When Budgeting Feels Like A Buzzkill

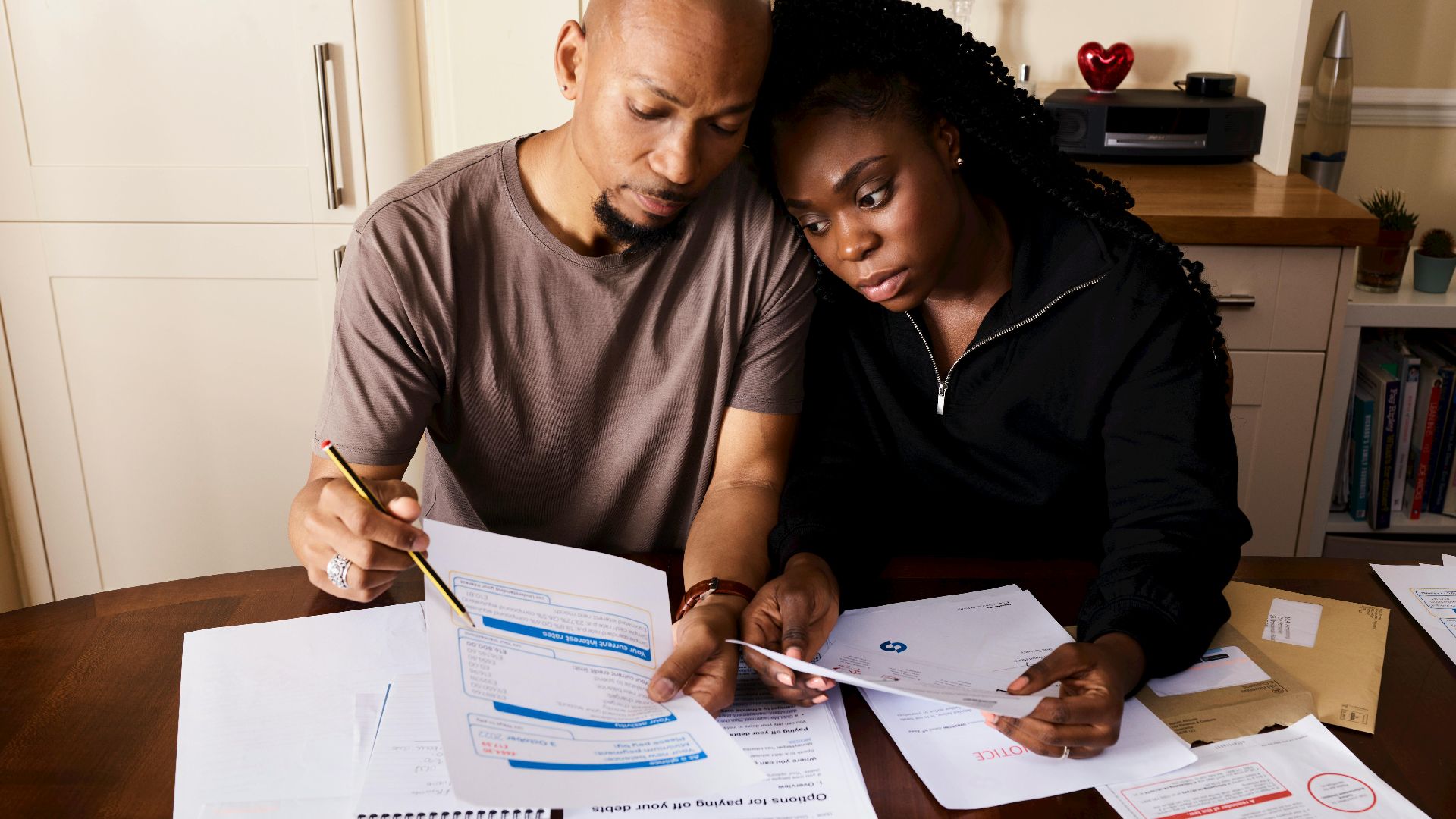

If your partner says budgeting kills the fun of money, you aren't alone. Plenty of couples clash because one person wants freedom and the other wants a plan. The bigger question is not whether budgeting is boring, but whether the two of you can make decisions together without secrecy, chaos, or resentment.

