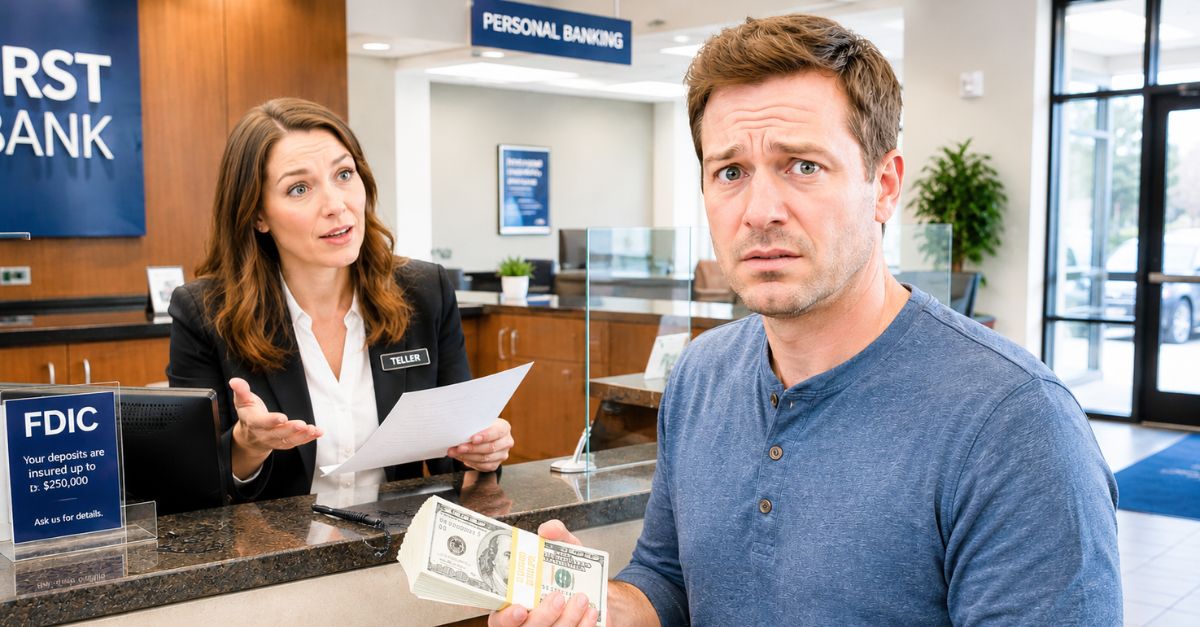

I Got Close, But Taxes Still Count

Almost hitting a five-figure parlay feels brutal enough before anyone brings up taxes. Still, your dad is partly right and partly exaggerating. A big sports-betting win can face federal withholding, state taxes, and extra paperwork. But is it as bad as he's making it sound? Let's just say: You still would have been very happy you won.

The Win Is Taxable Income

The IRS treats gambling winnings as taxable income. That includes winnings from sports betting, lotteries, horse racing, casinos, raffles, and similar wagers. You must report gambling winnings even if the sportsbook never sends you a Form W-2G. So the first hard truth is simple. A parlay payout is not tax-free money.

Withholding Is Not The Same As Final Tax

People often hear that gambling winnings get taxed at 24% and assume that is the whole bill. The IRS instructions for Form W-2G say regular federal gambling withholding is 24% for certain qualifying sports-wagering winnings. That withholding is like a prepayment toward your tax bill. Your final tax depends on your total income, deductions, filing status, and state rules.

The Threshold Matters

For sports wagering, federal withholding is not triggered by every nice win. The key federal rule generally looks at whether winnings minus the wager exceed $5,000 and whether the payout is at least 300 times the amount wagered. That means a $50 bet paying $10,000 may be treated differently from a $500 bet paying $10,000. The size of the win matters, but the odds multiple matters too.

A Five-Figure Payout Could Trigger Paperwork

A five-figure parlay can easily cross reporting and withholding thresholds if the wager was small enough. In that case, the sportsbook may issue a Form W-2G and withhold federal tax. The form reports the gambling winnings and any tax already withheld. That does not mean the IRS only cares when a form exists.

Smaller Wins Still Count

A common mistake is thinking unreported gambling income does not exist. The IRS says all gambling winnings must be reported, including winnings not reported on Form W-2G. This matters because sportsbooks may not issue a form for every taxable win. The taxpayer still has the reporting obligation.

State Taxes Can Change The Answer

Federal tax is only one layer. Many states tax gambling winnings as income, while some states have no income tax. Local taxes may also matter in some places. That is why two people with the same parlay payout can keep different amounts after tax.

The Sportsbook Usually Is Not Taking Most Of It

When people say “they take most of it,” they often mix up the sportsbook, the IRS, and the state. The sportsbook may withhold federal tax if the win meets the rule, but it is not keeping that money for itself. It sends withheld tax to the government in your name. The bigger built-in sportsbook cost is usually the odds and house edge before the bet is ever settled.

Parlays Are Built To Tempt You

Parlays are popular because they turn small stakes into eye-catching possible payouts. A Washington Post analysis found that parlays generate much higher revenue for sportsbooks per dollar wagered than straight bets in many states that publish parlay data. The reason is mathematical. Each added leg makes the ticket harder to hit.

Almost Winning Is Still Losing

A parlay that misses by one leg can feel like proof that you were close. Financially, it is the same as any other losing ticket. The near miss does not create a tax deduction unless you have gambling winnings and qualify to deduct losses. It also does not mean the next parlay is more likely to hit.

Fees Are Usually The Smaller Issue

For most mainstream online sportsbooks, deposit and withdrawal fees are usually not the main cost of betting. FanDuel says it does not charge deposit or withdrawal fees, though banks or payment providers may charge their own fees in some cases. The larger financial drag is usually losing bets, unfavorable odds, and taxes on actual wins. That is where bettors get surprised.

Losses Do Not Automatically Cancel Wins

This is where gambling taxes get frustrating. The IRS says gambling losses are deductible only if you itemize deductions and keep proper records. Loss deductions are also limited to gambling income. You cannot use gambling losses to reduce wages, business income, or other non-gambling income.

Lane V. Erickson, Shutterstock

Lane V. Erickson, Shutterstock

The Standard Deduction Can Hurt Bettors

Many taxpayers take the standard deduction instead of itemizing. For 2026, the IRS lists the standard deduction at $16,100 for single filers, $32,200 for married couples filing jointly, and $24,150 for heads of household. If you take the standard deduction, you generally do not separately deduct gambling losses. That can make the tax result feel worse than the actual betting result.

Records Are Not Optional

The IRS says taxpayers need an accurate diary or similar record to deduct gambling losses. Records should show winnings, losses, receipts, tickets, statements, or other proof. Sportsbook account histories can help, but bettors should not assume the app will preserve everything forever. Downloading statements during the year is a safer habit.

The 2026 Rule Adds A New Twist

Tax reporting around gambling became even more sensitive in 2026 because of the new federal limit on gambling-loss deductions. Reporting from Kiplinger and tax firms says the One Big Beautiful Bill Act limits deductible gambling losses to 90% beginning with the 2026 tax year. That can create taxable “phantom income” for heavy bettors. Even break-even gamblers may have taxable income under that rule if they itemize.

A Simple Example Shows The Problem

Imagine someone wins $10,000 in gambling income and loses $10,000 in documented gambling losses in 2026. Under the new 90% limit, only $9,000 of losses may be deductible if the bettor itemizes and otherwise qualifies. That leaves $1,000 of taxable income even though the bettor broke even in cash. That is why tracking and planning matter.

A One-Time Winner Has A Different Problem

A casual bettor who hits one big parlay may not have enough itemized deductions to make loss deductions useful. If that person has a $10,000 win and $2,000 in losses, the full win is still reportable. The losses may not help if the bettor takes the standard deduction. That is the part many casual bettors miss.

Inside Creative House, Shutterstock

Inside Creative House, Shutterstock

Withheld Tax Could Be Too Much Or Too Little

The 24% federal withholding rate is not a guarantee that your tax is settled. If your total income puts you in a higher marginal bracket, you may owe more at filing time. If too much was withheld, you may get credit for it on your return. Withholding is a starting point, not the final answer.

Big Wins Can Affect Other Tax Details

A large gambling win can increase adjusted gross income. Higher income can affect credits, deductions, marketplace health subsidies, student loan calculations, and other tax-sensitive items. That does not happen to every bettor. But it is a reason not to spend the whole payout before filing.

Promotional Bets Need Careful Reading

Sportsbooks often promote bonus bets, odds boosts, and parlay insurance. The tax treatment can depend on what is actually paid out and how the sportsbook records the transaction. The practical advice is to save the promotion terms and account statement. If the numbers are large, ask a tax professional before assuming the app’s balance tells the whole story.

Do Not Confuse Handle With Profit

Sportsbooks and regulators often discuss handle, which means the total amount wagered. A bettor can have a huge handle without making a huge profit. Tax reporting focuses on winnings, losses, and documentation. Your annual betting volume can look much larger than the money you actually kept.

The Best Move Is Boring

The smartest betting tax move is to keep a running log. Record the date, sportsbook, amount wagered, amount won or lost, and any tax form received. Save screenshots or statements after major wins. That is not exciting, but it is much easier than rebuilding a year of bets during tax season.

Do Not Chase The Tax Bill

A near miss can make another parlay feel tempting. That is exactly when bettors should slow down. Tax rules do not make a bad bet good, and chasing losses can turn a painful almost-win into a real financial problem. Set a betting budget before the game starts.

Your Dad Was Half Right

Your dad was right that taxes can take a meaningful bite out of a five-figure parlay payout. He was probably wrong if he meant most of the money would automatically vanish to taxes and fees. Federal withholding may be 24% in qualifying cases, state taxes may add more, and losses may be hard to deduct. But the exact result depends on the wager size, odds, state, income, and filing choices.

The Real Answer Is More Annoying

The tax system does not treat every sports bettor the same. A small-stakes bettor who hits a long-shot parlay can trigger withholding and reporting. A higher-stakes bettor with the same payout may not trigger the same automatic withholding rule. Both still have taxable income if they win.

What To Do After A Big Win

Set aside money for taxes before spending the payout. Download your sportsbook statement and save the W-2G if one arrives. Keep a separate record of losses, but do not assume they will fully offset the win. For a five-figure payout, a short appointment with a qualified tax professional can be worth the fee.

The Bottom Line

A five-figure parlay would not be swallowed whole by taxes and fees in most ordinary cases. The bigger truth is that gambling wins are taxable, losses are harder to use than people expect, and parlays are designed to favor sportsbooks over time. If you hit one, celebrate carefully. If you almost hit one, treat the near miss as a warning rather than a plan.