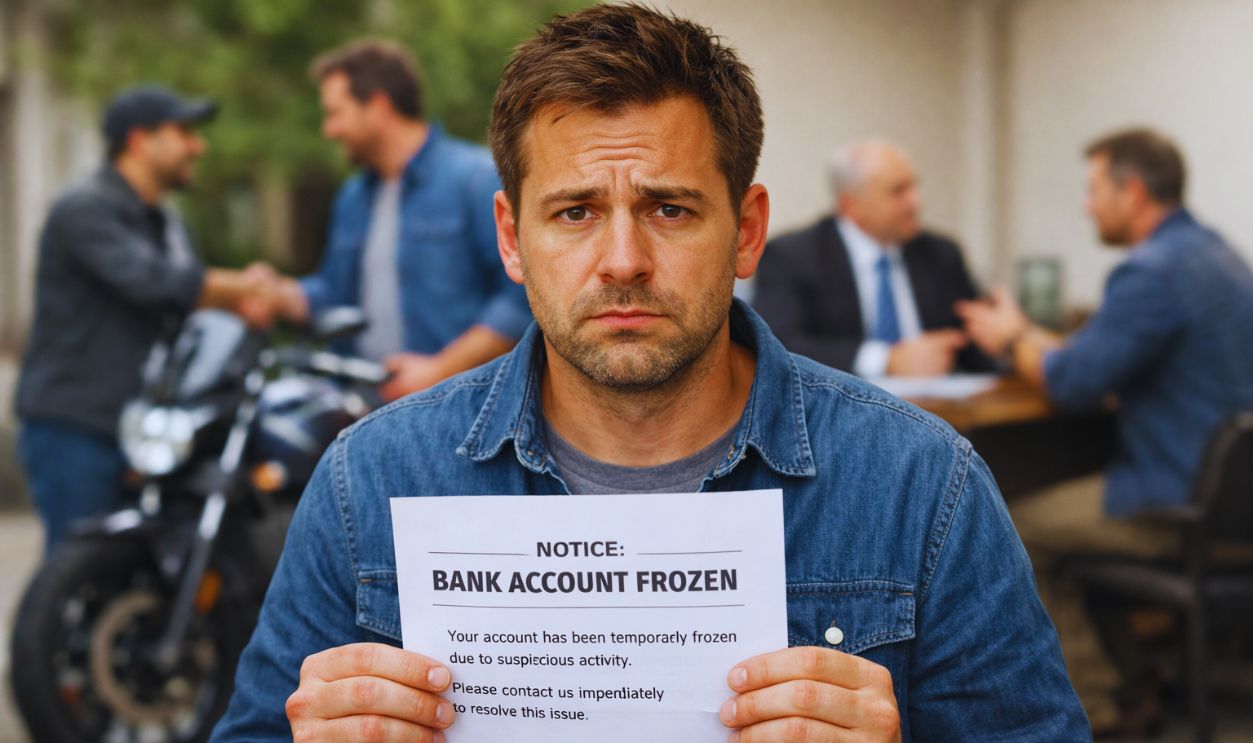

That $8,000 Deposit Can Raise Questions Fast

Selling a motorcycle for cash can seem simple until your bank suddenly restricts your account. If you deposited $8,000 and the bank froze access or put limits on the account, it can feel like your own money disappeared behind a wall of compliance rules.

But yes, a bank can place holds or restrictions while it reviews suspicious activity, even when the cash came from a legal sale. In fact, it's encouraged to.

Banks Do Not Wait For $10,000 To Pay Attention

A lot of people think banks only care once cash hits $10,000, but that is not how it works. Federal law requires banks to file a Currency Transaction Report for cash transactions over $10,000 in a single business day, but banks also watch smaller deposits for unusual patterns. An $8,000 cash deposit can still trigger a review if it looks out of character for your account.

The Rule People Get Wrong Most Often

The $10,000 number comes from the Bank Secrecy Act reporting system, and the Financial Crimes Enforcement Network says banks must file CTRs for cash transactions above that amount. But anything below $10,000 is not invisible. Banks also file Suspicious Activity Reports when they spot red flags, and those reports can involve much smaller amounts.

Sidney van den Boogaard, Shutterstock

Sidney van den Boogaard, Shutterstock

Suspicious Is Not The Same As Illegal

This is where many customers get caught off guard. A bank does not need proof that you did something wrong before it pauses access or reviews a deposit. If the transaction looks unusual compared with your normal banking history, the bank may restrict the account while it checks what happened.

Why A Motorcycle Sale Can Look Strange To A Bank System

If you usually get paid by direct deposit and then suddenly walk in with $8,000 in cash, that can stand out right away. Banks rely heavily on software and internal compliance teams to flag activity that does not match your usual pattern. A one-time private sale may be completely legal, but it can still look odd until you explain it.

Cash Draws More Attention Than A Check

Cash deposits usually get more scrutiny because cash is harder to trace than electronic payments. A check from the buyer, a bill of sale, and a title transfer create a cleaner paper trail. When the money comes in as stacks of bills, the bank may want more comfort that the source is legitimate.

A Hold Is Not Always The Same Thing As A Freeze

People often use those terms like they mean the same thing, but they can be different. A deposit hold usually delays access to some or all of the funds, while an account freeze or restriction can block withdrawals, transfers, debit card use, or online access more broadly. Either way, it becomes a real problem when bills are due.

Federal Hold Rules Usually Focus On Checks

The Expedited Funds Availability Act and Regulation CC mainly deal with how quickly banks must make check deposits available. Cash deposits made in person to a bank employee are generally supposed to be available no later than the next business day under the Consumer Financial Protection Bureau’s summary of the rules. But that does not stop a bank from restricting an account for suspected fraud or an anti-money-laundering review.

