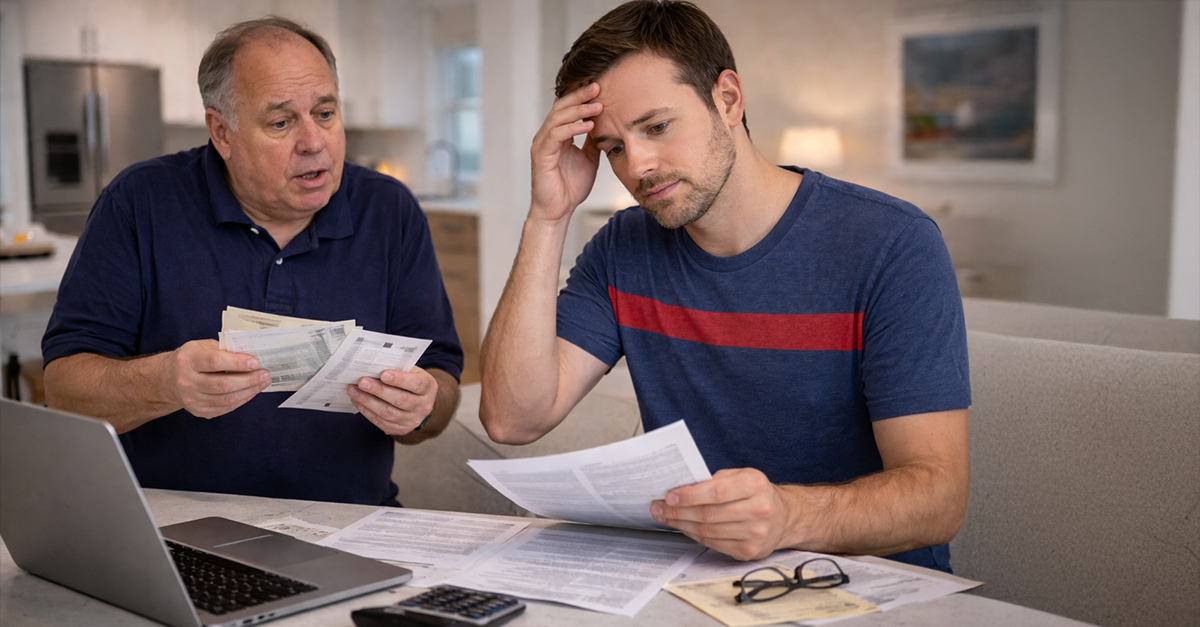

A Financial Request With History

You took a risk years ago buying Bitcoin, and your father-in-law openly mocked you for it at the time, dismissing it as the foolish financial blunder of a lazy, unreliable Millennial. Now, more than a decade later, your investment has paid off handsomely, and he is asking you for a substantial loan to save his struggling business. You never forgot his condescending attitude back then, and you’re experiencing a great deal of conflict.

Separate Emotions From The Decision

It’s completely natural to feel resentment or even a sense of irony in light of how he treated your decision in the past. But the smartest approach is always to separate emotion from financial decision-making. This situation isn’t about yelling “I told you so!,” or about settling scores. It’s about evaluating risk carefully and making a rational choice that protects your long-term financial stability.

Clarify What He Actually Wants

Before you make a decision, you need to understand exactly what he’s asking for in concrete terms. Is this a short-term loan meant to cover temporary cash flow issues, an open-ended request with no clear repayment plan, or something closer to an investment in his business? Each of these scenarios brings with it very different levels of risk and expectation.

Treat This Like A Business Transaction

Even though this involves family, you should approach it just the same way as you would any other financial decision involving a large sum of money. That means asking to see financial statements, understanding why the business is struggling, and figuring out whether there is a realistic path to recovery. If these details are vague or unavailable, that should raise immediate alarm bells.

Understand The Real Risk Of Loss

If you decide to lend him money, recognize there’s always a real possibility that you may never see this money again, especially with respect to a struggling business. Many companies fail even after they get additional funding. You should only consider lending an amount that you can afford to lose entirely without putting your own financial security, savings, or future plans at risk.

Decide If You Are Lending Or Giving

One of the most important decisions you need to make is to clarify if this is truly a loan or effectively a gift. If you expect repayment, then it must be structured and enforced accordingly. If you’re not comfortable taking legal or personal action to recover the money, it may be more honest to treat it as a gift or decline entirely.

Put Everything In Writing

If you decide to move forward with lending money, it’s an absolute must to formalize the agreement in writing. This written agreement should clearly outline repayment terms, timelines, any interest charged, and what happens if payments are missed. Verbal agreements, especially among family members, often lead to misunderstandings and can damage relationships when expectations aren’t met.

Consider Charging Interest

Charging interest may feel uncomfortable in a family situation, but it at least underlines the idea that this is a serious financial arrangement and not an informal favor. It also compensates you for the risk you’re taking. Even a modest interest rate can help clarify expectations and ensure that both parties treat the agreement with a suitable level of seriousness.

Think About Collateral

If the amount your father-in-law is asking for is significant, you may want to secure the loan with collateral such as business equipment, property, or other assets. This offers you some protection in case of nonpayment and demonstrates that the borrower is committed to honoring the agreement. Without collateral, your risk increases substantially.

Impact On Your Marriage

Your wife has a direct relationship with the person asking for help, which complicates this decision. It’s essential to have an open and honest discussion about what both of you are comfortable with before the two of you agree to anything. Financial decisions involving family can create tension, so alignment between you and your partner is critical.

Avoid Setting A Precedent

If you agree to provide financial assistance once, there is a possibility that it will not be the last time you are asked. Helping in one situation can create an expectation that you will step up to the plate again if future problems arise. Be clear from the very start about whether this is a one-time decision and set boundaries accordingly.

Watch For Emotional Pressure

Family requests for money are often accompanied by emotional undertones, whether intentional or not. You may hear arguments about loyalty, obligation, or shared history that make it harder to say no. Knowing these dynamics can help you stay focused on the financial realities rather than being influenced by pressure or guilt.

Consider Alternative Ways To Help

If you’re uncomfortable providing money, there are other meaningful ways to offer him support. You could help review his business plan, suggest some cost-cutting strategies, or connect him with some wise financial advisors or lenders. Offering guidance instead of cash gives you the room to help without exposing yourself to significant financial risk.

Be Honest If You Want To Say No

If you ultimately decide not to lend the money, make sure you communicate your decision clearly and respectfully. You don’t need to give him a detailed explanation of your finances, but you should also avoid being dismissive or confrontational. A calm and honest response will help you salvage the relationship even if he is disappointed.

If You Say Yes, Set Clear Limits

If you agree to help, make sure you define exactly how much you’re willing to provide and under what specific conditions. Make it clear that this is the full extent of your support and that additional requests will not be entertained. Setting firm limits upfront can prevent misunderstandings and protect you from ongoing financial obligations.

Protect Your Own Financial Future

Your Bitcoin investment was a triumph based on years of patience, risk-taking, and discipline. Before you use any of that wealth to help someone else, make sure that your own financial foundation is on a solid footing. This includes having sufficient savings, a solid retirement plan, and enough liquidity to handle unexpected expenses without stress.

Understand The Tax Implications

Large financial transfers between family members can have tax consequences depending on how they are structured. Loans, gifts, and investments are treated differently under tax laws. A consultation with a financial advisor or tax professional can help you avoid unexpected liabilities and ensure that everything is handled properly.

Document Every Interaction

Keep detailed records of all communications, agreements, and transactions related to a potential loan. This includes emails, written contracts, and payment history. Proper documentation can be extremely valuable if disputes arise later or if you need to take formal action to recover the funds.

Prepare For Any Outcome

Even with the best intentions, this situation could affect your relationship with your father-in-law or your spouse. Consider how you will handle different outcomes, including delayed repayment or a complete loss of funds. Thinking through these possibilities in advance can stop you from being caught off guard.

Bottom Line On Family And Money

You’re under no obligation to solve someone else’s financial problems, even if they are family. Whether you choose to help or decline, the most important thing is to make a decision that protects your financial well-being while upholding clear and respectful boundaries that support long-term relationships.

You May Also Like: