Understand The Situation

Your loan was sold to another company, and somewhere in that transfer, your payments got misreported. Now the new lender claims you missed payments and is piling on late fees. It’s an unfair and damaging situation, but you have rights and options to fix this problem.

Why Loans Get Sold

Lenders often sell loans to free up cash and reduce risk. The new company becomes your loan servicer, and is now responsible for collecting payments. Legally, your contract terms don’t change, but mistakes in the transfer process can cause some serious confusion about what you’ve already paid.

How Payments Get Misreported

Misreporting happens when the old lender fails to transfer payment records properly, or when the new lender’s system misapplies your payments. Sometimes payments made during the transition period get “lost in transit.” The result is wrong balances and mistaken claims that you owe money you don’t.

Impact On Credit Score

If the misreported payments appear as missed, your credit score can of course take a serious hit. Even one or two falsely reported late payments can drop your score by dozens of points. That affects your ability to get loans, mortgages, or even favorable interest rates going forward.

The Cost Of Late Fees

On top of the credit damage, late fees can add a new and unexpected financial burden. New lenders may add on charges for each alleged missed payment, which quickly adds on hundreds or even thousands of dollars. These charges are often non-refundable unless you can challenge them and prove they were wrongly applied. Let’s look at the best ways to do that.

Photo By: Kaboompics.com, Pexels

Photo By: Kaboompics.com, Pexels

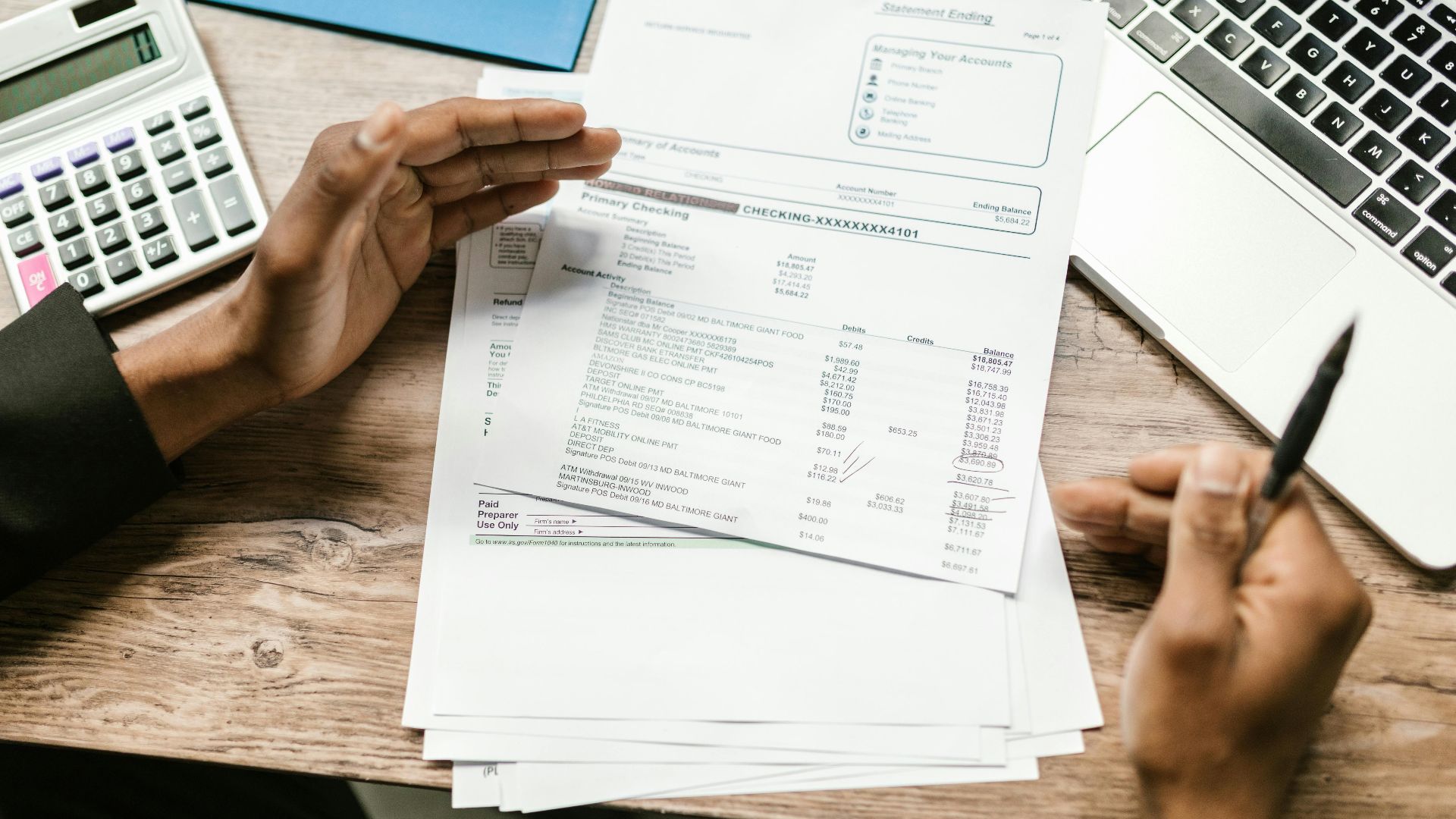

Review Your Loan Documents

Start by putting together all your original loan documents and recent statements. You’ll absolutely need proof of your payment history to fight this. Keeping your own records helps you demonstrate what you actually paid versus what the new lender is claiming. We can’t stress this enough: documentation is your strongest defense.

