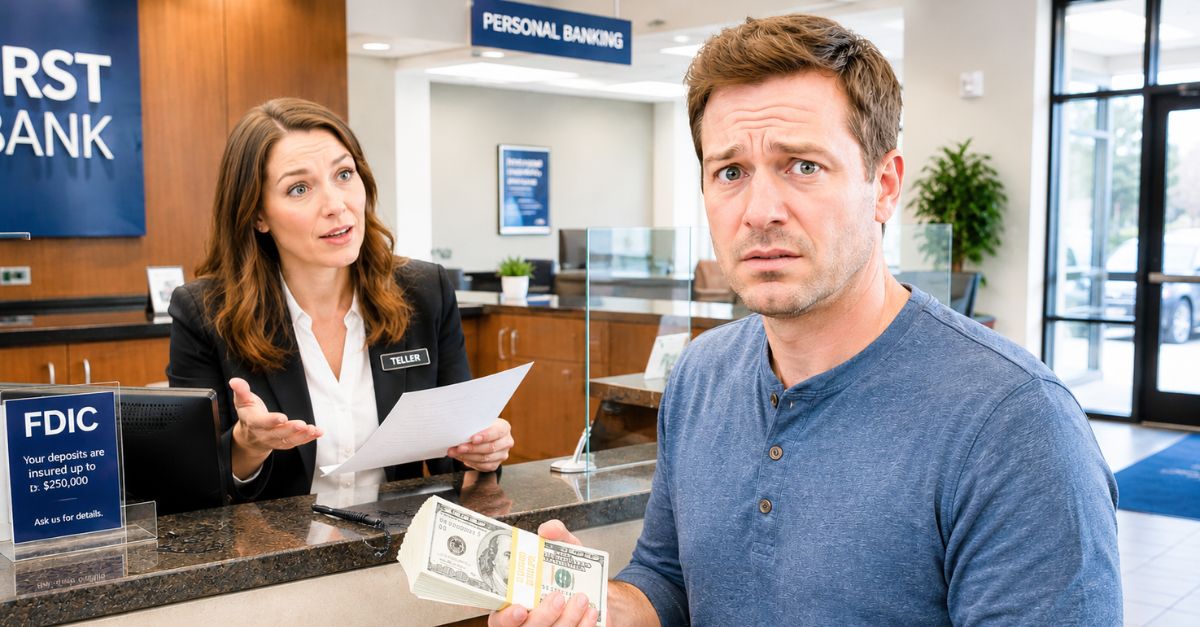

When Your Money Suddenly Gets Locked Up

A big deposit can make you or break you, but that night you double-check your balance everything suddenly grinds to a halt. Your debit card stops working, online access gets limited, and it's impossible to get a straight answer from the bank. That makes it personal, but in many cases the truth is it comes down to compliance rules, fraud checks, and anti-money laundering systems kicking in.

Yes, A Bank Can Freeze Access

In simple terms, yes. A bank can restrict or freeze an account while it reviews suspicious activity. Banks usually have broad power under account agreements and federal law to place holds, block transactions, or even close accounts. What they generally cannot do is hold your money forever without a legal reason, but they can delay access while they investigate.

The Rules Start With Deposit Hold Laws

A lot of the confusion comes from the fact that two different things may be happening at once. A bank might place a standard deposit hold under the Expedited Funds Availability Act and Regulation CC, or it might freeze an account because of suspected fraud or suspicious activity. Deposit hold rules are fairly specific. Fraud freezes are often much less clear to customers.

What Regulation CC Actually Covers

Regulation CC sets the basic rules for when deposited funds must generally be made available, especially for checks. The Consumer Financial Protection Bureau says many check deposits must be available within certain time frames, though banks can extend holds in some cases. Those exceptions include large check deposits, new accounts, repeated overdrafts, and reasonable cause to doubt that the check will be paid.

Large Deposits Often Get Extra Scrutiny

A large deposit is not illegal, but it can get attention fast. The Office of the Comptroller of the Currency says banks must watch for unusual activity as part of anti-money laundering compliance. If the amount, source, or pattern does not fit your normal account activity, the bank may review the transaction before giving full access back.

The $10,000 Myth Needs Clearing Up

A lot of people think any deposit over $10,000 automatically leads to a frozen account. That is not how it works. Cash transactions over $10,000 generally trigger a Currency Transaction Report under Bank Secrecy Act rules, but a report is not the same as a freeze and does not automatically mean you did anything wrong.

Who Requires Those Reports

The Financial Crimes Enforcement Network, or FinCEN, runs the Bank Secrecy Act reporting system. Financial institutions must file Currency Transaction Reports for certain cash transactions over $10,000 and Suspicious Activity Reports when they spot possible illegal activity. Those filing rules are one reason banks can seem so tight-lipped when customers ask what is happening.

Why The Bank May Not Tell You Much

If your account is frozen because of suspicious activity monitoring, the bank may reveal very little. Federal law makes Suspicious Activity Reports confidential, and banks generally cannot tell a customer whether one was filed. That silence is maddening, but it often reflects legal limits, not just bad customer service.

Suspicious Does Not Mean Guilty

This part matters. A suspicious activity review does not mean the bank has proved fraud, money laundering, or tax crimes. In many cases, it simply means the transaction looked unusual enough for the bank to hit pause and start asking questions.

Check Deposits Follow Their Own Timeline

If your large deposit was a check, the bank may also be dealing with collection risk. Regulation CC allows longer holds for certain large deposits, generally for the amount over $5,525, and for other exception situations. The exact timing depends on the type of check, your account history, and whether the bank has reason to think the check may not clear.

Cash Deposits Usually Work Differently

Cash is usually available faster than checks under funds availability rules, especially if you deposit it in person with a bank employee. But a cash deposit can still trigger anti-money laundering review if it is large or unusual. So even when normal availability rules point to quick access, a separate fraud review can still lock things up.

Wire Transfers Can Raise Flags Too

Wire deposits are generally treated as collected funds, but they are not immune from review. A sudden international wire, a large domestic transfer from an unfamiliar source, or a pattern that does not match your usual account activity can all trigger a fraud hold. Banks are under pressure from regulators to catch and stop illegal money flows, especially through fast-moving payment channels.

Your Account Agreement Gives The Bank A Lot Of Power

Buried in the account agreement is often language that lets the bank place holds, refuse transactions, or close the account if it suspects fraud, legal risk, or policy violations. That contract matters. It does not override federal law, but it often gives the bank wide room to act during a review.

Can They Hold Your Money Forever

Usually not. A temporary hold during an investigation is one thing. Keeping your funds indefinitely without a valid reason, sending back deposits without cause, or refusing to release funds after the review is over can turn into a legal and regulatory problem for the bank.

There Is No Simple Deadline For A Fraud Freeze

This is where many customers get stuck. Regulation CC gives timelines for many deposit holds, but there is no simple federal rule saying every suspicious activity freeze must end within a set number of days. The timing can depend on whether the bank is verifying a check, investigating fraud, responding to law enforcement, or deciding whether to close the account.

First, Ask What Kind Of Restriction This Is

Your first practical step is to figure out what kind of problem you are dealing with. Ask whether the bank placed a hold on one specific deposit, restricted the whole account, or closed the account pending review. Those are different situations, and the answer affects what timelines and rights may apply.

Get Everything In Writing

Ask the bank for written notice of any hold, restriction, or closure. Regulation CC generally requires notice for many exception holds on checks, including the reason for the hold and when funds will be available. If the bank will not say much, at least ask for the date the restriction started, what documents it needs, and when you should expect an update.

Be Ready To Show Where The Money Came From

If the deposit was legitimate, paperwork can help. Gather the check stub, sale contract, closing statement, inheritance papers, payroll records, invoice, or transfer confirmation showing where the money came from. A clean paper trail will not always get your account unlocked right away, but it can ease the bank’s concerns.

Do Not Try To Game The System

If you are thinking about splitting deposits into smaller amounts or moving money around to avoid attention, do not. Structuring transactions to dodge reporting rules is itself illegal under federal law. What might have been a routine review can start to look much worse.

Escalate Calmly Inside The Bank

Start with the branch, but do not stop there if you get nowhere. Ask for the deposit operations department, fraud department, or executive customer relations team. Keep notes with dates, names, and exact statements. A clear timeline can matter if you end up filing a complaint.

The CFPB Is A Real Next Step

If the bank is not responding or you think it is violating deposit hold rules, the Consumer Financial Protection Bureau takes complaints online. The CFPB forwards complaints to companies and tracks their responses. That process will not force a bank to reveal a Suspicious Activity Report, but it can push the bank to explain itself more clearly.

Your Regulator Depends On Your Bank

Some banks are overseen by the Office of the Comptroller of the Currency, some by the Federal Reserve, and state-chartered banks may also answer to the FDIC or state regulators. If your bank is national, the OCC’s customer assistance process can be a useful next stop. Finding the right regulator can speed things up because your complaint reaches the agency that actually supervises the bank.

Credit Unions Answer To A Different Watchdog

If your frozen account is at a federally insured credit union, the National Credit Union Administration may be the right regulator instead. Credit unions also follow anti-money laundering rules and may freeze accounts during reviews. The oversight path is different, but the headache is often the same.

What If The Bank Closes The Account

Banks can usually close accounts under the deposit agreement, subject to certain legal duties. In many cases, once the review ends, the bank sends a check for the remaining balance or transfers the funds using its normal process. If that does not happen, or the money is held for an unusually long time, it is time to escalate quickly and think about getting legal advice.

When Law Enforcement Is Involved

Sometimes the freeze is not just the bank’s call. A court order, garnishment, levy, or law enforcement request can restrict funds, and bank staff may be limited in what they can say. If you think that may be happening, ask whether the bank is acting under legal process and whether any notice was sent to you.

The Fastest Way To Protect Yourself

If your main account is frozen, protect your cash flow right away. Redirect direct deposit if you can, move automatic bill payments to another account, and make sure you have enough money elsewhere for rent, food, and utilities. This is one reason it helps to keep an emergency cushion at a second institution.

How To Lower The Odds Of Another Freeze

When possible, give your bank a heads-up before a large unusual deposit, especially after a home sale, business deal, insurance payout, or family transfer. Use clear memos and keep supporting documents handy. Steady account activity and proof of where the money came from make it easier for the bank to understand what it is seeing.

The Bottom Line

A bank can temporarily restrict access to your money after a large deposit, and it may not tell you much if suspicious activity rules are involved. But that power has limits, and you have options: get written notice, document the source of funds, escalate inside the bank, and complain to the right regulator if the bank goes quiet. If the freeze drags on or the amount is large, it may be worth calling a consumer finance attorney.