A Penny For Your Thoughts

Most people have a jar of spare change somewhere. You took things a little further. Over the years, loose coins turned into rolls, the rolls turned into boxes, and now there's nearly $5,000 sitting in your basement. It sounds harmless enough—until you start wondering what happens when you finally try to turn all that metal into money. Could a giant pile of change raise questions you weren't expecting?

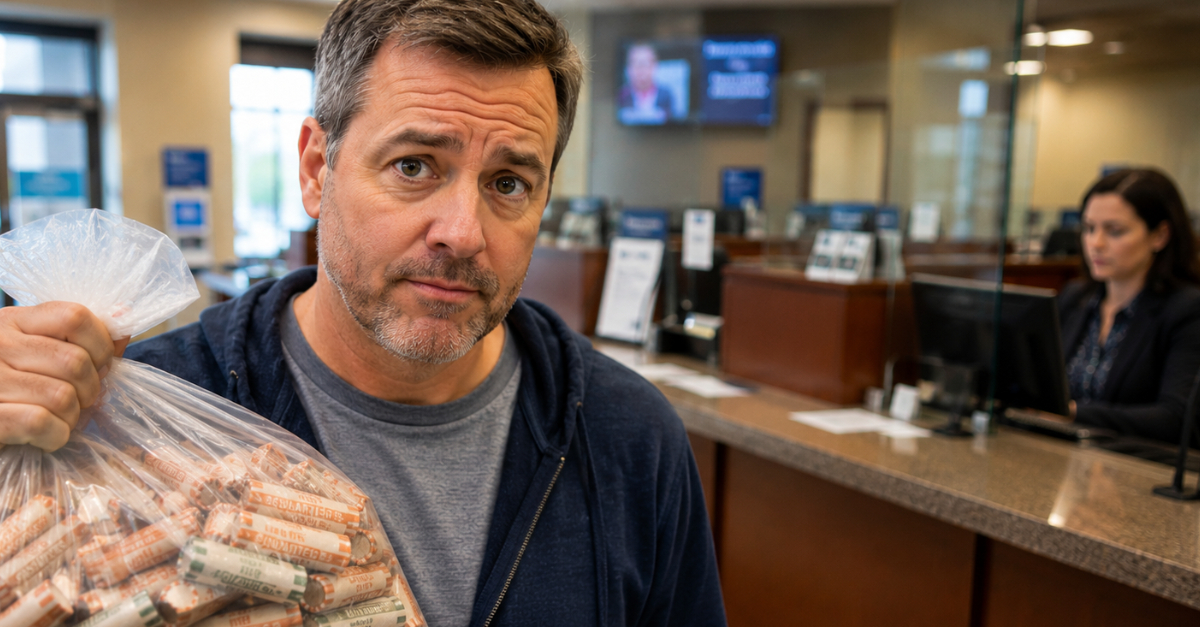

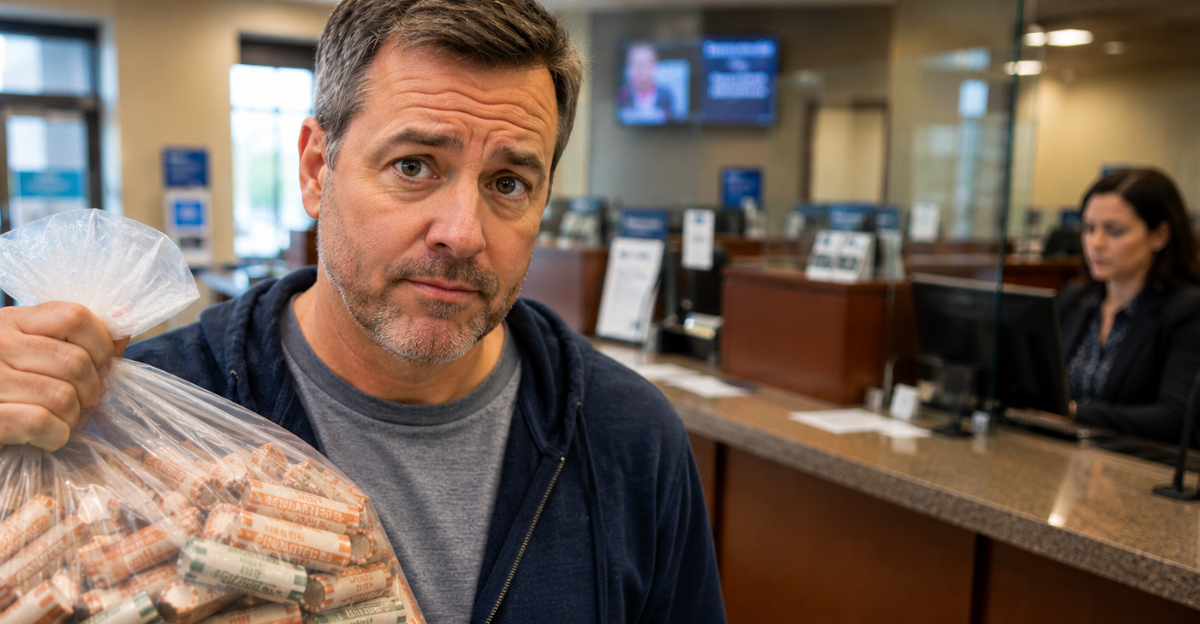

That's A Lot Of Change

Five thousand dollars in coins isn't the kind of thing most people walk into a bank with. In fact, it's enough that friends, family, and random people on the internet might all give you different answers about what happens next. Some say nobody will care. Others insist it could trigger reports, questions, or even an IRS headache. So what's fact, what's fiction, and what should you actually expect when you cash it in?

What Would You Say If Someone Asked?

For many people, the anxiety isn't about the coins themselves. It's about not having a perfect paper trail. After all, if you've been saving spare change for 10, 20, or even 30 years, how exactly would you prove where every penny came from? That's where a lot of the confusion starts—and where a lot of the myths begin.

$5,000 Might Get A Second Look

A $5,000 coin deposit is unusual enough that a bank employee may ask a few questions, especially if you're bringing in boxes of rolled coins. But that's very different from being accused of wrongdoing. Banks process large deposits every day, and a customer cashing in years of accumulated change is generally not something that automatically suggests a tax problem or criminal activity.

Banks Are Looking For Patterns

Contrary to popular belief, banks don't focus solely on transactions over a certain dollar amount. Banks may use monitoring systems to look for patterns, including activity that appears inconsistent with a customer's normal account history. That's one reason a smaller but unusual deposit can sometimes attract more attention than a larger deposit that fits an established pattern.

Unusual Activity Can Trigger Questions

