A Stack Of Old Savings Bonds Turned Up. Are They Still Worth Anything?

Finding old US savings bonds tucked away in a drawer, safe, or family filing cabinet can feel like discovering buried treasure. But once the excitement wears off, the questions begin. Are the bonds still earning interest? Have they already matured? Can they still be redeemed decades later? The good news is that many old savings bonds still have value, and finding out what they're worth is often easier than people expect.

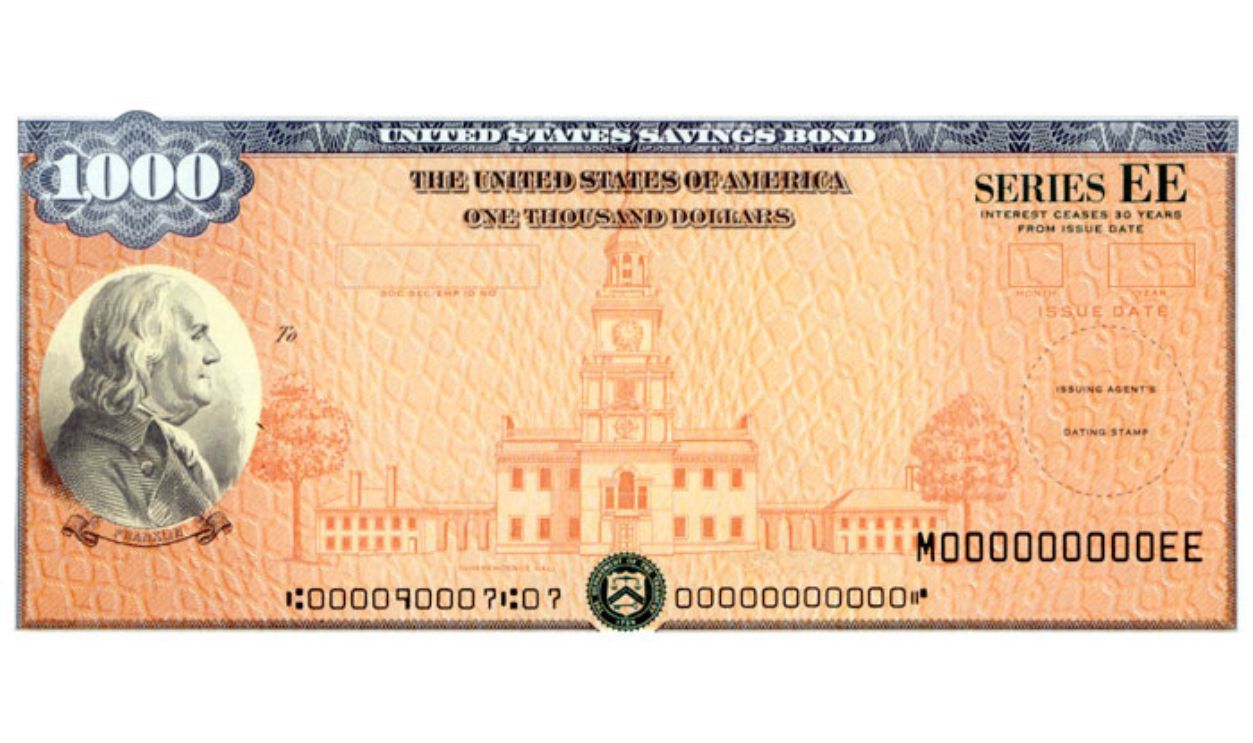

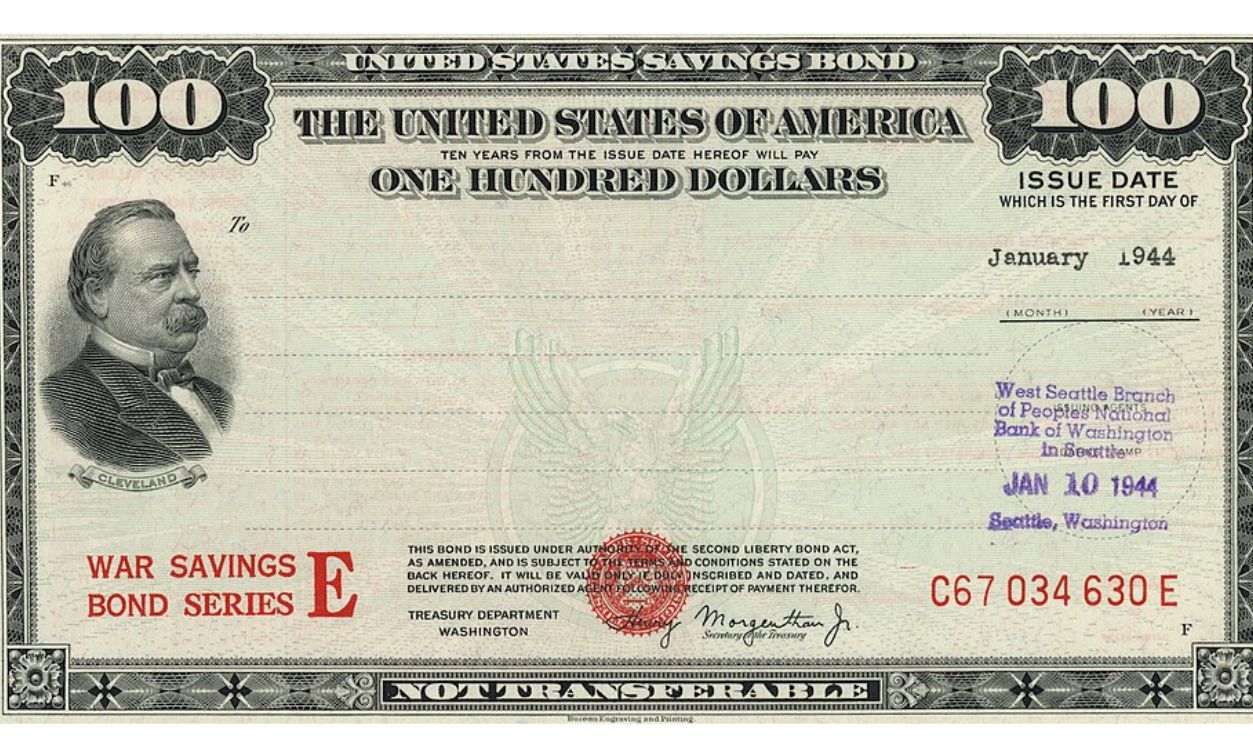

Start By Identifying The Bond Series

The first step is determining exactly what type of savings bond you have. The most common paper bonds are Series E, EE, I, and HH. The series name is usually printed on the front of the bond. Knowing the series is important because each one follows different interest rules and maturity periods.

United States Treasury, Bureau of Public Debt, Wikimedia Commons

United States Treasury, Bureau of Public Debt, Wikimedia Commons

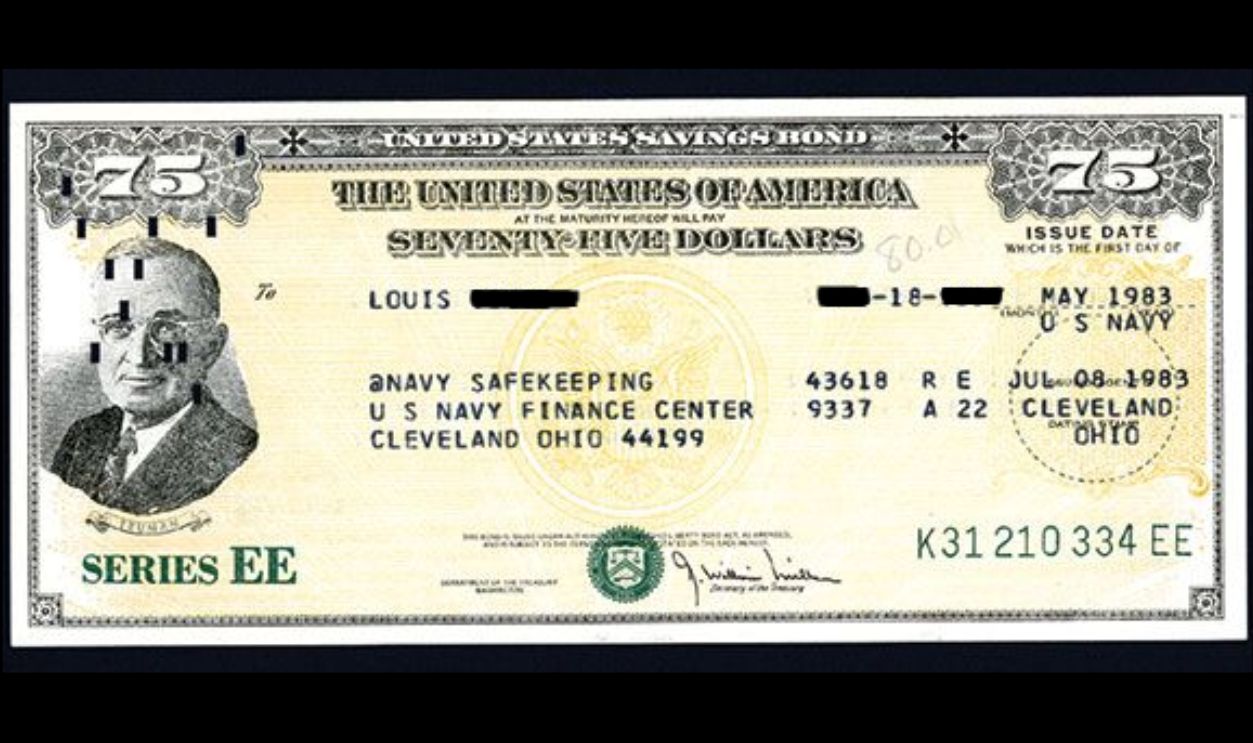

Check The Issue Date

The issue date appears on the front of the bond and plays a major role in determining its value. Different interest rates applied during different time periods, and some bonds stopped earning interest years ago while others continued growing for decades. Two bonds with the same face value may be worth very different amounts depending on when they were issued.