The Real Red Flag Is Not Hating Spreadsheets

Disliking budgets by itself is not automatically a major red flag. Some people connect budgets with stress, control, or childhood money problems. What matters more is whether your partner is willing to talk openly, agree on priorities, and stick to basic money decisions.

Why Money Fights Hit So Hard

Money fights often feel bigger than the dollars involved because they touch security, freedom, and power. Research from the American Psychological Association has long found money to be a major source of stress for many adults in the United States. That emotional charge is why a simple talk about takeout or shopping can turn into a fight about trust.

Harrison Keely, Wikimedia Commons

Harrison Keely, Wikimedia Commons

What Experts Mean By Financial Compatibility

Financial compatibility does not mean you both love cutting coupons or tracking every coffee. It means your habits can work together without hurting the household. The Consumer Financial Protection Bureau has stressed that healthy money management in relationships depends on communication, shared understanding, and planning for goals and bills.

G. Edward Johnson, Wikimedia Commons

G. Edward Johnson, Wikimedia Commons

Fun Money Is Not The Problem

Wanting room for fun is reasonable. Many financial planners encourage couples to build guilt-free spending into their system so neither person feels trapped. A plan with no room for enjoyment often fails because it feels punishing from the start.

But Refusing Any Plan Changes The Story

The bigger concern starts when a partner rejects every kind of structure. If they will not talk about bills, savings, debt, or limits, you are no longer arguing about style. You are dealing with someone who may not want to share responsibility, and that can create real risk.

Researchers Have Studied Money Conflict For Years

One often-cited study came from Kansas State University in 2012, when researchers found that money arguments were a top predictor of divorce in their study. Published in Family Relations, the research found that fights about money were often more intense and harder to resolve than other conflicts. That does not mean every budget fight ends a relationship, but it does mean ongoing money tension deserves attention.

Why Budgeting Can Feel Threatening

For some people, a budget sounds like surveillance instead of teamwork. They may hear, “You cannot be trusted,” instead of, “Let’s make a plan.” If your partner reacts strongly, it can help to ask what budgeting means to them emotionally before arguing over the numbers.

There Is More Than One Way To Budget

A budget does not have to mean a giant spreadsheet with endless categories. The CFPB and many nonprofit counselors describe simpler systems, including tracking fixed bills, setting savings goals, and leaving flexible room for personal spending. A partner who hates traditional budgets may still be open to something lighter.

A Spending Plan Might Sound Better

Sometimes the word “budget” is the problem. Calling it a spending plan can shift the tone from restriction to intention. The math stays the same, but the wording can make a defensive partner more willing to talk.

The Numbers You Cannot Ignore

If you share rent, a mortgage, children, or debt, avoiding a plan can cause problems fast. The Federal Reserve has repeatedly reported that many adults would have trouble covering an unexpected expense with cash or its equivalent. That makes basic planning less about being strict and more about protecting both people from preventable emergencies.

AgnosticPreachersKid, Wikimedia Commons

AgnosticPreachersKid, Wikimedia Commons

Ask Whether They Avoid Or Just Resist

There is a big difference between someone who jokes about budgeting and someone who avoids basic facts. Do they know what they earn, what they owe, and when bills are due? A partner who refuses to face reality is a much bigger concern than one who just prefers a looser system.

Look For Transparency First

Transparency is usually the make-or-break issue. Healthy couples do not need matching money personalities, but they do need honest information. Hidden accounts, secret debt, unexplained spending, and defensiveness around normal questions can point to a trust problem that goes far beyond budgeting.

