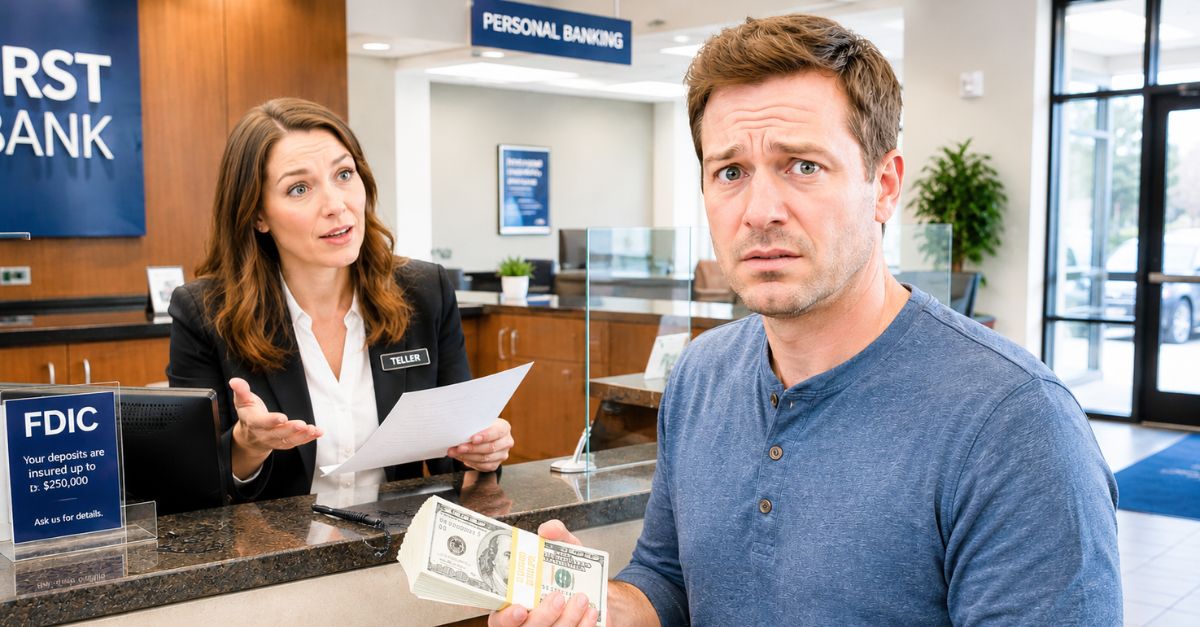

The Question That Throws People

You walk into your bank with a big stack of cash, and the teller suddenly starts asking personal questions. It can feel invasive, especially if the money really is yours and you're just trying to deposit it. But the bank isn't simply being nosy. It's following very real federal anti-money laundering rules that require it to understand certain cash transactions—even yours.

Why Your Bank Starts Asking

Banks in the United States are required to help detect money laundering, tax evasion, fraud, and other financial crimes. Much of that duty comes from the Bank Secrecy Act, which Congress passed in 1970. Over the years, the law has been expanded and enforced through rules from the U.S. Treasury Department and its Financial Crimes Enforcement Network, better known as FinCEN. That is why an ordinary cash deposit can quickly turn into a compliance check.

The Law Behind It

The Bank Secrecy Act, often called the BSA, created recordkeeping and reporting rules for financial institutions. According to the Office of the Comptroller of the Currency, banks must set up anti-money laundering programs and monitor for suspicious activity. The point is not to hassle regular customers. The point is to create a paper trail when cash activity could be tied to crime.

The $10,000 Rule Everyone Hears About

One of the best-known rules covers cash transactions over $10,000. Banks generally must file a Currency Transaction Report, or CTR, for cash deposits, withdrawals, currency exchanges, or other cash payments that go over $10,000 in a single business day. FinCEN says the report helps law enforcement track large cash movements. It does not mean the transaction is illegal. It means the bank has a reporting duty.

It Is Not Just About One Deposit

The reporting threshold can also apply to multiple cash transactions added together on the same business day. If a customer makes several deposits that total more than $10,000, the bank may treat them as one transaction for CTR purposes. FinCEN addresses aggregated transactions in its guidance and forms. That is one reason breaking up deposits usually does not keep a transaction off the radar.

Yes, Your Identity Matters

When a bank files a Currency Transaction Report, it needs identifying details. FinCEN's CTR rules include information such as your name, address, date of birth, and taxpayer identification number. The bank may also ask for your occupation or business. Those questions help it complete the required report correctly.

Where The Money Came From Matters Too

A bank may ask about the source of funds because understanding customer activity is part of anti-money laundering compliance. If a deposit looks unusual for your account, the bank may want some context. Maybe you sold a car, run a cash business, received insurance money, or inherited funds. A simple explanation can help the bank decide whether the transaction fits your normal pattern.

This Is Also About Suspicious Activity Reports

The bigger issue for banks is not just the CTR. It is whether they might also need to consider filing a Suspicious Activity Report, or SAR. The Office of the Comptroller of the Currency says banks are expected to file SARs when they detect known or suspected criminal violations or suspicious transactions. If your explanation does not match the activity, the bank may take a closer look.

Banks Usually Cannot Tell You If They Filed A SAR

One of the stranger parts of the system is that federal law generally bars banks from telling a customer that a Suspicious Activity Report was filed. FinCEN makes that confidentiality rule clear. So if a bank seems vague about why it is asking certain questions, that may be part of the reason.

