When Their Debt Suddenly Becomes Your Problem

You thought the hardest part was over once the relationship ended. Then the calls start coming in. Creditors are reaching out about thousands of dollars in credit card debt that your ex racked up, and somehow your name is being dragged into it too. You didn’t make those purchases, so why are you being asked to pay?

The answer depends on a few key details, and while this situation can get messy, it doesn’t automatically mean you’re responsible for everything.

It Depends On Whose Name Is On The Account

The first and most important question is whether your name is actually on the credit card. If you’re a joint account holder, then yes, you’re usually legally responsible for the debt, even if your ex was the one who spent the money. Credit card companies don’t care who used the card, they care whose name is tied to the account. That’s what determines liability.

Authorized User Is Very Different From Joint Owner

If you were just an authorized user on the card, that’s a completely different situation. Authorized users can use the card, but they’re not legally responsible for paying the balance. In most cases, creditors can’t go after you for that debt if you were only an authorized user. That distinction matters a lot, and it’s worth confirming your exact status right away.

Community Property States Change The Rules

If you live in a community property state, things can get more complicated. In those states, debts taken on during the marriage may be considered shared, even if only one spouse opened the account. That means you could potentially be on the hook for debts your ex created while you were married. The rules vary depending on where you live, so location plays a big role here.

Adoramassey, Wikimedia Commons

Adoramassey, Wikimedia Commons

Timing Matters More Than You Think

When the debt was created is just as important as whose name is on it. Debt taken on during the marriage may be treated differently than debt created after separation or divorce. If your ex kept spending after you split, that can work in your favor, especially if you can show the relationship had already ended.