Vodafone x Rankin everyone.connected, Pexels

Vodafone x Rankin everyone.connected, Pexels

Debt Can Turn This From Annoying To Dangerous

If your partner has high-interest debt and still rejects planning, the stakes rise quickly. The National Foundation for Credit Counseling has long warned that failing to track spending and debt can deepen financial stress and slow payoff. In a shared household, one person’s avoidance can hurt both credit, both savings goals, and both stress levels.

Red Flags That Matter More Than The Budget Itself

Watch for patterns like lying about purchases, borrowing money without talking about it, missing bills, draining savings, or pushing you to spend more than you can afford. Those are stronger warning signs than simply saying, “I hate budgeting.” The issue is not whether they like money apps. It is whether their behavior is honest, steady, and safe for a shared future.

Different Money Styles Can Still Work

Many couples do just fine with one saver and one spender. The key is setting rules that protect the household while leaving room for independence. That might mean shared goals for the essentials and separate personal spending accounts so no one feels watched all the time.

Try The Bare Minimum Version First

If your partner shuts down at the thought of a full budget, start smaller. Agree on monthly bills, savings goals, debt payments, and a set amount of personal spending for each of you. That simple setup often covers the biggest risks without making the process feel overwhelming.

Set A Date With The Numbers

Money talks usually go better when they are planned instead of launched in the middle of an argument. Pick a calm time, bring the account balances and bills, and frame the talk around shared goals. The point is to solve problems together, not to catch each other doing something wrong.

Rhoda Baer (Photographer), Wikimedia Commons

Rhoda Baer (Photographer), Wikimedia Commons

Use Goals That Feel Worth It

A budget gets easier to accept when it is tied to something concrete. Think a vacation, a home down payment, a debt-free date, or a stronger emergency fund. People are more likely to stick with a plan when it feels like a path to freedom instead of a list of punishments.

Keep Some Money Fun On Purpose

This is where your partner may have a point. A plan with no room for fun is hard to keep and easy to resent. Building in guilt-free spending can protect both your relationship and your discipline.

When Refusal Turns Into Control

Be careful if your partner mocks your concerns, shuts down every conversation, or tells you to just relax while expecting you to deal with the consequences. That dynamic can turn controlling when one person gets all the freedom and the other gets all the stress. Healthy compromise means both people adjust.

What If One Person Earns More

Income gaps can make budgeting fights more charged. The higher earner may feel entitled to more freedom, while the other partner may feel exposed or powerless. A fair system should account for each person’s responsibilities and dignity, not just who earns more.

Joint Accounts Need Joint Rules

If money is pooled, the need for some kind of structure becomes even more important. Shared accounts without shared expectations are a setup for confusion and blame. You do not need a long rulebook, but you do need clear agreements on bills, savings, and spending limits.

Separate Accounts Are Not A Magic Fix

Keeping finances separate can reduce tension for some couples, but it does not remove the need for honesty and planning. Shared life still creates shared costs. If one partner refuses to budget at all, separate accounts may hide the problem rather than fix it.

When To Get Outside Help

If every money talk turns into a dead end, outside help can make a difference. A nonprofit credit counselor, financial therapist, or couples therapist may bring structure and language that feel less personal. The Financial Therapy Association and accredited counseling groups exist because money stress often mixes emotional issues with practical ones.

The Question To Ask Before You Panic

Ask yourself this: Is your partner saying, “I do not want a strict budget, but I will work on a plan with you,” or are they saying, “I refuse limits, discussion, and accountability”? The first is a solvable difference in style. The second can be a real red flag.

Your Gut Should Not Do All The Work

It is easy to second-guess yourself if your partner acts like you are overreacting. Let the facts lead. Look at missed payments, debt trends, savings progress, and whether your agreements are actually being kept.

The Bottom Line On The Red Flag Question

A partner who dislikes budgeting is not automatically bad news. A partner who rejects transparency, responsibility, and compromise may be. If money is becoming a source of secrecy or instability, take that seriously now, because financial stress can turn small cracks into expensive problems.