Banks don't just look at dollar amounts. They also look at whether a transaction fits your normal banking pattern. If you've never deposited large amounts of cash and suddenly show up with thousands of dollars in rolled coins, the bank may ask where the money came from. That's not necessarily a sign you're in trouble—it's simply part of the monitoring banks are required to do for unusual transactions.

Banks May Be More Curious Than The IRS

If anyone asks questions, it's usually the bank rather than the IRS. A teller might simply ask where the coins came from because transporting and processing large amounts of coinage is unusual. A bank's concern is usually understanding the source of the funds rather than collecting taxes. If your explanation makes sense and matches the circumstances, the conversation often ends there.

Banks File Certain Reports

One reason people worry about large deposits is because they've heard banks report certain transactions to the government. That's true. Banks are required to file Currency Transaction Reports for cash transactions exceeding $10,000 in a single business day. However, a $5,000 coin deposit falls below that threshold.

Coins Count As Cash

For reporting purposes, coins are considered cash just like paper currency. If someone deposited more than $10,000 in coins, the same reporting rules would generally apply. Even then, a report is simply a record of the transaction—not an accusation of wrongdoing.

Change Happens

First, simply depositing money is not a taxable event. The IRS taxes income, not bank deposits themselves. If the coins came from years of saving spare change from purchases, piggy banks, tip jars, couch cushions, and forgotten pockets, you're generally just converting one form of money into another. The act of turning coins into cash doesn't create new income.

The IRS Doesn't Tax Your Own Money Twice

One of the biggest misconceptions is that any large deposit automatically triggers taxes. That's not how it works. If the money originally came from wages, gifts, refunds, or other legitimate sources that were already taxed—or weren't taxable to begin with—depositing it later doesn't suddenly make it taxable. You're simply putting existing money back into the banking system.