Collect Proof Of Payment

Bank statements, canceled checks, and online confirmation numbers are all key pieces of evidence. If you made payments electronically, download and print off the transaction histories. Your goal is to create a clear indisputable timeline demonstrating that you did, in fact, make on-time payments, and that the lender’s records are flawed.

Contact The Old Lender

Reach out to your old lender and get them to send you a complete record of your payment history. They are legally required to keep accurate records. If the misreporting happened on their end, you’ll need written confirmation from them to help tidy up the errors with the new lender.

Contact The New Lender

Once you’re done with the old lender, contact the new lender in writing. Explain the situation and include proof of payment. Request them to correct the misapplied payments and removal of late fees. Always keep copies of correspondence. Written requests are important as they generate a paper trail that’s harder for lenders to ignore.

Photo By: Kaboompics.com, Pexels

Photo By: Kaboompics.com, Pexels

Escalate With A Complaint

If the lender doesn’t respond, you need to immediately escalate the issue. File a complaint with the Consumer Financial Protection Bureau (CFPB). The CFPB forwards complaints to lenders. This should motivate them to sit up and take an active interest in your situation. The added layer of regulatory pressure should most likely see your dispute get attended to.

Tony Webster, Wikimedia Commons

Tony Webster, Wikimedia Commons

Dispute With Credit Bureaus

If your credit report shows false late payments, file disputes with the three major credit bureaus: Equifax, Experian, and TransUnion. Furnish them with supporting documents. By law, bureaus have to investigate within 30 days. If the lender can’t provide proof of its own reporting, the negative marks on the credit score have to be removed.

Understand RESPA Protections

The Real Estate Settlement Procedures Act (RESPA) requires lenders to handle transfers fairly. If you send a “qualified written request,” by law the lender has to acknowledge your inquiry within five days and take action within 30. This is a powerful tool to force lenders to go back and fix their mistakes.

Tingey Injury Law Firm, Unsplash

Tingey Injury Law Firm, Unsplash

Know Your FDCPA Rights

Under the Fair Debt Collection Practices Act (FDCPA), lenders and servicers cannot attempt to collect debts you don’t actually owe. If late fees or balances are ballooning because of errors, trying to collect them may break federal law. Having this knowledge in hand can strengthen your legal arguments.

Consider Legal Steps

If the situation still isn’t resolved, consider talking to a consumer protection attorney. Lawyers who specialize in credit reporting or debt collection will be able to advise you on whether to sue for damages. Sometimes, just the threat of legal action can push lenders to fix errors quickly.

Ask For Fee Reversals

Don’t assume late fees are written in stone. If you give proof that the numbers are misreported, lenders will as often as not reverse the charges. Be polite but persistent; many companies have “goodwill” policies in place that allow them to waive or refund fees once errors are found and verified.

Photo By: Kaboompics.com, Pexels

Photo By: Kaboompics.com, Pexels

Stay Current On Payments

Even when you’re disputing errors, continue making ongoing payments. If you fall behind now, it will actually create real late fees and weaken your case. Always pay what you legitimately owe, even if the other past charges are in dispute. It minimizes your problems and keeps your account in better standing while you work things out.

Document Everything Carefully

It should go without saying, but keep detailed records of every phone call, letter, or email that you exchange with lenders. Write down names, dates, and give summaries of conversations (if possible). The better your documentation, the more it will help you if you need to escalate to regulators, credit bureaus, or the courts.

Long-Term Credit Recovery

Even if errors do short-term damage to your credit score, setting them straight will help your profile bounce back. Once the false late payments are got rid of, your score will rebound. Keep on practicing good credit habits: low balances; on-time payments; and monitoring your reports regularly.

Prevent Future Confusion

Any time your loan is sold, you should immediately get in touch with the new servicer to confirm balances, due dates, and account numbers. Set up payments with confirmation tracking. Staying proactive will reduce the risk of screw-ups and protect you from future disputes.

Photo By: Kaboompics.com, Pexels

Photo By: Kaboompics.com, Pexels

Move Forward With Confidence

Having your loan sold may be a bit unsettling, but errors can be fixed. By documenting payments, disputing errors as soon as possible, and making use of legal protections, you can stop incorrect late fees and repair credit damage. Acting quickly and persistently is the best way to ensure that this setback doesn’t define your financial future.

You May Also Like:

I bought a $60K truck with a 9-year loan at 11% interest. Did I just wreck my finances?