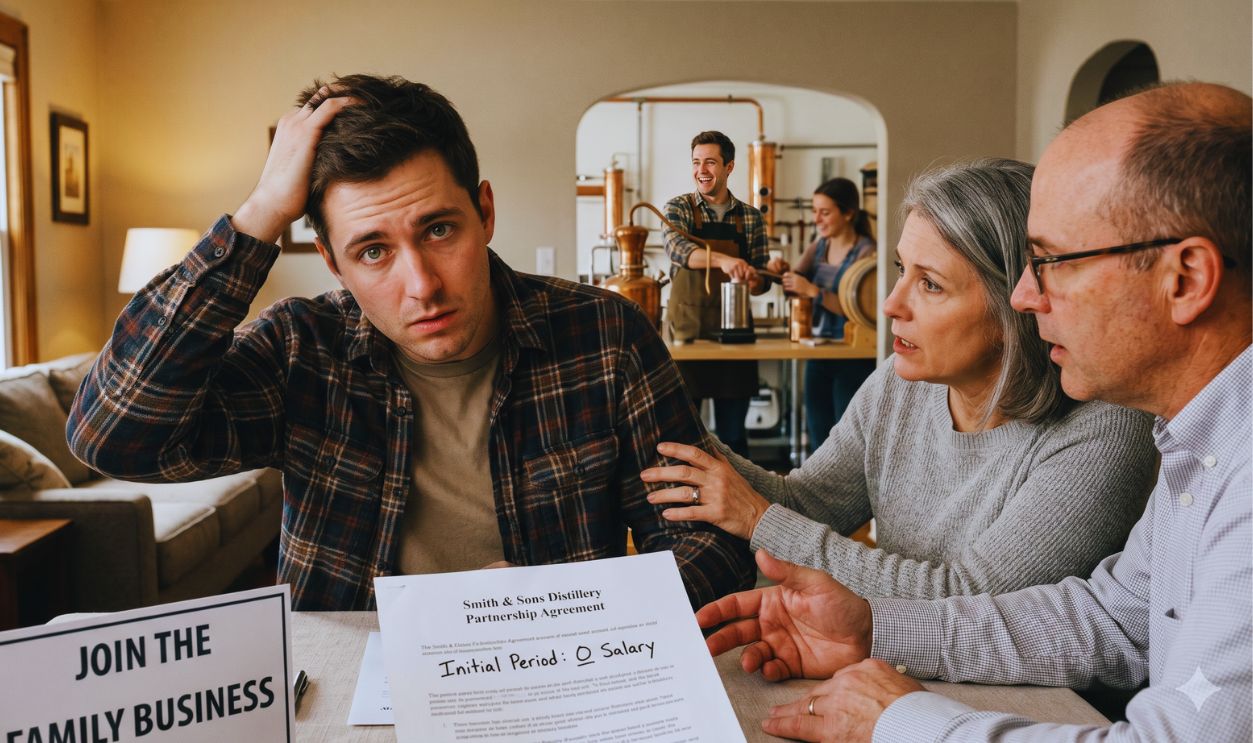

The Offer That Changes Everything

Your parents want you to leave a paying job and join the family business, but there is a catch. They want you to start with no salary, at least for a while. That kind of offer can stir up equal parts dread and curiosity. It puts money, identity, loyalty, and risk in the same room. Yes or no could both be the right decision, but you have to make sure you know what you're getting into.

Why This Feels So Loaded

A family business is never just a job. It can carry years of sacrifice, pride, and unspoken expectations. The U.S. Census Bureau has noted that most U.S. employer firms are family owned, so this is not some rare dilemma. A lot of people have had to ask themselves the same question: Is this a smart career move, or an emotional one?

The No Salary Part Is The Real Flashpoint

Joining a family business can sound exciting. Doing it without pay is where things get serious. The U.S. Department of Labor says workers in the private sector generally must be paid at least the federal minimum wage for all hours worked, with very limited exceptions. If your parents expect regular work in a for-profit business, that matters right away.

