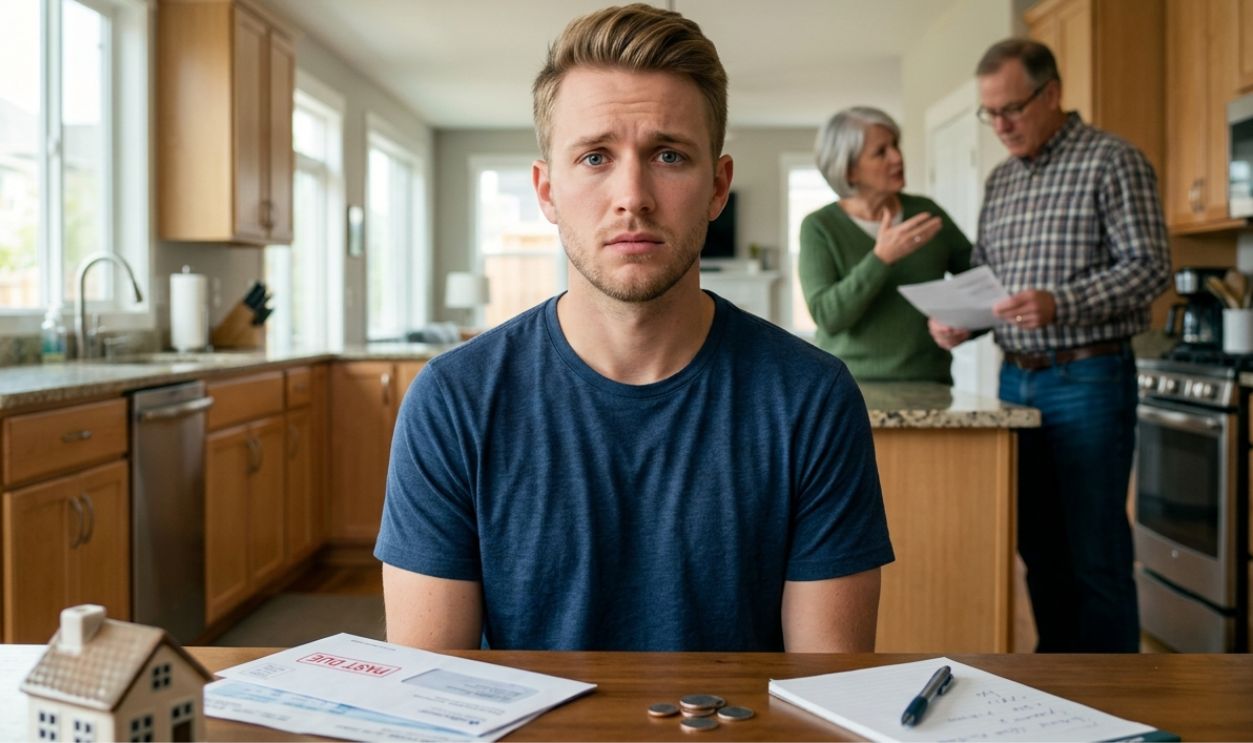

A Family Favor That Can Get Expensive Fast

When parents ask an adult child to put utilities in their name, it can sound harmless. It feels like paperwork, not a serious financial move. And, after all, you do kind of owe them, don't you? But once your name is on the account, the bill and any fallout tied to it can become your problem too—and the fallout can be a lot more serious than you might think.

Why This Matters More Than It Looks

Utility accounts do not feel as big as a mortgage or car loan. Still, unpaid balances can go to collections, and collection accounts can show up on your credit reports. The Consumer Financial Protection Bureau, or CFPB, says debt collectors may report collection accounts to credit reporting companies, which is why a small favor can turn into a real risk.

What It Really Means To Put Utilities In Your Name

If the account is in your name, the utility company will usually treat you as the person responsible for paying it. That is true even if you do not live in the home. In plain terms, you may be taking legal and financial responsibility for someone else’s monthly bills.

The Biggest Risk Is Not Just One Missed Bill

The real problem is often not a single late payment. It is what happens next if the balance keeps growing. A past-due account can become a collection account, and that can make it harder to rent an apartment, borrow money, or get a good rate later.

Collections Can Cause A Mess Fast

The CFPB says debt collection is one of the most common consumer complaints it handles. Once an unpaid bill is sent to a collector, you may be dealing with calls, letters, disputes, and credit reporting problems. That is a steep price to pay for trying to help family.

Your Credit May Be More Exposed Than You Think

People sometimes assume utility bills never affect credit unless a credit card is involved. That is not quite true. The three nationwide credit bureaus note that collection accounts can appear on credit reports, even though regular utility payments usually are not reported the same way as loans.

There Is Also The Risk Of Utility Identity Theft

The Federal Trade Commission warns that identity thieves can open utility accounts in someone else’s name. That matters here because even a family-arranged account can create similar headaches if charges pile up and the person named on the account later disputes responsibility. Sorting out who used the service and who owes the debt can turn into a long, stressful process.

If You Do Not Live There, You Lose Control

You cannot control thermostat settings, water use, or whether bills are paid on time in a house where you do not live. You also cannot control whether service gets shut off for nonpayment. That gap between responsibility and control is one of the clearest reasons to be careful.

Consumer Protections Help, But They Do Not Remove The Risk

The Fair Debt Collection Practices Act protects consumers from some abusive debt collection practices. The FTC says debt collectors cannot use harassment, lies, or unfair tactics when trying to collect a debt. Those protections matter, but they do not erase the debt itself or the time it can take to fix a mistake.

Christian Velitchkov, Unsplash

Christian Velitchkov, Unsplash

Fixing A Bad Bill Takes Time

The CFPB advises consumers to dispute inaccurate information on their credit reports and with debt collectors when needed. That can mean letters, records, deadlines, and follow-up. If the utility account never should have been your responsibility in the first place, that is a lot of cleanup for a favor.

This Can Also Hurt Future Housing Plans

Landlords and property managers often check credit reports during the rental process. A collection account tied to unpaid utilities can become a red flag. If you are planning to move, buy a car, or apply for a mortgage, this is exactly the kind of avoidable problem you do not want.

Parents May Have Real Reasons For Asking

Sometimes parents ask because their own credit is shaky, they have an old unpaid utility balance, or the company wants a deposit they cannot afford right now. Those are real problems. But the problem does not disappear just because it gets shifted into your name.

A Utility Deposit May Be Safer Than Taking Over The Account

If the real issue is a deposit, paying that deposit as a gift may be less risky than opening the utility account in your own name. Policies vary by company and state, so the account holder should ask what options are available. In many cases, solving the exact problem is better than taking on the full liability.

Ask One Key Question First

Why can they not keep the utilities in their own name. The answer matters. If the issue is temporary cash flow, there may be safer ways to help. If the issue is a history of unpaid bills, that is a loud warning sign.

If There Is A Past-Due Balance, Get The Facts

Ask which utility company is involved, what service address is on the account, how much is owed, and whether a deposit or prior balance is blocking service. You need specifics, not vague promises. This is one of those moments when direct questions can save you from a long financial headache.

There May Be Energy Assistance Available

The federal Low Income Home Energy Assistance Program, known as LIHEAP, helps eligible households with home energy costs. The Administration for Children and Families says the program can help with heating and cooling bills, energy crises, and weatherization in some cases. If your parents qualify, that route is much safer than using your credit as a backup plan.

Payment Plans May Solve The Problem

Many utility companies offer payment arrangements or budget billing for customers who are behind. State utility regulators often require or encourage consumer protections and complaint processes. Before you put your name on anything, your parents should ask the utility and the state regulator what hardship options are available.

Some Households May Have Extra Protections

Some states and utilities have protections for seniors, medically vulnerable customers, or households facing shutoffs during extreme weather. These rules vary a lot by location. That is another reason to contact the utility directly instead of assuming the only answer is using someone else’s name.

A Verbal Promise Is Not A Safety Net

You may hear, “We will pay you back every month,” and they may mean it. But if money gets tight, the company will still look to the person named on the account. Family trust does not change the legal responsibility attached to your name.

If You Want To Help, Choose A Safer Way

You could offer a fixed amount each month instead of taking responsibility for the whole bill. You could help them apply for assistance, call the utility with them, or cover a deposit as a one-time gift if you can afford it. Those options let you help without putting your own credit on the line.

Another Smart Move Is Paying The Utility Directly

If you are worried the money might get used for something else, ask whether you can make a payment straight to the utility company. Many companies allow one-time guest payments online or by phone. That can help keep service on without making you the account holder.

Boundaries Are Not The Same As Abandoning Someone

Saying no to this request does not mean you do not care about your parents. It means you understand that mixing your credit with someone else’s household bills can create long-term problems. You can be generous and still protect yourself.

If You Are Still Considering It, Get Everything In Writing

You should know the exact utility, the expected monthly cost, any deposit required, and what happens if the bill goes unpaid. Check whether the company even allows a non-occupant to open the account and what liability terms apply. Written details can reduce confusion, but they do not remove the risk.

Also Keep An Eye On Your Credit Reports

If your name is tied to any account that could go wrong, checking your credit becomes even more important. AnnualCreditReport.com is the official site authorized by federal law for free credit reports from Equifax, Experian, and TransUnion. Looking at your reports regularly can help you spot collection activity or account issues before they get worse.

What The Practical Answer Usually Looks Like

For most people, the safest answer is no, do not put utilities for someone else’s home in your name. The risk is yours, but the control is not. If you want to help, offer money you can afford to lose, help them work with the utility, or point them toward assistance programs.

The Kindest Choice May Also Be The Safest One

A financial favor can turn into resentment fast when bills are missed and collection notices start showing up. Clear boundaries now can prevent bigger family conflict later. Helping your parents find a solution is generous, but becoming legally responsible for their utilities is a risk you do not have to take.