Structuring Can Make A Bad Situation Worse

Some people think the smart move is to deposit $9,000 today and another $9,000 later to avoid the $10,000 report. That can create a separate problem called structuring. The Internal Revenue Service says structuring means breaking up transactions to dodge reporting requirements, and it is illegal. Even if the cash itself is legitimate, trying to avoid the reporting rule can create serious trouble.

The Rule Is Old, But It Is Still Enforced

The Bank Secrecy Act dates back to 1970, but banks still actively enforce its requirements today. FinCEN, which was established in 1990 and became a Treasury bureau in 1994, oversees many of these reporting systems. After the USA PATRIOT Act of 2001, customer identification and anti-money laundering rules became even stronger. In other words, this is not some temporary banking trend.

What The Bank Is Looking For

Banks build profiles based on what they know about your account and your usual transactions. If you normally get paid by direct deposit and then suddenly show up with $18,000 in cash, that is likely to get attention. If you run a restaurant, barbershop, food truck, or another cash-heavy business, larger cash deposits may be easier to explain. Context matters more than many people realize.

Legal Cash Is Still Cash

Depositing a large amount of legal cash is not, by itself, a crime. The problem is that banks cannot tell whether cash is legitimate just by looking at it. That is why they ask about the source, purpose, and expected activity. Your answers help them separate everyday life from possible red flags.

Common Reasons For Large Cash Deposits

There are plenty of ordinary reasons for a big deposit. You may have sold a vehicle, received payment from a private sale, run a cash-based small business, collected rent in cash, or withdrawn money earlier and are now putting it back. The bank may ask for supporting details or documents. That can be frustrating, but it often helps move things along.

Centre for Ageing Better, Pexels

Centre for Ageing Better, Pexels

Documents That Can Help

If the cash came from a sale, bring a bill of sale or receipt. If it came from your business, consider bringing deposit logs, invoices, or sales records. If it came from an insurance claim, legal settlement, or estate distribution, keep the official paperwork handy. Clear records can make the bank more comfortable and cut down on back-and-forth.

Your Bank Has To Know Who You Are

Another reason for personal questions is the Customer Identification Program requirement under federal law. Banks must form a reasonable belief that they know the true identity of each customer. The FDIC says this process includes collecting identifying information and verifying it. That system supports broader anti-money laundering monitoring.

Some Accounts Get More Attention

Business accounts, money services businesses, and accounts with unusual cash patterns often get deeper review. Banks may also watch politically exposed persons, high-risk industries, or customers tied to international transactions more closely. Those risk-based reviews are a standard part of compliance programs. They do not automatically mean the customer did anything wrong.

A Teller May Just Be Following Procedure

The questions you hear at the branch are often driven by bank policy, not personal suspicion from the employee standing in front of you. Tellers and branch staff are trained to collect facts when transactions hit certain thresholds or trigger alerts. In many cases, they are required to document your answers. So while it may feel personal, it is often just procedure.

Refusing To Answer Can Cause Problems

You are not always legally required to answer every question a bank employee asks right away, but refusing to cooperate can lead the bank to decline the transaction, restrict the account, or review the relationship. Private banks have broad control over account management, as long as they follow the law and their own policies. If they cannot get comfortable with the transaction, they may decide not to accept it. That is the practical reality many customers run into.

Could The Government See This Information

Potentially, yes. CTRs and SARs are filed with FinCEN, which shares information with law enforcement and other authorized agencies. The reporting system exists so investigators can spot patterns that may point to crime. That does not mean every large cash deposit leads to an investigation. It means the information can become part of a larger database used to detect financial crime.

Privacy Concerns Are Understandable

Many customers do not like this system, and that reaction makes sense. Financial privacy advocates have long argued that broad reporting rules pull in many innocent people. But under the current rules, banks can face penalties if they fail to report or investigate when required. That gives compliance departments every reason to be cautious.

What To Do Before Making A Large Deposit

If you know a big cash deposit is coming, call your bank first. Ask what identification or documents they may want and whether the branch has any limits or special procedures for large cash transactions. A little notice can make the visit much smoother. It can also reduce the chance of delays or confusion.

Do Not Try To Beat The System

The worst move is trying to game the reporting rules by splitting up cash deposits or giving vague answers. Banks are trained to spot patterns that look like avoidance. The IRS warns that structuring is illegal even when the money was earned lawfully. Honesty and documentation are usually much safer than trying to be clever.

If The Cash Came From A Business, Be Ready

Cash-heavy businesses deal with this issue all the time. Good bookkeeping matters because repeated large deposits can bring routine questions. Keep sales records, daily cash logs, and tax documents organized. If your records are clean, answering the bank gets a lot easier.

If The Money Was A One-Time Windfall, Say So

Banks do not expect every customer to have the same transaction pattern forever. A one-time event like selling a motorcycle, getting paid for collectibles, or clearing out a family safe deposit box can explain a large deposit. The key is to be clear and consistent. If possible, bring proof that connects the cash to the event.

What If The Bank Still Seems Uneasy

Sometimes a bank may place a hold, ask you to speak with a manager, or request more documents later. That does not necessarily mean you are being accused of anything. It often means the bank wants a better record of why the cash showed up. Staying calm and responding clearly usually works better than getting defensive.

The Bottom Line On Those Personal Questions

Your bank cares where your money came from because federal law requires it to care. Large cash deposits can trigger mandatory reports, extra identity checks, and questions meant to detect suspicious activity. If your cash is legitimate, the best approach is simple: be honest, bring documents, and understand that the bank is following rules that have been in place for decades.