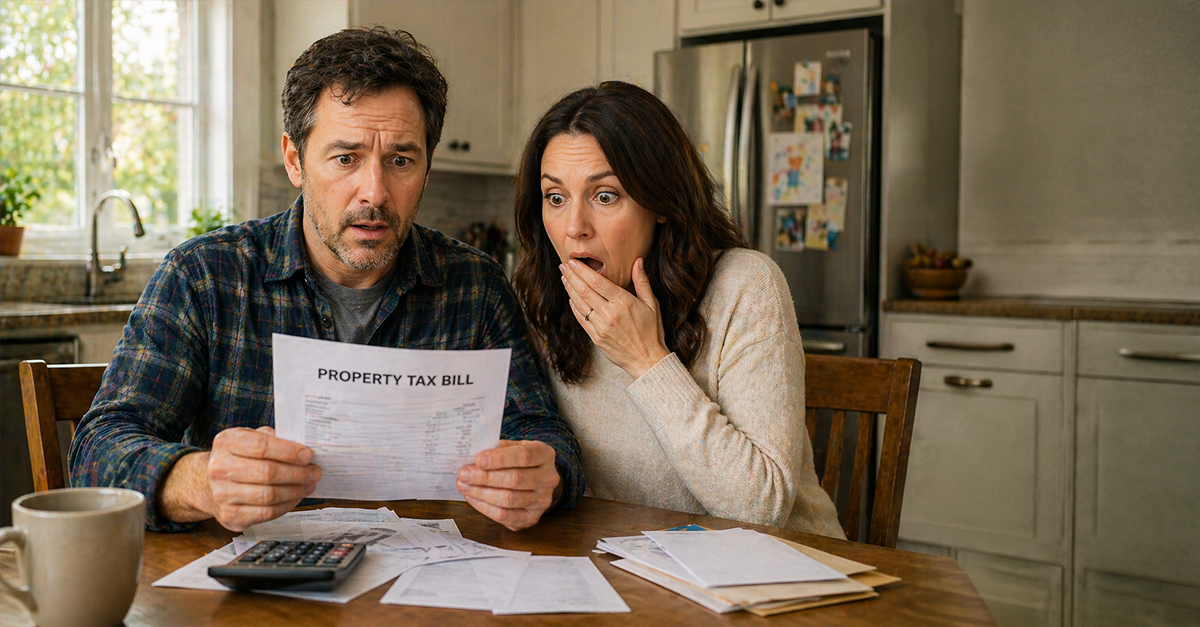

The Shock Of A Rising Assessment

You opened your latest property tax bill bracing yourself for the worst, but felt a jolt of disbelief. Your home’s assessed value climbed 20%, and your tax bill followed right behind it. You haven’t sold your home or earned any extra income, but you owe significantly more. It feels like you’re being taxed on money you haven’t actually received.

Why It Feels Like A Tax On Paper Gains

When your home’s value increases without a sale to go with it, that rise is considered an unrealized gain. In most cases, taxes on capital gains only apply when you sell and lock in a profit. So when your tax bill is hiked alongside your home’s assessed value, it naturally feels like the system is jumping the gun.

What An Unrealized Gain Really Means

An unrealized gain is simply a change in value on paper. If your home rises from $300,000 to $360,000, that $60,000 increase exists only in theory. You cannot spend that extra $60,000 unless you sell or borrow against it, which is why taxing it directly would be controversial.

Why Property Taxes Are Structured Differently

The issues here is that property taxes aren’t technically based on gains at all. They are based on ownership and assessed value. Local governments use property values to determine how much each homeowner contributes to public services, regardless of whether any income or profit has been realized or not.

The Key Distinction You Need To Know

A capital gains tax is triggered by a sale. Property tax is triggered solely by ownership. That difference is why governments can raise your tax bill without you having to sell your home. Even though the effect seems similar, the legal framework is totally different.

How Your Assessment Drives Your Tax Bill

Your municipality periodically reassesses homes to reflect the prevailing market conditions. It’s pretty simple: if property values have gone up across your area, your assessed value goes up too. Unless tax rates are adjusted downward, your total bill will go up along with that new valuation.

Why Municipalities Rely On This System

Property taxes are a stable, predictable source of revenue for local governments. Because real estate can’t be moved or hidden, it forms a reliable tax base. This stability helps fund schools, roads, and emergency services, even though it nobody would deny that it can present sudden financial pressure for homeowners.

Why The System Feels Unfair

Your frustration here comes from a real issue. Your tax bill is rising without any corresponding increase in your income. You may be wealthier on paper, but that doesn’t help you pay the bill. This is the disconnect that makes property taxes feel like a tax on unrealized gains.

Your Liquidity Problem

This situation creates a situation that economists like to diplomatically call a “liquidity problem.” Your asset value has gone up, but your available cash hasn’t kept pace. That can force you to make some difficult choices, especially if property taxes go up faster than your income over time.

Why Governments Avoid Calling It A Gain Tax

Governments frame property taxes as taxes on ownership, not profit. This distinction allows them to tax based on value without causing the same concerns that come with taxing unrealized gains directly. Still, the financial impact can feel very similar from your perspective.

Should You Appeal Your Assessment?

If your tax bill jumped sharply, it’s worth considering an appeal of your assessment. Assessments aren’t always perfectly accurate, and even small errors can result in meaningful overpayment. Taking a closer look is often the first and most practical step.

Signs Your Assessment Might Be Too High

If your assessed value is significantly higher than similar homes nearby, that is a red flag. Differences in square footage, condition, or location can also cause inflated assessments. These discrepancies give you a stronger case for filing an appeal.

How To Check Comparable Properties

Research recent sales of homes similar to yours in your neighborhood. Pay attention to size, age, and condition. If comparable homes are selling for less than your assessed value, that information can back your argument for a reduction.

What The Appeal Process Looks Like

Most jurisdictions allow you to file a formal appeal within a set timeframe. You’ll need to provide evidence including comparable sales data or an independent appraisal. While this process can take time, many homeowners see meaningful reductions in their assessments.

When An Appeal Makes Sense

An appeal is most worthwhile when you can prove a clear gap between your assessed value and market reality. If your valuation aligns closely with recent sales, your chances of success go down. Still, it’s always a smart move to review the numbers.

Understand Tax Rates Vs Value

Even if your home’s value rises, your final tax bill depends on local tax rates. Sometimes municipalities adjust rates to offset rising assessments. Having a grasp of both factors helps you see whether your increase is driven by value, policy, or both.

Plan For Future Increases

Property taxes can fluctuate over time, especially in rapidly growing real estate markets. Building some flexibility into your budget can leave you better able to handle future increases without financial strain. It is better to prepare ahead of time than to be caught off guard again.

Consider Your Long-Term Options

If rising property taxes turn into a recurring issue, you may want to consider broader changes. Downsizing, relocating, or restructuring your finances can all help manage long-term housing costs. These decisions aren’t easy, but they can offer you some stability.

The Bigger Debate Around Asset Taxes

There’s an ongoing debate about whether taxes based on asset values are fair. Some see them as a way to ensure that contributions reflect wealth. Others argue they burden people who are asset-rich but cash-poor. Your situation sits right smack dab in the middle of that debate.

Bottom Line

It may feel like a tax on unrealized gains, but property taxes are legally based on ownership, not profit. Having said that, it doesn’t mean you have to accept your bill without question. Review your assessment, consider an appeal, and take definite steps so you can manage future increases with confidence.

You May Also Like: