I Deposited The Same Check Twice: Now What?

If you accidentally deposited the same check twice with mobile deposit, you are not the first. It usually looks like free money for a moment because your bank may give you a fast “availability” credit. The suspense part is that the banking system is built to catch duplicates, and it almost always does.

Gustavo Fring, Pexels, Modified

Gustavo Fring, Pexels, Modified

Why This Happens So Easily

Mobile deposit is designed for speed, not ceremony. It is easy to forget whether you already hit submit, especially if the app froze or you did it late at night. Some people also deposit by mobile and then later deposit the paper check in person, not realizing that counts as a second deposit.

The First Thing You See: A Temporary Credit

Many banks make some or all of the deposit available quickly under their funds availability policies. That does not mean the check has “cleared” in the way people mean it. It is more like a provisional credit that can be reversed if the check is returned or flagged.

“Cleared” Versus “Settled” Is The Whole Game

Checks move through multiple steps, including presentment and return timelines. Your app may show “accepted” or “processed,” but the paying bank still gets a chance to return it. That gap is where double deposits tend to get discovered.

How Banks Spot A Double Deposit

Banks use image analysis, duplicate detection, and review systems to catch repeat presentments of the same check image. Even if the photo is a little different, the check number, routing number, account number, and amount can match. Many duplicates are caught before final posting, but some are caught afterward.

What “Duplicate Presentment” Usually Triggers

If your bank sees the same check twice, it will likely reject the second deposit quickly. If it gets further, the check can be returned unpaid through the check return process. Either way, the second deposit typically does not stick.

The Most Common Outcome

The bank reverses the second deposit and pulls back the funds. If you already spent the money, your account can go negative. Then overdraft fees can become the next problem.

Why You Might Not Notice Until Later

Some banks post a deposit quickly and reverse it days later. The reversal can show up as a “returned item,” “adjustment,” or “chargeback” type entry in your transaction list. That delay is why this mistake can surprise people at the worst time.

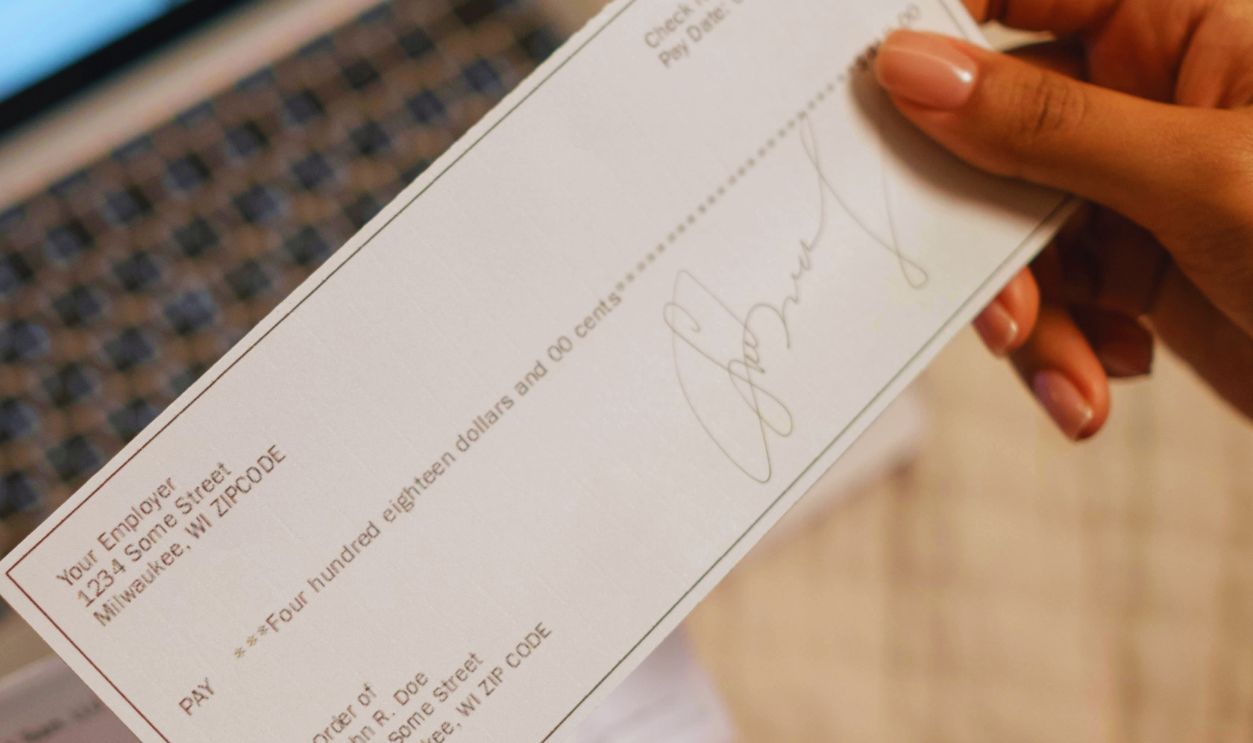

Yes, The Paper Check Still Matters

Most banks tell you to keep the original check for a period of time and then destroy it. That is partly so you can show it if there is a dispute, and partly to stop you from redepositing it. Keeping it in a drawer without marking it can set you up to repeat the accident.