U.S. Department of the Treasury, Wikimedia Commons

U.S. Department of the Treasury, Wikimedia Commons

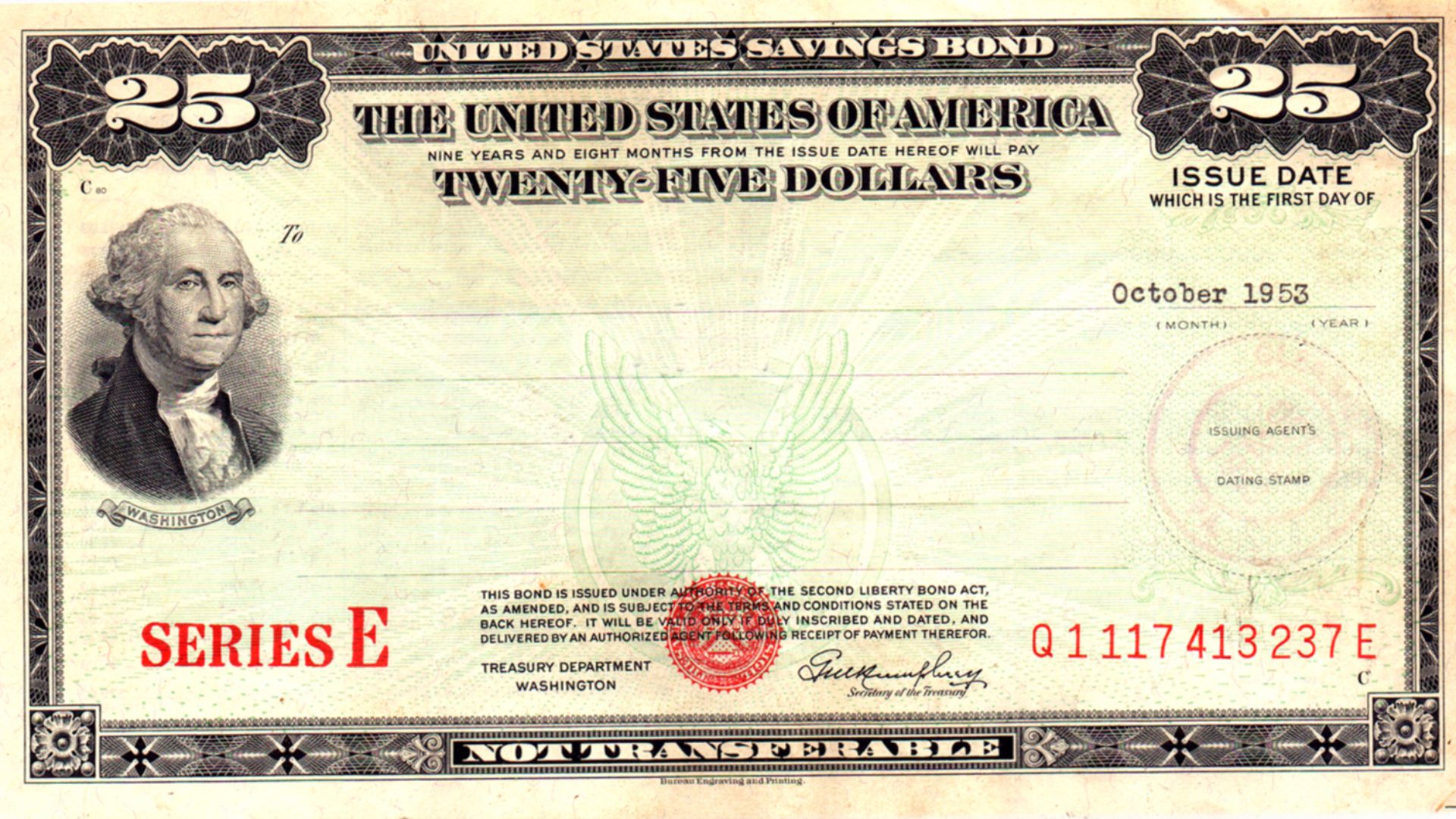

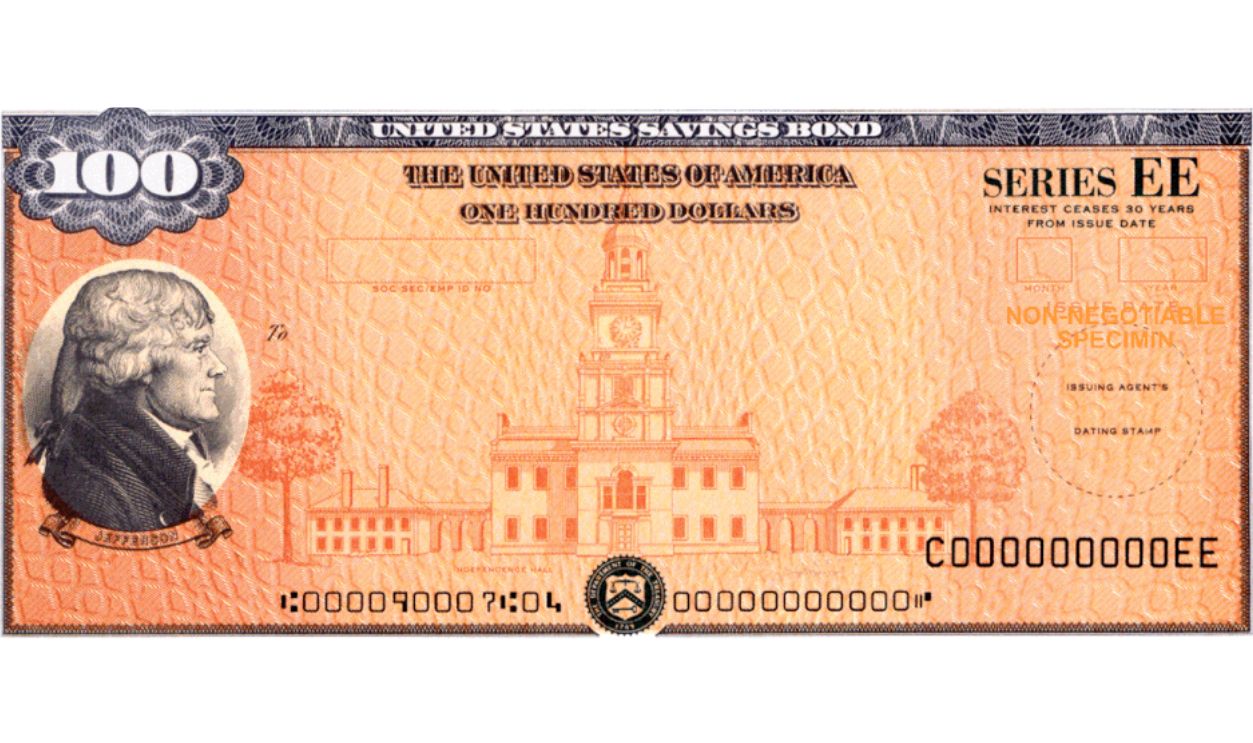

Face Value Isn't The Same As Current Value

Many older savings bonds were purchased for half of their face value. For example, a $100 bond may have originally cost only $50 and gradually grown over time. Other bonds were issued differently. Don't assume the amount printed on the bond reflects what it's worth today.