This Is Not Just A Family Conversation

It is easy to frame this as a personal favor, but it can also be a labor law issue. The Fair Labor Standards Act sets the national baseline for minimum wage and overtime rules. State laws can be stricter. So an unpaid setup that feels normal inside the family may still be unlawful on the job. Before you get into guilt, gratitude, or family duty, start with compliance.

What The Law Generally Says

The Department of Labor draws a key line between for-profit businesses and true volunteer work. In general, people cannot volunteer unpaid services to a for-profit company the way they might for a charity or public agency. That does not mean every family arrangement is automatically illegal, but it does mean the business needs to get this right. If you would be doing real work that would usually be done by a paid employee, that should raise concerns.

Family Ties Do Not Erase Wage Rules

A lot of people assume a family business can make its own rules. Usually, it cannot. Being related does not automatically cancel wage protections. The Department of Labor recognizes some narrow exemptions involving certain family members in certain business structures, but those are not blanket carve-outs. The details can depend on the business setup, your role, your age, and state law.

Ask The Most Important Question First

What exactly does “no salary at first” mean in writing, not just in spirit? Is it two weeks, three months, or an open-ended test of loyalty? If there is no clear timeline, no milestones, and no set review date, then this is not really a plan. It is uncertainty dressed up as trust.

If Equity Is On The Table, It Must Be Real

Sometimes families try to justify no salary by promising ownership later. That can be meaningful, but only if it is documented and clearly structured. How much equity? When does it vest? What happens if you leave? Do you get voting rights? A vague promise that “this will all be yours someday” is not compensation.

The Hidden Cost Of Leaving A Paying Job

Your current paycheck is not just a paycheck. It may also include retirement contributions, payroll tax withholding, unemployment insurance coverage, and maybe health insurance. The Consumer Financial Protection Bureau has warned how quickly cash-flow shocks can throw off a household budget. Giving up steady income can hit harder and faster than people expect.

ANTONI SHKRABA production, Pexels

ANTONI SHKRABA production, Pexels

Do The Cash Math Before You Do The Loyalty Math

Add up your rent or mortgage, food, transportation, debt payments, insurance, and emergency savings needs. Then compare that with what your finances would look like if your income dropped to zero. The CFPB recommends keeping an emergency buffer, and that matters even more when you are thinking about a risky career move. If the numbers do not work, loyalty will not make them work.

Set A Runway, Not Just A Dream

If you are seriously considering this, figure out exactly how long you can go without income. That should be a hard limit based on cash, not optimism. Maybe it is six weeks. Maybe it is three months. Whatever the number is, make it real. Once you know your runway, you can negotiate from reality instead of emotion.

Treat The Family Business Like Any Other Employer

Ask for financial statements, recent revenue trends, debt obligations, and payroll history. That may feel awkward, but it is standard due diligence. If the business is healthy, your parents should be able to explain how and when it can support your role. If they resist basic transparency, that tells you something too.

Get Clear On Your Actual Job

Titles can get blurry in family companies. “Help out where needed” may sound harmless, but it often leads to chaos and no clear path forward. Ask for a written job description, specific responsibilities, and a clear sense of how much authority comes with the role. You need to know whether you are stepping into a future leadership track or just filling gaps as unpaid labor.

Succession Drama Is Very Real

The Family Business Institute and other advisory groups have long warned that failed succession plans can hurt both the company and the family. Transitions often stall when founders cannot let go or when the next generation never gets real authority. If your parents talk about the future but still control every decision, your role may end up being more symbolic than strategic. That is how resentment starts.

Christina @ wocintechchat.com M, Unsplash

Christina @ wocintechchat.com M, Unsplash

The Best Sign Is A Specific Growth Plan

A solid offer from a family business has milestones. It may include training goals, performance targets, and a salary start date tied to revenue or responsibilities. It may also spell out when ownership talks happen and who reviews your progress. Precision is not cold. It is a sign that the opportunity is real.

The Worst Sign Is Emotional Pressure

Be careful if the pitch sounds more like obligation than opportunity. Phrases like “we need you” or “family should sacrifice” may be sincere, but they can also be a way to avoid paying fair wages. When guilt is doing most of the recruiting, there is usually a deeper business problem underneath. Healthy businesses make a business case.

Taxes Matter More Than People Expect

If you leave a regular job, your tax situation may change in ways that affect your budget. The Internal Revenue Service offers guidance on worker classification and compensation, and getting that wrong can create headaches for both the worker and the business. If your role mixes labor and ownership, the structure should be reviewed carefully. This is the kind of situation where a CPA can save everyone a lot of trouble.

Health Insurance Can Become A Major Problem Fast

Employer-sponsored health coverage is one of the easiest parts of job security to overlook. Losing it can mean a big jump in monthly costs, especially if you need coverage right away. Before you resign, figure out whether you would use COBRA, a marketplace plan, or family coverage if that is an option. The price can be much higher than people expect.

Vitaly Gariev, Unsplash, Modified

Vitaly Gariev, Unsplash, Modified

Your Resume Risk Is Not Imaginary

Joining a family business can be a smart long-term move, but it can also create short-term career risk if the role is vague. Future employers may understand a move into family leadership. They may be less impressed by a position with no title, no formal compensation, and no clear achievements. Protect yourself by defining what success would look like on paper.

There Is A Difference Between Investing And Working For Free

If you believe in the business, you might choose to invest money or accept reduced pay for a limited period in exchange for ownership. That is very different from simply doing unpaid work. One is a negotiated risk with a possible return. The other can turn into a one-sided sacrifice unless it is formally structured. That distinction matters.

Put Every Promise In Writing

This is the part that can protect both your finances and your family relationships. If your parents promise future pay, equity, profit sharing, reimbursement, or eventual control, write it down. Written agreements reduce confusion and make hard conversations easier later. They also force everyone to be honest about what they actually mean.

Create A Trial Period With Exit Terms

If you want to explore the opportunity without taking a blind leap, suggest a short trial period. Set the start date, end date, weekly hours, responsibilities, and the exact point when salary or equity gets decided. Also include what happens if either side decides it is not working out. An exit plan is not pessimistic. It is smart.

Bring In A Neutral Professional

Family dynamics can make basic business questions feel personal. A business attorney, CPA, or family business consultant can help turn loose ideas into clear, enforceable terms. They can also spot wage law, tax, governance, and ownership issues that relatives may miss. Outside advice often protects the relationship as much as the deal itself.

Ask Yourself One Brutally Honest Question

If this offer came from someone else’s parents, would you take it? That question cuts through a lot of emotion. If the answer is no, figure out what would need to change to make it a rational decision. Those changes are probably the terms you should be asking for.

When It Might Actually Make Sense

This move can make sense if the business has healthy financials, your role is strategic, the unpaid period is short and legal, and future compensation is documented. It can also make sense if you have enough savings to handle the risk and you truly want this path. In the best cases, family businesses can offer unusual trust, responsibility, and long-term upside. But the upside should be specific, not sentimental.

When You Should Probably Walk Away

If there is no written plan, no timeline for pay, no clarity on ownership, and no respect for wage rules, think hard before saying yes. The same goes for situations where the business is already struggling and your unpaid labor is being treated as the fix. Wanting compensation and clarity does not make you selfish. It makes you realistic.

You Are Not Crazy, But You Do Need Guardrails

Considering the family business does not make you naive. It means you see potential, and maybe even legacy, in something your family built. But even a good opportunity can still be a bad deal if the terms are vague. Love your family, but read the fine print.

Vitaly Gariev, Pexels, Modified

Vitaly Gariev, Pexels, Modified