Coin Deposits Are Common

Businesses routinely deposit large amounts of coins. Laundromats, vending machine operators, arcades, car washes, convenience stores, and restaurants can all generate significant coin deposits. A consumer showing up with years of accumulated change isn't nearly as rare as many people think.

The Real Concern Is Unreported Income

The IRS generally isn't interested in the fact that you deposited coins. What they care about is whether the money represents income that was never reported. If the coins came from a side business, cash tips, or other taxable income that was never declared, that could create a different issue entirely.

Documentation Helps

If you've been saving coins for many years, there may not be much documentation to produce. That's normal. However, if the money came from a specific source—such as a coin collection you sold, a garage sale, or a business activity—keeping records is always a good idea.

Most People Overestimate IRS Scrutiny

Many Americans assume the IRS reviews every deposit made into every bank account. In reality, the agency generally doesn't have the resources or interest to investigate ordinary banking activity without some other reason to do so. A $5,000 deposit by itself is usually not enough to trigger attention from the IRS.

Don't Try To Break Up Deposits

Some people hear about the $10,000 reporting threshold and think they should split deposits into smaller amounts. That's usually a bad idea. Intentionally breaking up deposits to avoid reporting requirements—known as structuring—can create more problems than simply making a legitimate deposit in the first place.

Coin Counting Machines Have Limits

Before heading to the bank, check its policies. Many banks no longer accept large quantities of rolled coins from non-customers, and some require appointments for substantial coin deposits. Others may have coin-counting machines that make the process much easier.

Some Banks Charge Fees

Not every bank handles large coin deposits for free. Certain institutions charge non-customers a fee or limit the amount they'll accept at one time. It's worth calling ahead before loading several hundred pounds of coins into your car.

$5,000 In Pennies Is Heavy

If your stash consists mostly of pennies, you're dealing with a surprisingly large amount of weight. A modern penny weighs about 2.5 grams, meaning thousands of dollars in coins can quickly become a transportation challenge. The logistics may be more difficult than the tax questions.

Coinstar Is Another Option

Coin-counting kiosks can convert coins into cash or gift cards. However, cash redemption options often involve fees. For very large amounts, a bank relationship is frequently the more economical route.

The Source Matters More Than The Form

From the IRS perspective, the key issue isn't whether the money is coins, bills, checks, or electronic transfers. The important question is where the money originally came from and whether any taxable income associated with it was properly reported.

Gifts Aren't Usually A Problem

If the coins were accumulated from gifts, birthday money, holiday cash, or similar sources over many years, depositing them generally doesn't create a tax issue. Gifts are generally not taxable to the recipient, though very large gifts may create filing obligations for the person giving the gift.

Old Savings Can Add Up Fast

Many people underestimate how much loose change they accumulate over time. Saving just a few dollars in coins each week can eventually grow into thousands of dollars over a decade or two. What feels like pocket change today can become a surprisingly large pile later.

Banks See Stranger Things

Bank employees routinely encounter customers depositing inheritances, settlement proceeds, home-sale funds, insurance checks, and years' worth of saved cash. A bucket of rolled coins may be memorable, but it's hardly the strangest transaction they'll see that week.

What If The IRS Did Ask?

In the unlikely event that questions ever arose, you'd simply explain the source of the funds. If the coins truly came from years of accumulated spare change, that's a perfectly legitimate explanation. The more unusual the deposit looks compared to your normal banking activity, the more important it becomes to provide a straightforward and consistent explanation.

Lane V. Erickson, Shutterstock

Lane V. Erickson, Shutterstock

The Bigger Challenge May Be Counting It

Before worrying about the IRS, you may want to verify how much money is actually there. Many people estimate their coin hoards incorrectly and discover the total is higher—or lower—than expected once everything is counted. The math may be the biggest surprise.

So Can The IRS Question It?

Technically, the IRS can ask questions about almost any financial transaction. But a one-time deposit of roughly $5,000 in rolled change from years of legitimate savings is unlikely to raise major concerns on its own. If the money came from lawful sources and any taxable income was properly reported when earned, cashing in the coins is usually more of a banking task than a tax problem.

You Might Also Like:

My insurance premium suddenly increased and now I can't afford it. Is there anything I can do?