Could The Paying Bank Pay Both?

Sometimes both deposits appear to go through at first, but that is not the same as final payment. The paying bank obviously is not supposed to pay the same check twice. If it happens, the duplicate is often reversed later through return or adjustment processes.

What If The Check Writer Notices First?

If the person or company that wrote the check sees two debits, they can contact their bank. They may also ask you directly, which can be awkward. The bank-to-bank process usually handles it, but communication can speed up the cleanup.

Your Bank Might Freeze Things Briefly

Some banks put a hold on your account or restrict mobile deposits if they suspect duplicate deposits. They are managing fraud risk, even if your situation was an honest mistake. The restriction is usually temporary, but it depends on the bank and the pattern they see.

Fees: The Part Nobody Wants To Click On

If the duplicate causes your balance to dip below zero, overdraft fees can follow. If the check is returned, returned deposited item fees may apply depending on your account terms. Many banks list these fees in their schedule of charges, so it is worth checking yours.

What If You Already Spent The Money?

If the bank reverses the duplicate credit and you do not have enough funds, you may need to deposit money to cover the shortfall. Acting quickly can reduce the chance of multiple overdrafts or declined payments. Waiting turns a simple mistake into an explensive chain reaction.

Could This Look Like Fraud?

Accidental double deposits happen, but intentional double presentment fraud is very much a thing. That is why the safest move is to report the mistake promptly. Being proactive can help your bank document it as an error instead of suspicious activity.

When To Contact Your Bank

Contact your bank as soon as you realize you deposited it twice. Ask what they see on their end and whether any holds or reversals are pending. Then ask what steps they want you to take, because procedures vary by bank.

What To Say On The Phone

Tell them the check amount, the date you submitted each deposit, and whether the paper check was also deposited elsewhere. Ask them to confirm which deposit will be reversed and when. Also ask if any fees are expected and whether they can be waived.

Do Not Try To “Fix” It By Depositing Again

It is tempting to keep poking at the problem until the app looks right. Additional deposits can create more confusion and more returned items. The cleanest fix is letting the bank reverse the duplicate and then settling any balance issues.

Should You Contact The Check Writer?

If the check writer is a person you know, it can be smart to tell them what happened. If it is a company, your bank may handle the correction without you needing to call anyone. If the writer sees two withdrawals, they may reach out anyway, so a heads-up can help.

How Long Does This Take?

Timing depends on when the duplicate is detected and the banks involved. Some duplicates are rejected the same day, while others are reversed after the check return cycle plays out. If you need a firm date, your bank is the best source because they can see the transaction status.

What “Holds” Mean In Plain English

A hold means the bank is delaying your access to funds while it verifies the deposit. Funds availability rules allow banks to delay availability in certain cases, including when they suspect the deposit might not be collectible. That is why you can see money in your account that you cannot fully use.

How To Protect Your Account While You Wait

Stop spending the extra money immediately. Move enough cash into the account to cover bills that might hit soon. If you are on the edge of overdraft, consider pausing nonessential payments until the reversal is done.

Preventing This Next Time Is Simple

Write “mobile deposited” and the date on the front of the check after your deposit is accepted. Store checks in one place until your bank’s recommended retention period is over. Then shred them so they cannot accidentally resurface.

Use The App’s Deposit History Like A Paper Trail

Most banking apps show a deposit history with images and timestamps. Check that screen before you try to deposit a check you found on your desk. That one habit prevents a lot of accidental duplicates.

If The Bank Thinks It Is A Pattern

If duplicate deposits happen repeatedly, a bank may disable your mobile deposit feature. They can also close accounts in serious cases, based on their account agreements. One mistake is usually fixable, but patterns raise red flags.

If You Get A Negative Balance Surprise

If your account goes negative because of the reversal, contact the bank quickly. Ask if they can waive fees if this was a first-time error. Also ask how long you have to bring the balance back to positive to avoid additional consequences.

The Bottom Line You Can Act On Today

Most of the time, the duplicate deposit gets reversed, and you are responsible for any money you spent that you were not entitled to keep. The smartest move is to contact your bank, stop spending the extra funds, and plan for a reversal. The real question is not whether the system will notice, but when.