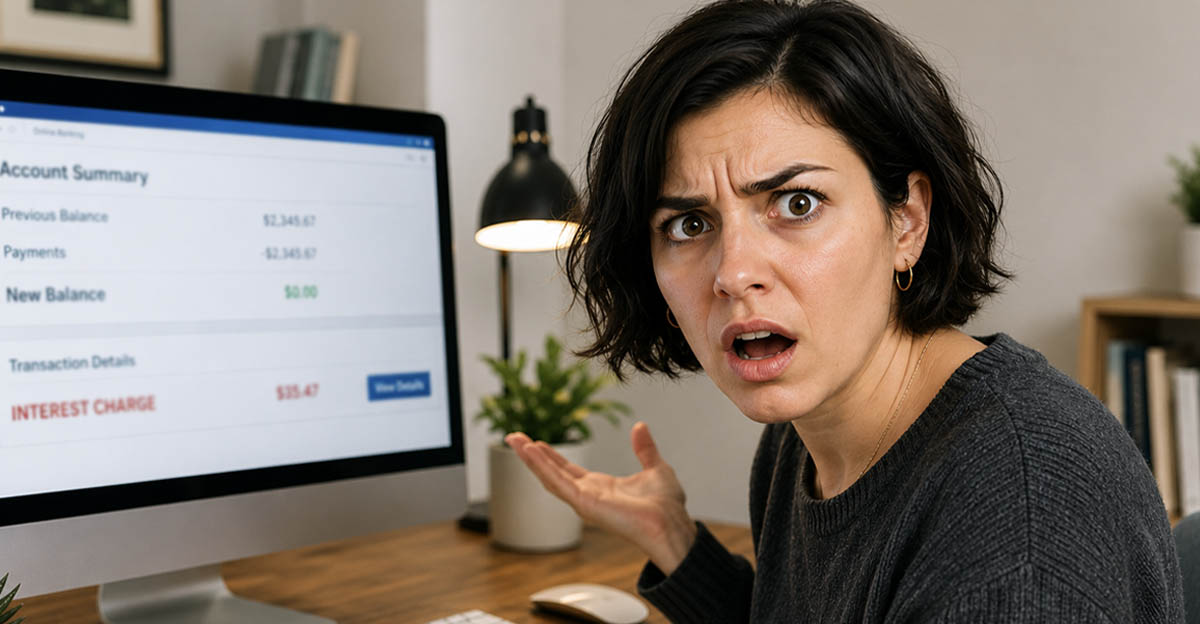

I Paid Everything They Asked For. Now There’s More?

You finally pay off your credit card or loan balance, breathe a sigh of relief, and then the next statement arrives with…more interest charges. Now, it feels like the lender is just inventing charges to squeeze more money out of you. The frustrating reality is that this situation is actually pretty common, especially with credit cards. But whether the charge is legitimate depends on why it appeared, and in some cases, you absolutely can dispute it.

This Is Often Called “Residual” Or “Trailing” Interest

A lot of people don’t realize that interest on credit cards usually accrues daily, not just once a month. That means even if you pay your full balance, interest may still have accumulated between the statement closing date and the day your payment was processed. The leftover amount that appears afterward is often called trailing or residual interest.

Credit Cards Usually Don’t Stop Interest Immediately

Unlike a fixed monthly bill, credit card interest often keeps ticking daily until the issuer receives and processes the payoff amount. So even if you paid the statement balance exactly as shown, additional interest may have built up afterward.

Loans Can Have Similar Timing Issues

This doesn’t only happen with credit cards. Auto loans, personal loans, and mortgages sometimes have payoff timing differences too. If you request a payoff amount but the payment arrives later than expected, extra interest can sometimes appear.

Sometimes The Charge Is Legitimate

As annoying as it is, residual interest charges are often legal and disclosed in the account agreement. If the lender calculated the interest correctly under the terms you agreed to, disputing it may not succeed.

But Billing Errors Absolutely Happen Too

That said, lenders and credit card companies are not perfect. Processing mistakes, incorrect interest calculations, delayed payment posting, or system errors can create charges that are actually wrong. That’s why it’s worth reviewing the details carefully instead of assuming the company is automatically correct.

Step One: Check The Dates Carefully

The dates are everything here. Look at your statement closing date, payment date, and the date the payment officially posted. If interest accumulated before the payment fully processed, that may explain the charge.

Look At Whether You Paid The Full Statement Balance

Some people accidentally pay the “minimum due” or “current balance” instead of the exact statement balance required to avoid interest. Even a small remaining amount can trigger additional finance charges.

Grace Periods Matter A Lot

Many credit cards offer grace periods where no new interest accrues if you pay the statement balance in full every month. But once you carry a balance, you may temporarily lose that grace period entirely.

That’s Why Interest Can Suddenly Snowball

Once the grace period disappears, new purchases may start accruing interest immediately. That’s one reason trailing interest catches so many people by surprise after they finally pay everything off.

Step Two: Ask For An Explanation

Before escalating things, contact the lender and ask for a detailed breakdown of the interest charge. Sometimes the explanation reveals it’s standard residual interest. Other times, you may spot inconsistencies or errors.

Sometimes Companies Will Waive Small Charges

Here’s something many people don’t realize: if the remaining interest amount is small, customer service representatives will sometimes waive it as a courtesy, especially for long-time customers with good payment histories.

You Can Absolutely Dispute Actual Errors

If the interest calculation truly appears incorrect, you can dispute the charge directly with the lender. Under the Fair Credit Billing Act, consumers have rights to dispute certain billing errors on credit accounts.

Documentation Helps A Lot

Save statements, payoff confirmations, payment receipts, screenshots, and transaction histories. If the dispute escalates, having organized documentation makes a huge difference.

Payoff Quotes Are Important For Loans

For installment loans, lenders often provide official payoff quotes that include estimated interest through a specific date. If you paid later than that date, extra interest may have accrued legitimately.

Auto-Pay Timing Can Create Problems Too

Even automatic payments can sometimes post later than expected because of weekends, holidays, or processing delays. Those timing gaps occasionally generate small extra charges.

Credit Reporting Usually Isn’t Ruined Immediately

A lot of people panic that a tiny leftover interest amount will instantly destroy their credit. In many cases, there’s still time to resolve the issue before serious reporting consequences happen, especially if you act quickly.

Sometimes Paying One Final Small Amount Solves It

Unfortunately, in many legitimate trailing-interest situations, the simplest solution is just paying the final small amount owed. Once that clears, the account usually fully closes out.

But You Shouldn’t Ignore It Completely

Even if the amount seems tiny, unpaid balances can sometimes continue generating additional fees or interest if left unresolved. That’s why it’s smart to investigate rather than simply ignoring the statement.

So What Should You Do Right Now?

Start by reviewing your payment and statement dates carefully. Then contact the lender and ask exactly why the interest appeared. If it’s legitimate residual interest, you may simply need one final payment. But if the numbers don’t add up, you absolutely have the right to dispute potential billing errors.

Final Thoughts

Seeing interest charges after paying off your balance feels incredibly frustrating, especially when you thought you were finally done. In many cases, the charge turns out to be legitimate trailing interest caused by how daily interest accrues. But billing mistakes do happen, and you have every right to question charges that seem incorrect. The important thing is understanding why the interest appeared before assuming you’re stuck paying it.

You May Also Like:

My bank froze my account after I made one large deposit. Is that really legal?