Yes, A Bank Can Restrict An Account During A Review

Your deposit may be available under funds availability rules, yet your account can still be locked down for a separate reason. Deposit availability law is not the same thing as fraud monitoring. If the bank thinks it needs to investigate suspicious activity, it may limit transactions while that review is underway.

The Bank May Not Tell You Much

This is one of the most frustrating parts of the process. Banks generally do not disclose whether they filed a Suspicious Activity Report, and federal law restricts them from telling customers about SAR filings. So you may hear vague language like “under review” instead of getting a clear answer.

Regulators Expect Banks To Watch For Red Flags

The Office of the Comptroller of the Currency says banks must maintain systems designed to identify and report suspicious activity. Those systems are part of anti-money-laundering and Bank Secrecy Act compliance programs. In plain English, banks are not just allowed to watch for unusual deposits. They are expected to.

Structuring Can Make A Bad Situation Worse

Some customers try to avoid attention by breaking cash into smaller deposits, but that can backfire fast. Federal law treats “structuring” as a crime when someone intentionally splits transactions to avoid reporting requirements. Even if your $8,000 came from a legitimate sale, making smaller deposits to stay under $10,000 can create a whole new problem.

One Straight Deposit Is Usually Better Than A Workaround

If you sold your motorcycle for cash, the safest move is usually to deposit the amount honestly and be ready to document it. Trying to outsmart the system often creates more suspicion than the original transaction. Compliance teams see workarounds as a major red flag.

Your Best Defense Is A Clean Paper Trail

If the bank questions the deposit, gather proof quickly. A signed bill of sale, title transfer, photos of the motorcycle listing, messages with the buyer, and any receipt showing the agreed sale price can all help. The clearer your records, the easier it is for the bank to connect the cash to a legitimate sale.

Bring The Sale Documents To The Branch

If your account is restricted, it may help to speak with a branch manager or fraud department and offer documents right away. Keep your explanation short, factual, and consistent. The goal is to show where the money came from, not to argue about banking law in the lobby.

Ask What Kind Of Restriction Was Placed

You should ask whether the bank put a deposit hold, a fraud restriction, or a full account freeze on the account. Those are different issues and may come with different timelines. Getting the right label matters because it tells you whether the problem is delayed funds or a broader investigation.

Request The Bank’s Funds Availability Policy

If the bank says the money is simply on hold, ask for its funds availability disclosure and the specific reason for the delay. Banks are required to provide disclosures about those policies. If the problem goes beyond a standard hold, that may become clearer from the bank’s explanation.

Keep Notes On Every Conversation

Write down the date, time, branch, phone number, and name or employee ID of anyone you speak with. Note what they said about the restriction and what documents they asked for. If the situation drags on, a solid timeline can help a lot.

Do Not Expect It To Clear Overnight

Some reviews are resolved quickly, but others can last for days or longer depending on the bank and the facts. There is no universal federal deadline for every fraud review or suspicious activity investigation. That uncertainty is exactly what makes a sudden restriction so disruptive.

If Bills Are Due, Escalate Early And Stay Calm

Tell the bank if the restriction is affecting urgent expenses like mortgage payments, payroll, or medical bills. Ask whether any part of the balance can be released while the review continues. A calm, documented escalation usually works better than anger, especially with fraud teams.

You Can File A Complaint If The Bank Will Not Respond

If you believe the bank is mishandling the situation or refusing to explain a standard hold, you can submit a complaint to the Consumer Financial Protection Bureau. The CFPB forwards complaints to financial companies and tracks responses. That does not guarantee a fast fix, but it can create pressure and a paper trail.

State Or Federal Regulators May Also Matter

The right regulator depends on the bank’s charter and whether it is supervised by a state or the federal government. The FDIC, OCC, Federal Reserve, or a state banking department may oversee the institution. If you are not sure who regulates your bank, its website or branch staff should be able to tell you.

There Is A Safer Way To Handle Big Private Sale Proceeds

Before accepting cash for a vehicle or motorcycle, think about whether a cashier’s check at the buyer’s bank or another verified payment method during banking hours would leave a better paper trail. Cash is legal, but it creates more questions later. A cleaner transaction today can save you a lot of trouble afterward.

Meet The Buyer At A Bank If You Can

This is one of the simplest ways to avoid problems in the future. If the buyer brings cash, meeting at your bank lets you deposit it right away and get a receipt on the spot. It also gives you a chance to explain the source of the funds before the deposit gets flagged for review.

What Not To Say Or Do

Do not joke about avoiding reporting rules, and do not mention splitting deposits to stay under limits. Do not create backdated paperwork or change your story later. Banks are trained to notice inconsistent explanations, and credibility matters when your account is under review.

The Bottom Line On Whether A Bank Can Hold Your Money

Yes, banks can restrict access to your account or delay use of funds when they suspect fraud, need to verify a cash transaction, or detect activity that triggers anti-money-laundering review. That does not mean the bank gets to keep your money forever or that you did anything wrong by selling your motorcycle. It means you should be ready to prove where the cash came from, ask precise questions, and escalate step by step if the restriction does not clear.

What To Do Right Now If This Happened To You

Gather your bill of sale, title records, listing screenshots, buyer messages, and deposit receipt. Contact the bank, ask what kind of restriction was placed, and request the fastest way to submit source-of-funds documents. If the response is vague or unreasonable, document everything and consider filing a CFPB complaint while you keep pressing for a clear answer.