US Government, Wikimedia Commons

US Government, Wikimedia Commons

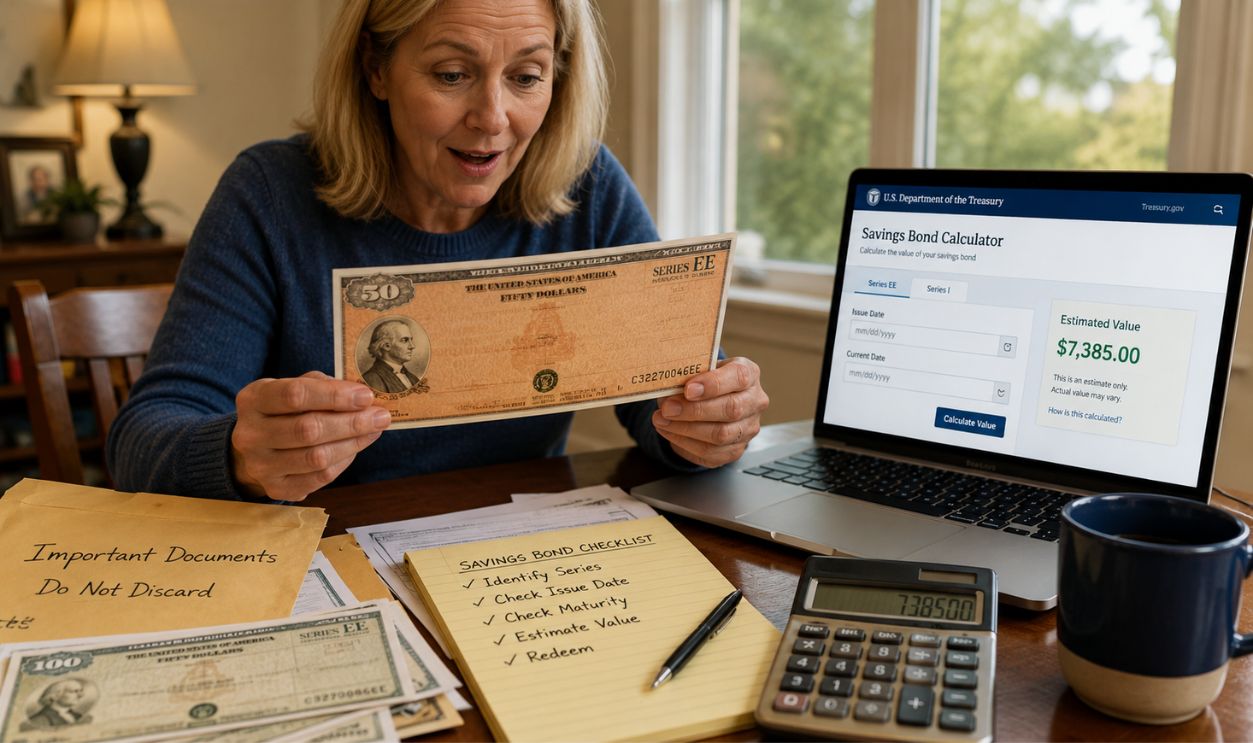

The Treasury Has A Free Savings Bond Calculator

One of the easiest ways to estimate the value of many paper savings bonds is by using the US Treasury's Savings Bond Calculator. By entering the bond series, denomination, and issue date, you can see its estimated current value, whether it is still earning interest, and when it reached final maturity. It's one of the most useful tools available for families sorting through old bonds.

Some Bonds Have Stopped Earning Interest

Savings bonds don't earn interest forever. Most eventually reach what's called final maturity, after which their value no longer increases. Even if the bond stopped growing years ago, it can usually still be redeemed for its final value. Many people are surprised to discover they've been holding mature bonds that haven't earned another penny in years.

Older Doesn't Mean Worthless

A bond from the 1960s or 1970s may look ancient, but that doesn't mean it's expired or invalid. Many older bonds still retain their redemption value even after they stop earning interest. If the bond hasn't already been redeemed, it generally remains redeemable by the rightful owner or eligible heirs.

United States Department of the Treasury, Wikimedia Commons

United States Department of the Treasury, Wikimedia Commons

Look Carefully At The Owner's Name

Ownership matters. Some bonds list a single owner, while others include a co-owner or a payable-on-death beneficiary. The names printed on the bond determine who has the legal right to redeem it. Before heading to a bank, verify exactly how ownership is listed.

Damaged Bonds Can Often Be Replaced

If a bond is torn, faded, partially destroyed, or difficult to read, don't assume it's worthless. The Treasury offers procedures for replacing lost, stolen, or damaged savings bonds. As long as enough information exists to identify the bond, replacement is often possible.

Lost Bonds May Still Be Recoverable

Many families know bonds once existed but can't find the original certificates. Fortunately, the Treasury may still be able to locate electronic records if enough identifying information is available. You'll typically need details such as the owner's name, Social Security number, approximate issue date, or other supporting information.

United States Department of the Treasury, Wikimedia Commons

United States Department of the Treasury, Wikimedia Commons

Banks May Not Redeem Every Bond

Years ago, redeeming savings bonds at a local bank was common. Today, not every financial institution offers this service, particularly for customers who don't bank there. Some banks redeem certain paper bonds for existing customers, while others direct people to the US Treasury instead. Calling ahead can save an unnecessary trip.

Carol M. Highsmith, Wikimedia Commons

Carol M. Highsmith, Wikimedia Commons

TreasuryDirect Handles Many Modern Transactions

The TreasuryDirect website serves as the primary online resource for many savings bond services. It provides information about redemption, conversions, replacements, ownership questions, and electronic savings bonds. Even if your bonds are paper certificates, TreasuryDirect often points you toward the correct procedures.

Taxes Still Matter

Interest earned on US savings bonds is generally subject to federal income tax, although state and local income taxes typically do not apply. Many people choose to defer paying federal tax until the bond is redeemed or reaches final maturity. If you're cashing in several bonds at once, it's worth understanding the potential tax consequences.

Education Benefits May Apply

In some situations, savings bond interest may qualify for federal tax exclusions when used for eligible higher education expenses. Specific rules apply regarding bond type, issue date, income limits, and how the proceeds are used. If college expenses are involved, it may be worth reviewing whether the Education Savings Bond Program applies.

Inherited Bonds Follow Special Rules

Families often discover savings bonds after the death of a parent or grandparent. Redeeming inherited bonds can involve additional paperwork depending on how ownership was structured and whether the estate has been settled. The process isn't necessarily difficult, but it may require supporting documents such as death certificates or probate paperwork.

Don't Rush To Redeem Everything

If the bonds are still earning interest, redeeming them immediately may not always be the best financial decision. Compare the bond's current interest rate with other savings options and consider your overall financial goals. Sometimes holding the bond a little longer makes sense, while other times cashing it in is the smarter move.

Organize Everything First

Before redeeming any bonds, create a simple inventory. Record the series, denomination, issue date, serial number, owner's name, and estimated value. This makes it much easier to decide which bonds have matured, which are still growing, and which require additional research.

Check For Duplicate Records

Families occasionally discover duplicate paperwork or redemption records along with old bonds. Before assuming every certificate has value, make sure it wasn't already redeemed years ago. If you're unsure, the Treasury can often help determine the bond's status.

Beware Of Scams

Because savings bonds involve government-issued securities, scammers sometimes target people searching for redemption information. Use official Treasury resources whenever possible and be cautious of anyone promising to unlock hidden value for an upfront fee. Most legitimate information is available directly from the government at no cost.

Electronic Conversion Is Available For Some Bonds

Certain paper savings bonds can be converted into electronic form through TreasuryDirect. Some owners prefer electronic records because they eliminate concerns about loss, theft, or physical damage. Conversion isn't required before redemption, but it may be convenient for long-term recordkeeping.

Keep Copies Of Everything

Before mailing bonds or submitting paperwork, make copies or take clear photographs of every certificate. Also save copies of any forms, correspondence, and mailing receipts. Good records can make resolving any future questions much easier.

If You're Missing Information, Don't Panic

It's common for families to discover bonds without knowing exactly when they were purchased or why they were issued. Fortunately, the Treasury can often work with incomplete information. As long as you provide as many details as possible, there may still be a path toward identifying and redeeming the bonds.

Professional Advice May Help With Large Collections

If you've inherited dozens of bonds or believe they represent a substantial amount of money, consulting a financial advisor, estate attorney, or tax professional may be worthwhile. They can help evaluate tax implications, estate issues, and redemption strategies, particularly when multiple heirs are involved.

Don't Leave Mature Bonds Sitting Forever

Many people unknowingly hold bonds that stopped earning interest years ago. While they generally remain redeemable, leaving them in a drawer means they're no longer growing. Checking their status now could help you put that money to better use.

The Process Is Usually Simpler Than People Expect

At first glance, old savings bonds can seem confusing, especially if they're decades old or belonged to another family member. In reality, identifying the series, checking the issue date, estimating the value, and following the Treasury's redemption instructions usually answers most questions. A little organization goes a long way.

Those Old Bonds May Still Be A Valuable Surprise

If your family recently discovered old savings bonds, don't assume they're worthless or impossible to redeem. Many continue to hold significant value, even after decades in a safe or filing cabinet. By identifying the bond series, checking whether it has matured, using the Treasury's valuation tools, and following the proper redemption process, you can determine exactly what they're worth and decide the best way to put that forgotten money to use.

You May Also Like:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}