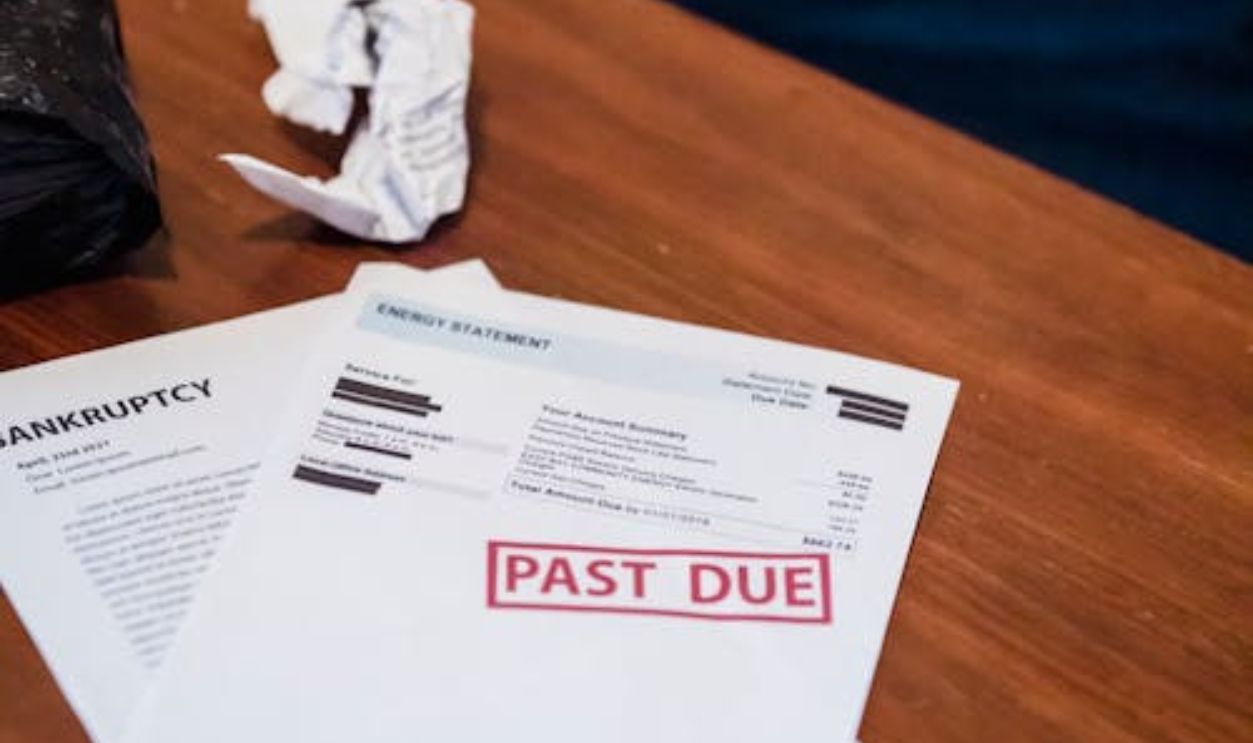

Divorce Agreements Don’t Always Protect You From Creditors

Even if your divorce agreement says your ex is responsible for certain debts, that doesn’t always stop creditors from coming after you. Creditors aren’t bound by your divorce terms because they weren’t part of that agreement. That means they can still try to collect from anyone legally tied to the account. The agreement may help you recover money later, but it doesn’t always stop collection efforts upfront.

Joint Debt Means Shared Responsibility

If the credit card was opened jointly, both parties are typically fully responsible for the balance. This is called joint and several liability, which means the creditor can pursue either one of you for the full amount. It doesn’t matter who made the charges or who benefited from them.

You Still Have The Right To Dispute Charges

If there are charges you truly didn’t authorize or that look suspicious, you may be able to dispute them. This is especially relevant if your ex used the card in ways that violated the agreement or involved fraud. It won’t apply in every case, but it’s worth reviewing the statements carefully.

Creditors May Try To Pressure You

Even if your legal responsibility is unclear, creditors may still contact you and try to collect. That doesn’t always mean you actually owe the debt. Sometimes it’s just part of their collection process. It’s important not to panic and to understand your rights before agreeing to anything.

Your Credit Score Could Be Affected

If your name is tied to the account, missed payments or high balances can impact your credit score. That’s true even if your ex was the one running up the debt. Keeping an eye on your credit report can help you catch problems early.

Removing Yourself From Accounts Can Help Going Forward

If you’re still listed on any shared accounts, it’s a good idea to remove yourself as soon as possible. That won’t erase existing debt, but it can prevent new charges from being added in your name.

Communication With Creditors Matters

If creditors are contacting you, don’t ignore them completely. You can ask for verification of the debt and clarify whether your name is actually on the account. Getting that information in writing can help you understand where you stand.

You May Be Able To Seek Reimbursement

If you end up paying off debt that your ex was supposed to handle, you may be able to pursue reimbursement. This is often done through the court system, especially if your divorce agreement assigned responsibility to your ex. It’s not always easy, but it’s an option.

Legal Advice Can Make A Big Difference

If the amounts involved are significant, it’s worth talking to a lawyer. They can review your situation, explain how local laws apply, and help you figure out your next move. A quick consultation can save you a lot of guesswork.

Debt Collectors Must Follow Rules

Even if you do owe the debt, collectors have to follow certain laws when contacting you. They can’t harass you, threaten you, or mislead you about what you owe. Knowing your rights can make these interactions a lot less intimidating.

You Can Request Debt Validation

If you’re unsure about the debt, you can ask the collector to provide validation. This means they have to prove the debt is legitimate and that you’re actually responsible for it. This step alone can sometimes stop improper collection attempts.

Keep Records Of Everything

Save all communications, statements, and agreements related to the debt. Having a clear record can help you if you need to dispute the debt or take legal action later. It also helps you stay organized during a stressful situation.

This Situation Is More Common Than People Think

A lot of people assume that once a relationship ends, financial ties automatically end too. Unfortunately, that’s not always the case. Shared accounts and debts can linger and cause issues long after the relationship is over.

Final Thoughts: You Might Not Be Fully Responsible

Whether you’re on the hook for your ex’s credit card debt depends on a few key factors, including whose name is on the account, when the debt was created, and where you live. While it can feel overwhelming at first, you’re not automatically responsible just because you were married. Once you understand your specific situation, you’ll be in a much better position to push back or take action if needed.

You May Also Like: