That was not the amount I asked for

You walk up to the ATM, punch in your PIN, and request $500. Completely routine. But instead of stopping, the machine keeps dispensing cash. You count it...$6,500. No warning, no error message, nothing unusual on screen. Just stacks of bills. It feels like a lucky glitch—but it’s actually the start of a situation banks take very seriously.

Wait…did that just happen?

At first, it doesn’t even feel real. The receipt might still say $500, which makes it even more confusing. You double-check the cash, look around, and realize this wasn’t a visual mistake—you actually received an extra $6,000.

Is this actually free money?

It’s easy to rationalize it. You didn’t force the machine or do anything unusual. But banks process large volumes of ATM transactions every day, and their systems are built to catch discrepancies, especially ones this large.

Centre for Ageing Better, Pexels

Centre for Ageing Better, Pexels

Why it feels so tempting

That extra cash can feel like relief. The Federal Reserve has found many Americans struggle to cover even a $400 emergency. So, suddenly having thousands in hand can feel like a rare chance to get ahead fast.

Spending it happens faster than you think

Because it doesn’t feel earned, it often gets spent quickly. Paying bills, clearing debt, or making purchases can burn through thousands faster than expected. Studies on “windfall spending” show people are far more likely to spend unexpected money quickly rather than save it.

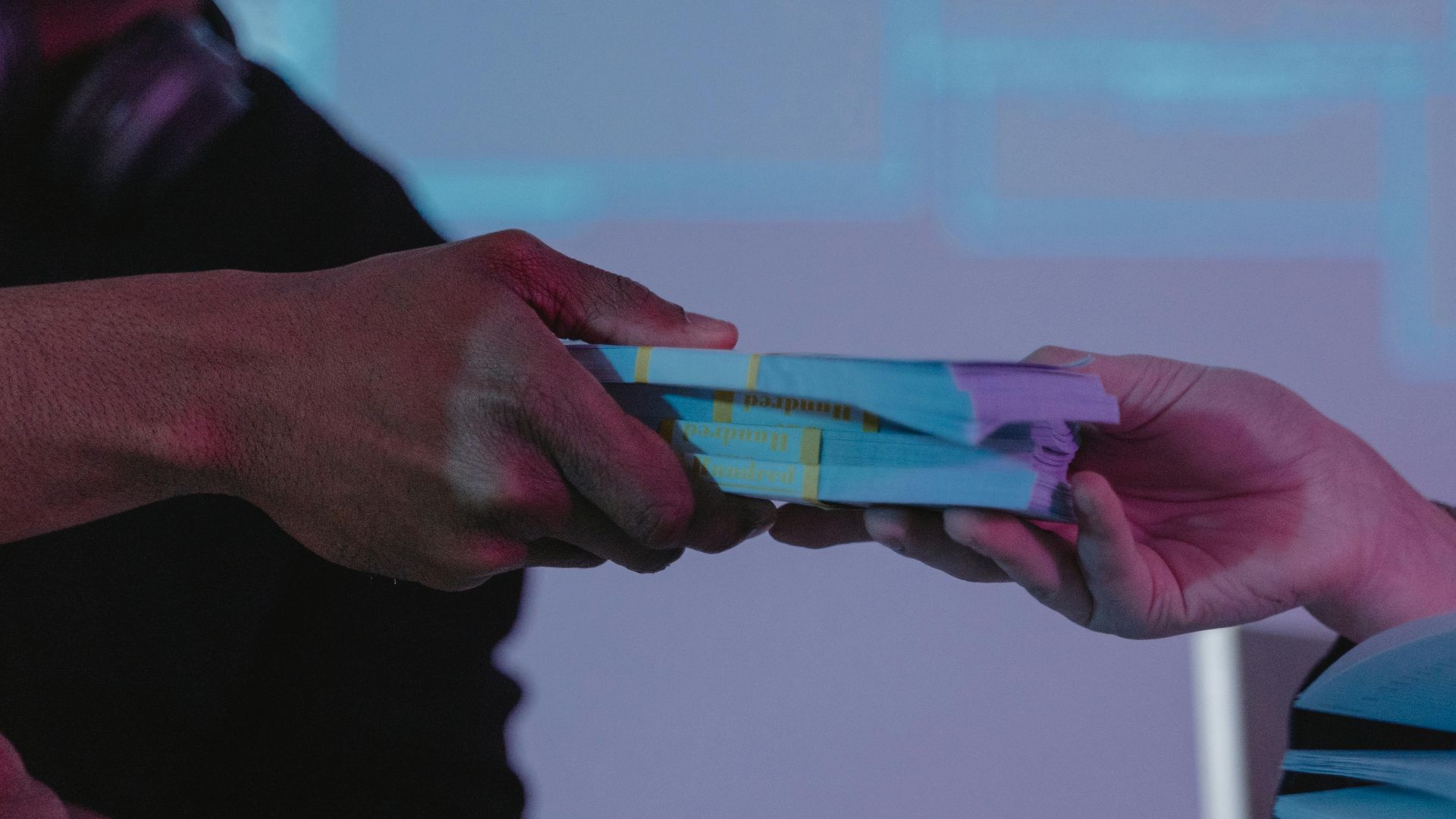

ATMs don’t just lose money like that

Modern ATMs track every bill using internal sensors and counters. Banks process large volumes of ATM transactions daily, and machines are regularly balanced against expected totals—so even small discrepancies tend to get flagged quickly.

Every dollar gets tracked and reconciled

Banks regularly reconcile ATM balances, often daily or within 1–2 business days. If a machine is short thousands, it’s flagged and investigated during these checks, even if the customer says nothing.

Yes, there are cameras watching

Most ATMs have high-resolution cameras recording every transaction. Banks can match the exact time of the error with footage to identify who was at the machine.

There’s also a full digital trail

Your card, account, withdrawal request, and timestamp are all logged. Even if the receipt says $500, the system can identify when excess cash was dispensed and tie it to your transaction.

The money is not legally yours

Even though the ATM made the mistake, that doesn’t shift responsibility. Banking errors don’t transfer ownership—the money still belongs to the bank, and you’re expected to return it once the error is identified.

This is called unjust enrichment

Legally, this situation is known as unjust enrichment—you benefited from a mistake at someone else’s expense. Once you become aware of the error, you’re expected to return the money. It doesn’t matter that you didn’t cause the mistake, what matters is knowingly keeping funds that aren’t yours.

Spending it is where it becomes a problem

There’s a big difference between receiving the money and deciding what to do with it. If you immediately report it, it’s usually treated as a simple error. But if you knowingly keep and spend it, that’s when things escalate. In many cases, it starts as a civil issue (repayment), but it can become a criminal matter if it’s clear the money was knowingly used.

People have actually been charged for this

There are real cases of people facing theft or fraud charges after keeping ATM overpayments—especially when they knowingly spent the money. The outcome often depends on the amount involved and whether intent can be proven.

The bank will come looking for it

Banks don’t ignore missing money. You’ll likely get a call, email, or notice asking about the discrepancy. In many cases this happens within a few days, though sometimes it can take a few weeks, but it’s almost always discovered.

They can take money back from your account

If the extra funds are still sitting in your account, the bank may reverse the transaction or debit the difference, depending on the situation. This is often the fastest way for them to correct the error.

Your account could get frozen

If the issue isn’t resolved quickly, your account may be restricted or frozen during the investigation. That can mean no withdrawals, no transfers, and even declined payments. Some people only realize something is wrong when their card suddenly stops working.

It can turn into a debt fast

If the money is already spent, the bank typically treats it as a debt you owe. That can come with repayment demands—and in some cases, additional costs may be added if the situation goes unresolved or is sent to collections.

You still have to pay it back

Spending the money doesn’t change anything. If you received $6,500 and used it, the bank will still expect the full amount back. At that point, it’s treated like a debt. If you can’t repay it right away, you may need a payment plan—or risk collections or legal escalation.

And it can hurt your credit

If the debt goes unpaid and gets sent to collections, it can stay on your credit report for up to 7 years. Collection agencies may also add fees or pursue further recovery.

This kind of ATM mistake does happen

ATM errors are rare but real. One common issue is machines being loaded incorrectly—like dispensing $100 bills instead of $20s.

But banks always catch it eventually

Between audits, tracking systems, and physical cash counts, missing thousands of dollars will be discovered. Banks are required to maintain strict internal controls, so even rare errors are investigated and corrected, sometimes weeks later.

If you act quickly, it usually stays a simple mistake

If you report the error right away or cooperate fully when contacted, banks typically treat it as a correction, not a crime. In many cases, there are no legal consequences, just repayment.

What you should have done instead

The safest move is to report the error immediately. Acting quickly shows good faith and usually prevents things from escalating.

What to do now that they’re calling

Don’t ignore the bank. Be honest and work with them. The sooner you deal with it, the better your chances of avoiding serious consequences.

The bottom line

It might feel like a lucky break, but it’s not free money. Keeping and spending an ATM error can lead to repayment demands, account restrictions, credit damage, added costs, and even legal trouble. That quick win can turn into a long-term headache fast.

You Might Also Like: