What Happens to a Car Lease After Someone Passes Away?

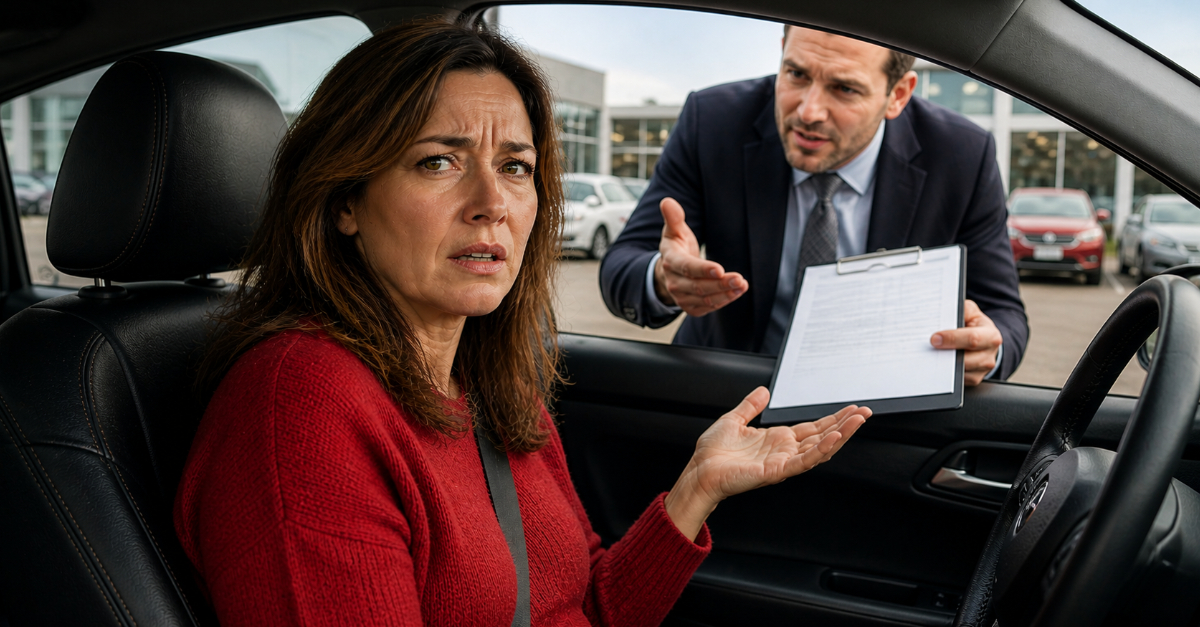

Losing a parent is already overwhelming—and then something like this shows up out of nowhere. A car lease with years left on it, a dealer asking for payments, and a situation that doesn’t feel right. So are you actually responsible for all of it?

The Lease Doesn’t Automatically Transfer to You

A car lease is a legal contract between your father and the leasing company—not you. When someone passes away, their contracts don’t just jump to the next of kin automatically. That means you typically don’t inherit the lease obligation just because you’re family.

The Estate Is What Matters First

When someone dies, their debts, including a car lease, become the responsibility of their estate, not individual family members. The estate includes assets like bank accounts, property, or anything of value your father left behind. Those assets are used to settle debts.

You’re Only Responsible If You Signed Something

This is one of the most important points. If you co-signed the lease, or agreed in writing to take responsibility at some point, then yes, you could be legally on the hook. But if your name is nowhere on that contract, that’s a very different situation.

Dealers Sometimes Push

Unfortunately, a dealer, leasing company, or debt collector may pressure family members to keep making payments. They might say things like “it’s now your responsibility” to avoid dealing with the estate process. That doesn’t automatically make it legally accurate.

Leasing Companies Have Their Own Policies

Many lease agreements actually include a clause for what happens in the event of death. Some allow early termination without major penalties. Others may still require the remaining balance, but again, from the estate. It’s worth reviewing the original lease contract.

There May Be Early Termination Options

In some cases, the leasing company may allow the lease to be ended early due to death. This could involve returning the car and settling a reduced amount rather than the full remaining payments. Not ideal, but often better than three more years of payments.

The Car Can Usually Be Returned

If no one in the family wants the vehicle, the leasing company can typically take it back. Depending on the lease terms, this may trigger early termination fees, remaining payments, or other charges, which are handled through the estate. This doesn’t erase the obligation, but it shifts everything back to the estate rather than you personally.

The Estate Pays Debts

If your father’s estate has enough money or assets, those will be used to cover obligations like the lease. This could include cash in bank accounts or proceeds from selling assets like a home or vehicle. If there’s not enough, the situation changes quite a bit.

If the Estate Has No Money, You Likely Owe Nothing

If the estate is insolvent (meaning it can’t cover its debts), unpaid obligations usually go unresolved. Family members are generally not required to step in and cover the difference out of their own pocket.

Being a Beneficiary Doesn’t Mean You Owe

If you’re a beneficiary, estate debts can still impact you, but not in the way dealers often imply. The estate must pay off obligations like a car lease before anything is distributed. So yes, that could reduce what you eventually inherit. But that’s not the same as being personally responsible. You’re not required to make payments out of your own pocket unless you were legally tied to the lease.

This Isn’t the Same as Inheriting Assets

People often assume that if they inherit something, they also inherit the debts tied to it. That’s not how it works. You can refuse assets—or accept them—but debts don’t automatically transfer unless you’re legally tied to them.

Taking the Car Can Change Things

If you decide to formally take over the lease, continue making payments, or sign paperwork related to the vehicle, that can complicate matters. Simply holding or storing the car temporarily while the estate is being handled is different, but taking steps that show ownership or responsibility could create legal obligations. It’s important to be careful before making that decision.

Insurance and Registration Still Matter

Even if the car is sitting unused, insurance and registration may still need to be handled temporarily. This is usually managed through the estate until a final decision is made.

Provincial and State Laws Can Vary

Rules around estates and debt can differ depending on where you live. This is especially true for situations involving spouses, joint debts, guarantors, or community property laws in some U.S. states, as well as creditor priority rules in Canadian provinces. That’s why local legal advice can be helpful here.

The Executor Handles This Process

If your father named an executor in his will, that person is responsible for handling debts like this. That includes notifying the leasing company, managing payments from the estate, and arranging the return or resolution of the vehicle. It shouldn’t fall on you unless you’re that executor.

Even Executors Don’t Pay Personally

Important distinction: even if you are the executor, you’re not paying out of your own money. You’re simply managing the estate’s funds and obligations.

Get Everything in Writing

If the dealer is telling you that you’re responsible, ask them to show exactly where that obligation exists—in writing. Verbal claims don’t mean much in situations like this.

Don’t Make Payments Without Clarity

Making even one payment can muddy the waters. It could potentially be interpreted as you accepting responsibility. Before paying anything, make sure you fully understand your legal position.

You Can Contact the Leasing Company Directly

Instead of relying on the dealership, reach out to the leasing company itself. They control the contract and can explain the official policy for death-related situations, which may be very different from what the dealer is telling you.

A Lawyer Can Quickly Clarify Things

This might sound intimidating, but even a short consultation with an estate or probate lawyer can clear things up fast. They can tell you exactly where you stand based on your situation and location.

This Situation Is More Common Than You Think

A lot of families run into issues like this after a loved one passes, especially with car loans and leases. And in many cases, they’re told they owe something when they actually don’t.

The Bottom Line

In most cases, you are not personally responsible for your father’s car lease unless you co-signed or agreed to take it on. The obligation typically belongs to the estate, not you. And while dealers may push for payment, that doesn’t mean the law is on their side.

You Might Also Like: