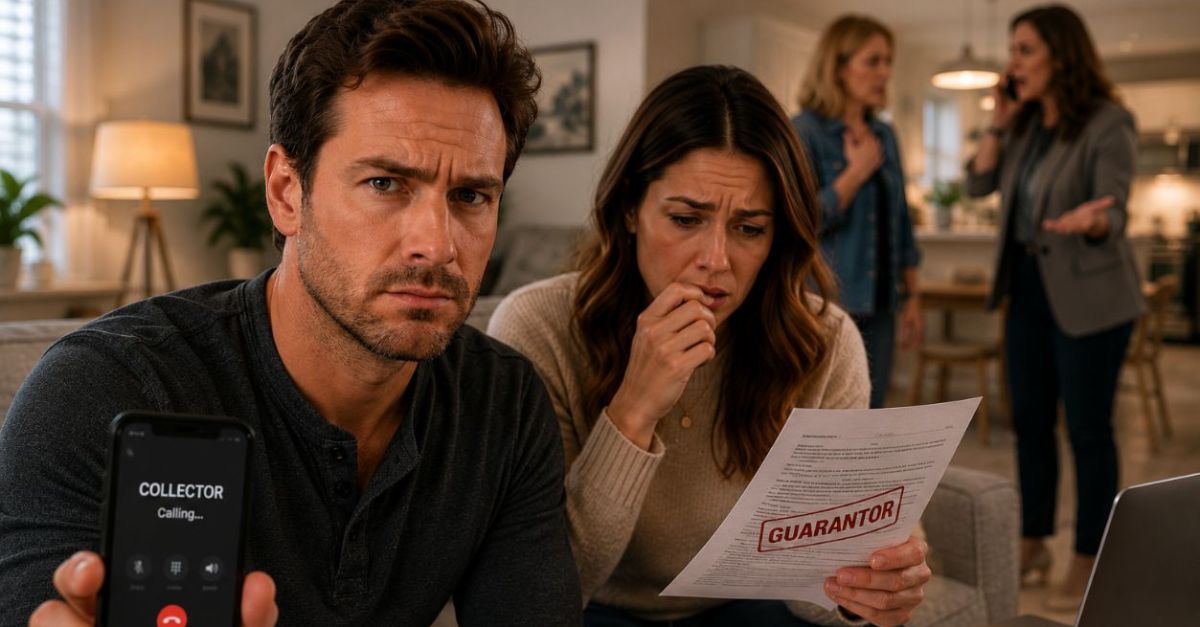

The Call That Changes Dinner

It often starts with a phone call that makes no sense. A collector asks for your spouse, mentions a loan you have never heard of, and suddenly your household feels exposed. If your wife secretly guaranteed a friend's debt, the big question is whether that problem can spill into your finances too. And what does it mean that she kept it secret?

What A Personal Guarantee Really Means

A personal guarantee is a promise to repay a debt if the original borrower does not. The Consumer Financial Protection Bureau explains that when someone cosigns or guarantees a loan, they can become fully responsible for it. In simple terms, your wife may be on the hook if her friend stopped paying.

Why Collectors Start Calling So Fast

Once a loan goes past due, lenders may turn to anyone who is legally responsible for repayment. That can include a guarantor, even if the guarantor never got any of the money. If your wife signed, the collector may have a legal reason to contact her about the unpaid balance.

Your Debt And Your Spouse's Debt Are Not Always The Same

Marriage does not automatically roll every debt into one shared bill. In many situations, debts stay with the person who signed for them. Whether this becomes a household problem depends a lot on state law, how the guarantee was signed, and whether any joint assets are exposed.

The Community Property Twist

This is where things can get complicated. In community property states, many assets and debts picked up during marriage may be treated as belonging to both spouses, though the exact rules vary by state. The National Conference of State Legislatures lists nine community property states: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin.

Why State Law Matters So Much

If you live in one of those nine states, a spouse's debt can sometimes affect community income or community assets. That does not mean every secret guarantee automatically becomes your personal debt. It does mean a creditor may have more ways to collect than it would in a separate property state.

Most States Use A Different System

Outside community property states, the usual rule is more straightforward. A debt generally belongs to the person who agreed to it, unless both spouses signed or the debt falls into a category treated as shared under state law. That can be a relief for a husband who never signed a guarantee himself.

Collectors Can Still Make Life Messy

Even if you are not legally responsible, collectors may still contact the household while trying to reach your wife. The Fair Debt Collection Practices Act puts limits on what debt collectors can do. The CFPB says collectors generally cannot harass, threaten, or lie about what is owed.

What They Can Ask You

A collector may contact third parties for limited location information, but the law puts tight limits on what they can say. They generally cannot lay out all the details of someone else's debt just because you answered the phone. If a collector starts oversharing or pressuring you personally, that is a warning sign.

The First Thing To Check

Do not guess about what was signed. Ask for the original loan documents, the personal guarantee, the payment history, and any notice of default. You need to know whether your wife signed as a cosigner, guarantor, or in some other role, because those labels can carry different legal effects.

Andrii Iemelianenko, Shutterstock

Andrii Iemelianenko, Shutterstock

Hidden Signatures Can Lead To Huge Surprises

Some guarantees are tucked into business loan papers, credit applications, or renewal documents. The Small Business Administration warns borrowers and guarantors to understand exactly what they are signing because a personal guarantee can put personal assets at risk. A favor for a close friend can turn into a long financial mess.

Is The Guarantee Even Enforceable

Not every collection demand is solid. The creditor should be able to show a valid agreement and prove your wife actually agreed to guarantee the debt. Missing signatures, fuzzy terms, or sloppy paperwork can matter, especially if the dispute ends up in court.

Why Timing Matters

Look closely at when the guarantee was signed and when the default happened. Those dates can affect notice rules, credit reporting timelines, and the statute of limitations for a lawsuit. When the story is vague and the pressure is high, dates and documents matter most.

Your Credit Is Not Automatically Hit

If you never signed and the account is not in your name, it should not just show up on your individual credit report. Under the Fair Credit Reporting Act, credit reporting has to be accurate and tied to the right consumer. Even so, it is smart to check your reports from all three major bureaus in case something was reported by mistake.

LIGHTFIELD STUDIOS, Adobe Stock

LIGHTFIELD STUDIOS, Adobe Stock

Joint Accounts Are A Different Story

If your wife used joint bank funds to make payments, or if a lender later reached a joint account through legal process, the damage can feel shared even if the legal duty is not. That is why couples sometimes learn too late that separate liability and shared money are a risky mix. A debt can stay hers on paper while still putting real pressure on the household budget.

Can A Creditor Take Our House

The answer depends on how the home is titled, what state you live in, and whether the creditor gets a judgment. In some situations, a creditor may be able to go after liens or other collection tools aimed at assets tied to the liable spouse. But homestead protections, tenancy rules, and exemption laws can change the result in a big way.

Wages Are Another Sensitive Area

If only your wife is liable, a creditor usually goes after her wages or assets, subject to state and federal limits. The Department of Labor explains that federal law caps how much of disposable earnings can usually be garnished in many debt cases. Whether your income can be touched depends on whether you are personally liable and how your state treats marital property.

If You Live In Texas Or California, Read Carefully

Community property rules get extra attention in states like Texas and California because marital income can be treated as community property. That can give creditors a wider target when one spouse owes a debt taken on during marriage. It is one reason local legal advice matters so much in cases like this.

Do Not Ignore A Summons

If the calls turn into a lawsuit, silence is the worst move. A court summons comes with deadlines, and missing them can lead to a default judgment. Once a creditor has a judgment, its collection options often grow.

LIGHTFIELD STUDIOS, Adobe Stock

LIGHTFIELD STUDIOS, Adobe Stock

Ask For Debt Validation Early

The CFPB advises consumers to ask for validation information so they can confirm the amount owed and the creditor's identity. This step can uncover errors, old accounts, or collectors chasing the wrong person. It also shifts the conversation back to paperwork instead of pressure.

Marriage Does Not Cancel Consent

It is easy to assume a spouse needed your permission to guarantee a friend's loan. Usually, adults can sign contracts on their own unless a specific asset or law requires both spouses' signatures. The emotional fallout may be personal, but the legal answer still comes down to the contract and your state's property rules.

What To Do In The First 48 Hours

Start by pulling credit reports, gathering bank records, and asking the collector for written notice. Then review how your money is held, especially any joint accounts that could become vulnerable. If the amount is serious, talk to a consumer law or debt defense attorney in your state right away.

Protect The Household Cash Flow

Think about moving automatic bill payments to an account that is clearly structured and understood, especially if there is concern about freezes or levies later. Do not hide assets or move money around in a panic, because that can create new legal problems. Focus on documentation, budgeting, and getting advice before making any big moves.

Watch For Collector Violations

Collectors cannot legally use harassment, obscene language, or false threats under federal law. Keep a written log of each call, note the date and time, and save voicemails and letters. Those details can matter if you need to file a complaint or defend yourself.

When A Friend's Crisis Becomes A Marriage Crisis

A secret guarantee is not just a legal issue. It can expose gaps in communication, trust, and financial planning inside a marriage. Before you can deal with the debt, you need the full paper trail and a clear picture of what was promised, when it was signed, and what assets might be at risk.

cottonbro studio, PexelsThe Bottom Line On Whether It Becomes Your Problem

cottonbro studio, PexelsThe Bottom Line On Whether It Becomes Your Problem

Someone else's debt does not automatically become yours just because you are married to the guarantor. But it can absolutely become your household's problem through shared accounts, community property rules, lawsuits, and pressure on family cash flow. The fastest way to get clarity is to verify the documents, check your state law, and get legal advice before the collector writes the next part of the story.