels, ground transportation, and 50% of meals qualify when travel involves overnight stays away from your tax home. Combining business with pleasure requires careful allocation between deductible business days and non-deductible personal vacation time.

New Senior Deduction

The enacted $6,000 additional deduction for taxpayers 65 and above represents the most significant new senior tax benefit in decades. This benefit phases out for singles earning more than $75,000 and couples earning more than $150,000. It is available to itemizers from 2025 to 2028.

Charitable Above-Line

Revolutionary changes allow non-itemizing taxpayers to reduce charitable contributions above the line: $1,000 for singles and $2,000 for married couples filing jointly. This is tax-advantageous for the 90% of seniors who take standard deductions. Donations must go to qualifying 501(c)(3) organizations.

Car Loan Interest

Temporary legislation permits lowering interest on auto loans for vehicles with final assembly in the United States. The rebate caps at $10,000 and phases out for higher-income taxpayers. Available through 2028, this provision encourages domestic auto purchases while providing tax relief.

Overtime Deduction

The ability to subtract up to $12,500 ($25,000 for married couples) above the line from adjusted gross income is now applicable to working seniors who get overtime pay. The Fair Labor Standards Act's rules requiring overtime compensation fall under this category.

Elderly Tax Credit

The often-overlooked Credit for the Elderly provides $3,750 to $7,500 in tax credits for qualifying elders, though strict income limits apply. Single filers should possess an adjusted gross income below $17,500. Credits deliver dollar-for-dollar tax reductions, making this a lot more valuable.

RMD Planning

Required minimum distributions (RMDs) must begin at age 73 for traditional IRAs and most employer-sponsored retirement plans, regardless of whether you need the funds. The IRS requires these withdrawals to ensure taxes are eventually paid on pre-tax retirement savings.

Spreading Distributions

If you delay your initial RMD until April 1 of the year after you hit 73, you will need to take two RMDs in that year (one for the previous year and one for the current year), which could push you into a higher tax bracket.

Blind Taxpayer Benefits

Vision loss triggers additional tax advantages beyond standard senior benefits. Blind taxpayers receive extra standard deduction amounts such as $4,000 for single filers. This accounts for $2,000 for the regular senior amount plus $2,000 as a blindness addition.

Blind Taxpayer Benefits (Cont.)

Also, it is $3,200 per qualifying spouse for married couples. Note, however, that legal blindness necessitates either a field of vision of 20 degrees or less, as confirmed by licensed eye care specialists, or 20/200 vision in a superior eye with correction.

{kind=link}